Download

1 / 18

180 likes | 363 Views

INCOME STATEMENTS. Ag Business Management Spring 1999. Original PowerPoint Created by Mike White Modified by Georgia Agricultural Education Curriculum Office June, 2002. How do you measure performance?. Your school work Basketball team Restaurant Greenhouse. Objectives.

E N D

INCOME STATEMENTS Ag Business Management Spring 1999 Original PowerPoint Created byMike White Modified by Georgia Agricultural Education Curriculum OfficeJune, 2002

How do you measure performance? • Your school work • Basketball team • Restaurant • Greenhouse

Objectives • Describe the importance of income statements. • Identify sources of revenue and expenses. • Given a list of transactions, categorize revenues and expenses.

Importance of an Income Statement • Did the business end the year with a profit or loss? • How much was the profit/loss?

Uses of Income Statement • Summarize revenues & expenses • Determine profit/loss • Explain changes in owner equity

Uses of Income Statement • Calculate financial measures • Support loan application

Summary of Revenue & Expenses • Revenue = cash receipts from product sales or dividends on interest income. • Short or long term asset sales • Inventory adjustments

Examples of Revenues • Cash Revenues • Cash sales • Government payments • Custom work receipts

Examples of Revenues • Non-cash Revenues • Acct. Receivable • Changes in inventory

Summary of Revenue & Expenses • Expenses • operating • interest • non-cash expense adjustment

Examples of Expenses • Cash operating • seed • fertilizer • chemicals

Examples of Expenses • Non-cash expenses • depreciation • changes in unused supp., acct. pay., accrued int., accrued taxes

Net Income • Net income = revenue - expenses • Net income calculated annually • Corresponds with income tax reporting dates

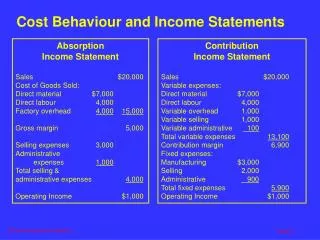

Cash Accounting - Income St. cash revenue - cash expenses = net cash income

Cash Accounting - Income St. net cash income - depreciation = net income from operations

Cash Accounting - Income St. net income from operation • gain/loss on sale of capital assets = net income

Accrual Accounting Income Statement gross revenue - cash expenses - depreciation non-cash expense adjustment = net income from operation

Accrual AccountingIncome Statement net income from operations • gain/loss on sale of capital assets = net income