Download

1 / 36

390 likes | 416 Views

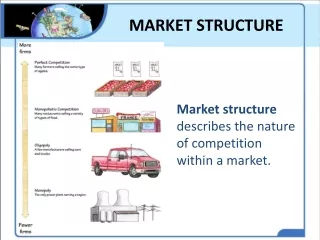

Market Structure. Perfect Competition. Market Structure – The important features of a market , including the number of buyers and sellers , product uniformity across sellers, ease of entering the market, and forms of competitors. Perfect Competition. Perfect Competition

E N D

Perfect Competition • Market Structure – The important features of a market, including the number of buyers and sellers, product uniformity across sellers, ease of entering the market, and forms of competitors.

Perfect Competition • Perfect Competition • Many buyers and sellers – no one individual can control the price

Perfect Competition • Firms produce a standardized product • Commodity – a product that is identical across producers

Perfect Competition • Buyers are fully informed about the price, quality, and availability of products, and sellers are fully informed about the availability of all resources and technology.

Perfect Competition • Firms can easily enter or exit an industry.

Perfect Competition • The best example of perfect competition is agricultural products. There are so many buyers and sellers that no single buyer or seller can influence the price. • “In perfect competition, there is no competition.”

Monopoly • A monopoly is the sole supplier of a product with no close substitutes.

Monopoly • Monopolies have a lot of market power. • Market power – the ability of a firm to raise its price without losing all sales to rivals. • In perfect competition firms have no market power.

Monopoly • A monopolized market has high barriers to entry, which are restrictions on the entry of new firms into an industry. • Legal restrictions – Entry may be illegal (in certain states only the government can sell alcohol) or restricted using licensing (you must obtain a license to be a doctor).

Monopoly • Economies of scale – Forces may reduce a firm’s average cost to produce goods as the firm’s size or scale increases in the long run. In other words, one firm can make goods more efficiently than multiple firms. • Example – The electrical grid

Monopoly • Control of essential resources – Example: China has a monopoly in supplying pandas to world zoos. The US rents Pandas from China for 1 million dollars a year.

Monopoly • Monopolists may not earn a profit – If there is no demand, there will be no profit. Many people have patents for goods that don’t sell.

Monopoly • True Monopolies are rare – Profitable markets draw competitors and substitutes even if barrier to entry is high. Also, technology changes can alter the ability for a monopoly to last. Example – Railroads had a monopoly on shipping goods but that monopoly ended when trucking began.

Monopoly and Efficiency • Competition forces firms to be efficient – to produce the maximum possible output from available resources – and to provide the product at the lowest available price.

Monopoly and Efficiency • Monopolies can charge a higher price and therefore do not have to be as efficient. • Monopolies may have too much influence on the political system. • Monopolies generally lack innovation and waste resources.

Monopoly and Efficiency • However, monopolies aren’t all bad • Due to economies of scale, monopolies may be able to offer goods cheaper because their cost is lower than if multiple firms offered the good or service

Monopoly and Efficiency • Government can force monopolies to lower prices or monopolies will keep prices low to avoid government regulation • Monopolies may keep the price low to prevent competition.

Monopolistic Competition • This market structure contains elements of both monopoly and perfect competition • Companies can influence prices because products are differentiated but barriers to entry are low

Monopolistic Competition • Product differentiation • Physical differences – some cars are boxy, some angular • Location – fast food is everywhere, that super tasty hole-in-the-wall restaurant only has one location • Services – delivery vs no delivery for food • Product image – Ipods seen as sleek and cool

Monopolistic Competition • Product differentiation costs more for firms so the products cost more. Some argue that product differentiation can be too artificial however others argue that consumers are willing to pay a higher price for choices.

Oligopoly • This market structure dominated by just a few firms. • Examples: markets for steel, oil, cars, breakfast cereals, and tobacco.

Oligopoly • Firms are interdependent. They know their actions affect the other firms in the market. • Oligopolies usually occur because of barriers to entry and economies of scale.

Oligopoly • Oligopolies may try to collude – agree to divide the market but fix the price • A group of firms that collude is called a cartel. Cartels typically produce less, charge more, earn a higher profit, and try to block the entry of other firms. • Example: OPEC – Organization of the Petroleum Exporting Countries

Oligopoly • Collusion and cartels are illegal in the United States • Cartels can dissolve if any of the members cheat and offer the product for a lower price.

Antitrust • If left alone, firms may try to become monopolies so the government institutes antitrust laws. These laws try to promote competition and prevent monopolies.

Antitrust • Companies may try to eliminate competition through mergers • Merger – the combination of two or more firms to form a single firm • Antitrust officials must approve a merger before it can happen

Antitrust • Flexible mergers – The government in recent years has allowed mergers if the firms will become more efficient or better able to compete with other large companies.

Antitrust • Some natural monopolies occur such as electricity transmission or a subway systems. These monopolies may be desirable but they are also regulated.

Increased Competition in the United States • Antitrust activity – Government has prevented many mergers

Increased Competition in the United States • Deregulation – Government has reduced regulation of some markets such as trucking, airlines, and telecommunications. This has increased competition.

Increased Competition in the United States • International trade – More foreign trade increases competitors.

Increased Competition in the United States • Technological change – Technology lowers barriers to entry and has made it easier for customers to compare different products.