Download

1 / 9

150 likes | 643 Views

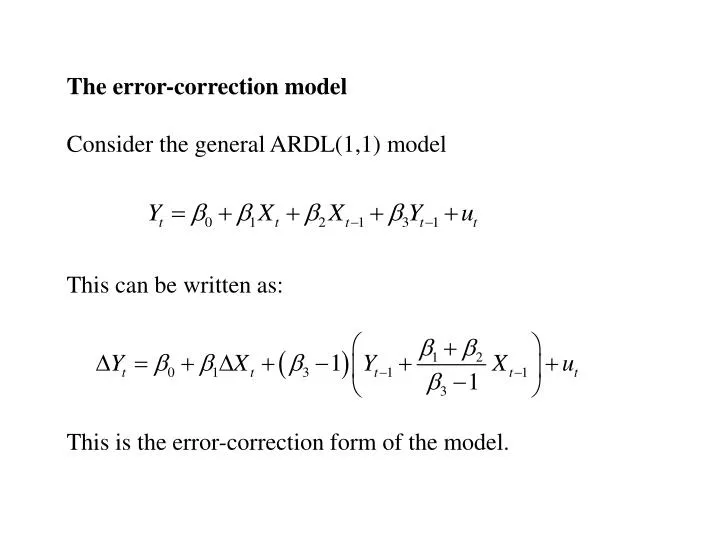

The error-correction model Consider the general ARDL(1,1) model. This can be written as:. This is the error-correction form of the model. The important features of the error-correction model are: 1. A relationship between the growth rate (or differences) of the

E N D

The error-correction model Consider the general ARDL(1,1) model This can be written as: This is the error-correction form of the model.

The important features of the error-correction model are: 1. A relationship between the growth rate (or differences) of the LHS variable and those of the RHS variables which describes short-run adjustment. 2. A relationship in levels between the variables which describes the long-run equilibrium relationship. 3. A parameter which describes the speed of adjustment when the variables are away from long-run equilibrium There is ALWAYS an algebraic transformation which allows us to write an ARDL model in EC form but some of the variables may not be significant when it is estimated.

The parameters of the error-correction model have natural economic interpretations.

Example: The following equation is an ARDL(1,1) model for UK imports

Note that when we write this is error-correction form the LHS variable becomes DLOG(M). This can be interpreted as a growth rate because: This is another reason why the log transformation is often used in econometric models.

The error-correction form of the model can be estimated as: This equation is just a different way of writing the ARDL model. This can be seen by the fact the SEE and other statistics based on the residuals are identical.

Why use the error correction form of the model? 1. The parameters have more natural economic interpretations than those of the ARDL model. 2. The ECM provides a test for the existence of a long-run relationship between the variables (whether the coefficient on the lagged endogenous variable is significantly negative). but…. the distribution of the estimator for the coefficient on the lagged endogenous variable is non-standard – the critical values are higher than those for the t distribution.

One method of estimating the ECM is to use the residuals from an OLS regression as a measure of disequilibrium. This regression is misspecified because there is serial correlation. However, the coefficient estimates are consistent estimates of the long-run parameters.

Using the residuals from the OLS regression we can then estimate an ECM model. Note that the t-ratio for the lagged residual does not have a standard t-distribution. In this case it is not significant.