Download

1 / 4

40 likes | 132 Views

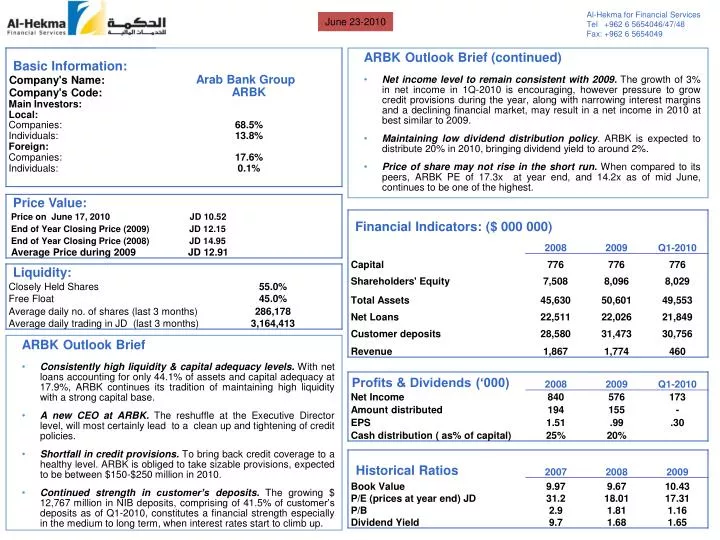

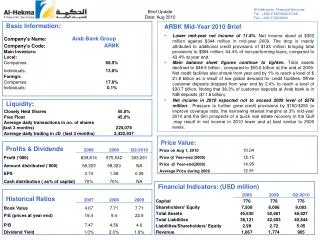

Al-Hekma for Financial Services Tel +962 6 5654046/47/48 Fax: +962 6 5654049. June 23-2010. ARBK Outlook Brief (continued)

E N D

Al-Hekma for Financial Services Tel +962 6 5654046/47/48 Fax: +962 6 5654049 June 23-2010 • ARBK Outlook Brief (continued) • Net income level to remain consistent with 2009. The growth of 3% in net income in 1Q-2010 is encouraging, however pressure to grow credit provisions during the year, along with narrowing interest margins and a declining financial market, may result in a net income in 2010 at best similar to 2009. • Maintaining low dividend distribution policy. ARBK is expected to distribute 20% in 2010, bringing dividend yield to around 2%. • Price of share may not rise in the short run. When compared to its peers, ARBK PE of 17.3x at year end, and 14.2x as of mid June, continues to be one of the highest. • ARBK Outlook Brief • Consistently high liquidity & capital adequacy levels. With net loans accounting for only 44.1% of assets and capital adequacy at 17.9%, ARBK continues its tradition of maintaining high liquidity with a strong capital base. • A new CEO at ARBK. The reshuffle at the Executive Director level, will most certainly lead to a clean up and tightening of credit policies. • Shortfall in credit provisions. To bring back credit coverage to a healthy level. ARBK is obliged to take sizable provisions, expected to be between $150-$250 million in 2010. • Continued strength in customer’s deposits. The growing $ 12,767 million in NIB deposits, comprising of 41.5% of customer’s deposits as of Q1-2010, constitutes a financial strength especially in the medium to long term, when interest rates start to climb up.

Performance Overview 2009 Overview Weakening trends • Sharp drop in net income. Due to slow economies as a result of the global financial crisis, ARBK registered in 2009 a net income of $575.5 million, a slide of 31.5% from 2008 levels. Net revenues in 2009 dropped by 5% on the back of a decline in net credit facilities by 2.2%, leading to lower revenues from interest and commissions of 3.3%. While expenses increased 17.7% mainly due to higher provisions for credit facilities of $204 million. Also a non-recurring income in 2008 of $36.8 million (sale of Cyprus branches), contributed to the drop • Steep rise in non-performing loans. NPLs in 2009 reached a record high of $1911.9 million, 8.3% of gross loans and 13.4% of equity. As compared to $960 million in 2008, 4.1% of gross loans and 4.2% of equity. A sizable portion of the NPLs is believed to be from the 20 top exposures in the Bank and concentrated in the construction and real-estate sector in the gulf region and Saudi Arabia. The deterioration in non-performing loans led ARBK to take additional provisions of $204 million in 2009, bringing credit provisions to $829 million, only 43.4% of non-performing loans, against a level of 67.5% in 2008 and 74.5% in 2007. When compared regionally, ARBK’s credit coverage ratios are much lower than its peers (NBK at 207% & Arab National Bank at 75.8%). Non withstanding the collateral of $489 million which ARBK maintains, additional provisions of similar if not higher levels will have e to take place in 2010 in order to improve credit coverage ratio. • Continued strength in customers’ deposits. The growing $12,143 million in NIB deposits, comprising of 38.6% of customer’s deposits as of end of 2009, constitutes to ARBK a financial strength in the medium to long term especially when interest rates starts to climb up. • Stable interest margin. Interest margin in 2009 remained at 3.3%, similar to that of 2008, even after the suspension of interest on an additional $951.9 million of non-performing loans in 2009. This implies that effectively interest margin in 2009 is slightly higher than that of 2008, while interest margin in 2007 was at 2.7%. Undoubtedly the higher interest margin has helped in the short run to partially compensate for the sizable loss of interest revenue as a result of the rise in NPLs. • Fee & commission income marginally lower. Fee and commission income in 2009 dropped by 1% to reach $ 283 million, . Traditionally ARBK has maintained a rather low fee and commission levels, comprising of .59% of average assets in 2009 as compared to the 1% ratio exhibited by similar rated banks. • Deterioration in efficiency levels. Return on average assets dipped sharply from 3.2% in 2008 to 2.1% in 2009, while efficiency ratio (Cost/Revenue) deteriorated from 45.1% in 2008 to 55.9% in 2009. • Growth in investments and corresponding income. • Total investments in 2009 increased by 25% to reach $8967 million, of which 6.5% is in shares, 34.7% is in treasury bills, 18.8% is in government bonds, and 38.2% is in other bonds. The main growth was in the financial assets available for sale, which reflected a rise of 55% to reach $ 6414.4 million, of which $3159.2 million represents bonds with no market value. However this does not necessarily reflect added risk, as ARBK has sizable investments in local currency bonds where its branches and subsidiaries operate. During 2009 profits from financial assets for trading and for sale reached $21.9 million while provisions for the drop in value of financial assets for sale declined by 78% to reach $ 38.7 million. • Lower fair value of financial assets held to maturity. During the global financial turmoil in Q3-2008 ARBK reclassified $755 million from financial assets for trading to financial assets held to maturity. This move may indicate ARBK intention to avoid taking any sizable provisions. In any case, the book value of financial assets (bonds) held to maturity declined by 27% to reach a level of $ 1891 million in 2009. The fair value of this investment as of year end is $ 1840.1 million, $ 51.6 million lower than the book value. Given the long maturity nature of this investment, no provisions are required. Noting that ARBK declared their expectation of full repayments of these bonds at maturity and that average effective interest rate is at 5.6% • Consistently high liquidity and capital adequacy levels. ARBK continues to maintain high level of liquid assets with net loans accounting for 44.1% of total assets and 60.5% of total deposits. Also ARBK’s capitalization has been consistently strong, underpinning the Bank’s conservative culture. In 2009 capital adequacy ratio improved to 17.9% from a level of 16.2% in 2008.

