Download

1 / 14

140 likes | 276 Views

Income Statements. A2 Business Studies. Aims & Objectives. Aim: Understand income statements Objectives: Define income statements Explain the components of income statements Analyse operating and gross profit margins Evaluate the quality of profits.

E N D

Income Statements A2 Business Studies

Aims & Objectives Aim: • Understand income statements Objectives: • Define income statements • Explain the components of income statements • Analyse operating and gross profit margins • Evaluate the quality of profits

Standard Life PLC Income Statement 2009/2009 • What do you think the financial objectives of Standard Life PLC are? • Do you think the performance of Standard Life PLC has improved or deteriorated between 2008-2009?

Income Statement Definition: • A financial document that summarises a businesses trading activity and expenses to show whether it has made a profit or a loss. • Found in the annual report.

Income Statement Definition: • A financial document that summarises a businesses trading activity and expenses to show whether it has made a profit or a loss. • Found in the annual report.

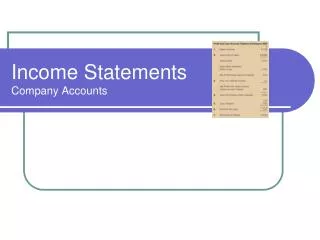

Income Statement of Ted Baker PLC for the 52 Weeks ending 27 January 2007

Activities: • Using the above income statement, calculate the operating profit margin and gross profit margin for Ted Baker Plc. • What do these figures show you? • How significant do you think the Ted Baker brand name is in achieving the gross profit margin?

Activities: • Complete the below Income Statement of Ted Baker PLC for 2007. • Calculate the operating profit margin and gross profit margin for Ted Baker Plc. • Has Ted Baker become more profitable over time or less profitable? • What reasons may there be for this? Between 2007 and 2008 the minimum wage increased in the UK.

Profit Quality Looks at how sustainable profits are. What percentage is from routine day-to-day activity as apposed to non-routine activity (selling off assets).

High Quality Vs Low Quality High Quality Low Quality Difficult to repeat One-off profits usually caused by sale of assets Shareholders need to adjust reported profit to assess what the likely profit is for next year. • Profit which can be repeated • Not reliant on one-off profits • Shareholders can have some confidence in the profit trend

Profit Utilisation • How profit is being used. • Whether it is being ploughed back into the business or distributed to shareholders.

Plenary • Define income statements • Explain gross profit margin and operating profit margin. • What does profit quality mean? • What factors may affect a decreasing Operating Profit Margin over time?