Q1-2010 Overview 2010 Outlook • Change at Senior Management Level. Q1-2010 witnessed a reshuffle at the Executive Director level, which usually leads in the short run to a clean up and tightening of credit policies. • Net income grew by 3.0%. Net income reached$173.3 million, against $168.6 million in Q1-2009. The growth is attributed to a relatively impressive rise in fees & commissions of 19% to reach $76 million and a hike in realized profits from investments available for sale to $25.4 million as compared to $ 2 million in 1Q-2009. • Non-performing loans recovered by 6%. Non-performing loans went down to $ 1,791.8 million compared to $1,911.9 at year end, while credit provisions grew by 5.4% to reach $849,6 million, bringing provision coverage ratio to 47.4% compared to 43.4% at year end. • Main balance sheet figures tighten. Uncustomary for ARBK, Q1-2010 balance sheet reflected a slight dip in several items from year end. Total assets went down by 2.1%, while equity dropped by 0.8% on the back of a drop in the foreign currency translation reserve. Net credit facilities also shrank by 0.8%, the drop is believed to be partially related to ARBK’s exposure to heavy burdened companies owned by the Government of Dubai which so far did not reach a rescheduling agreement with its creditors. Most strikingly however was the slide in customers deposits by 2.3%. The decrease in deposits was spread across all sectors including retail, SMEs and corporate. Noting that NIB deposits reached $12,767 million, 41.5% of customers deposits as compared to $12,143 million at year end. • Interest margin narrows by 0.2%. After two year of stable interest margin at 3.3%, interest margin in Q1-2010 dropped to 3.1%, due to market competition. Also net interest income dropped marginally in Q1-2010 by 0.2% • Weakening trend expected to continue in 2010. While it is difficult to anticipate net income for 2010, we believe that if the global economies and financial markets do not recover, most likely ARBK will reflect at best a similar performance to that of 2009. • Higher provisions for credit facilities is needed. To improve credit coverage ratio and bring it up to a 75% level, (cetris peribus). ARBK will have to take into provisions at least $ 240 million for the next two years, or $160 million for the next three years. This provision alone will undermine the overall performance of the bank in 2010. • Interest margin may narrow in 2010. In Q1-2010, interest margin dropped by 0.2% to reach 3.1%. If the same rates continue through out the year then interest revenue is expected to be adversely affected by $ 60 million. Noting that since 42% of customer deposits are non-interest bearing, ARBK’s interest margin will usually narrow as interest rates go down, which is the case in Q1. • Construction and real estate sectors in the Gulf continue to be under pressure. The depressed construction and real estate markets in the Gulf, will most likely spill-over to other sectors in the economy, triggering a further slowdown. Making it even more difficult for ARBK to reverse the declining trends and grow in credit facilities. Thus interest revenue is expected at best to remain at current levels. • Higher provisions for investments in shares globally and regionally may be needed. The recent slide in financial markets may oblige ARBK to grow investment provisions. • Net income may be similar to 2009 levels. The growth of 3% in net income in 1Q-2010 is encouraging, however pressure to grow credit and investment provisions during the year may result in a net income at best similar to 2009 levels. • Consistently high liquidity and capital adequacy levels. ARBK is expected to continue in 2010 to maintain high level of liquid assets and strong capital adequacy ratio.

![Actual 1Z0-962 Exam [PDF] Sample Questions Answers](https://cdn4.slideserve.com/7888383/oracle-dt.jpg)

![1Z0-962 Exam Dumps - Preparation with 1Z0-962 Dumps PDF [2018]](https://cdn4.slideserve.com/7914939/oracle-1z0-962-exam-dt.jpg)

![1Z0-962 Dumps - [2018] Download Oracle 1Z0-962 Exam Questiosn PDF](https://cdn4.slideserve.com/8049143/oracle-dt.jpg)