Download

1 / 17

170 likes | 326 Views

This comprehensive guide to corporate finance addresses long-term investments, raising money, and managing cash flow for businesses. Learn about Capital Budgeting, Capital Structure decisions, net working capital, financial markets, stocks, bonds, investment environment, debt, equity, and corporate governance. Understand the relationship between debt and equity, financial markets, and agency costs in corporate finance.

E N D

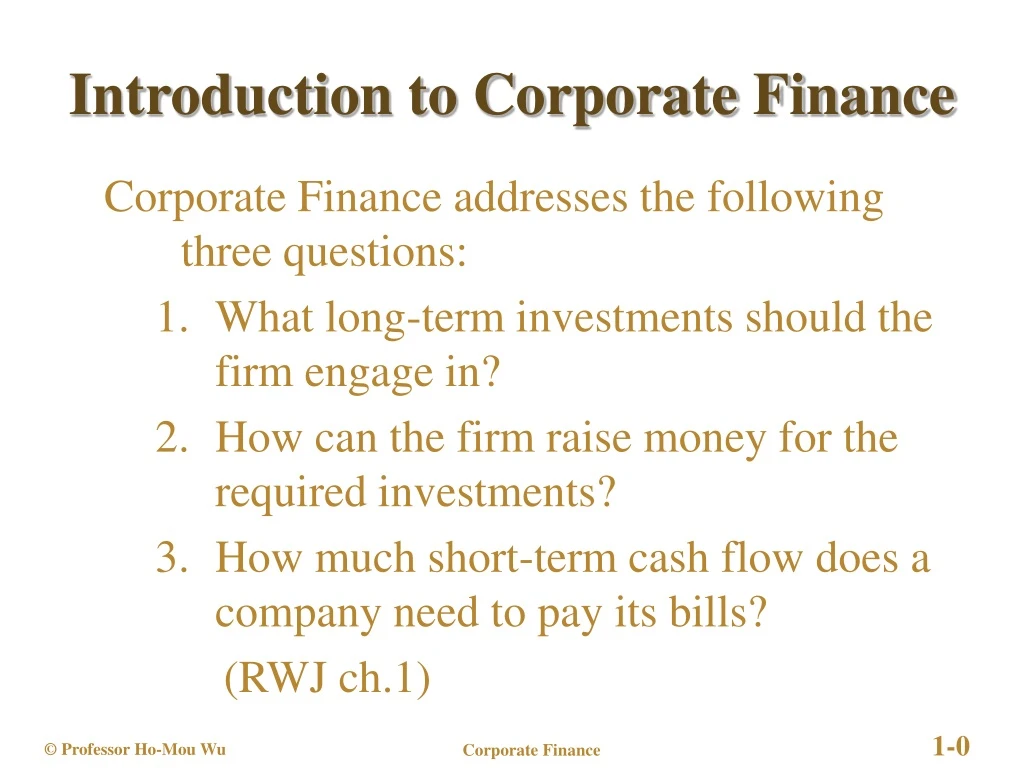

Introduction to Corporate Finance Corporate Finance addresses the following three questions: What long-term investments should the firm engage in? How can the firm raise money for the required investments? How much short-term cash flow does a company need to pay its bills? (RWJ ch.1)

Total Value of Assets: Total Firm Value to Investors: Current Liabilities Current Assets Long-Term Debt Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity The Balance-Sheet Model of the Firm

The Balance-Sheet Model of the Firm The Capital Budgeting Decision (Investment Decision) Current Liabilities Current Assets Long-Term Debt What long-term investments should the firm engage in? Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity

The Balance-Sheet Model of the Firm The Capital Structure Decision (Financing Decision) Current Liabilities Current Assets Long-Term Debt How can the firm raise the money for the required investments? Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity

The Balance-Sheet Model of the Firm The Net Working Capital Investment Decision (Financial Decision) Current Liabilities Current Assets Net Working Capital Long-Term Debt How much short-term cash flow does a company need to pay its bills? Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity

25% Debt 70% Debt 30% Equity 75% Equity Capital Structure The value of the firm can be thought of as a pie. The goal of the manager is to increase the size of the pie. 50% Debt The Capital Structure decision can be viewed as how best to slice up a the pie. 50% Equity If how you slice the pie affects the size of the pie, then the capital structure decision matters.

Firm Financialmarkets Government The Firm and the Financial Markets Firm issues securities (A) Retained cash flows (F) Investsin assets(B) Cash flowfrom firm (C) Dividends anddebt payments (E) Short-term debt Long-term debt Equity shares Current assetsFixed assets Taxes (D) The cash flows from the firm must exceed the cash flows from the financial markets. Ultimately, the firm must be a cash generating activity.

Financial Markets • Primary Market • When a corporation issues securities, cash flows from investors to the firm. • Usually an underwriter is involved • Secondary Markets • Involve the sale of “used” securities from one investor to another. • Securities may be exchange traded or trade over-the-counter in a dealer market.

Stocks and Bonds Money Primary Market Secondary Market securities money Financial Markets Investors Firms Bob Sue

Capital Structure :Debt and Equity • The basic feature of a debt is that it is a promise by the borrowing firm to repay a fixed dollar amount of by a certain date. • The shareholder’s claim on firm value is the residual amount that remains after the debtholders are paid. • If the value of the firm is less than the amount promised to the debtholders, the shareholders get nothing.

Payoff to debt holders Payoff to shareholders $F $F Value of the firm (X) Value of the firm (X) Debt and Equity as Options If the value of the firm is more than $F, debt holders get a maximum of $F. If the value of the firm is less than $F, share holders get nothing. $F If the value of the firm is more than $F, share holders get everything above $F. Debt holders are promised $F. If the value of the firm is less than $F, they get the whatever the firm if worth. Algebraically, the bondholder’s claim is: Min[$F,$X] Algebraically, the shareholder’s claim is: Max[0,$X – $F]

Combined Payoffs to debt holders and shareholders Payoff to shareholders Payoff to debt holders $F Value of the firm (X) Combined Payoffs to Debt and Equity If the value of the firm is less than $F, the shareholder’s claim is: Max[0,$X – $F] = $0 and the debt holder’s claim is Min[$F,$X] = $X. The sum of these is = $X $F If the value of the firm is more than $F, the shareholder’s claim is: Max[0,$X – $F] = $X – $F and the debt holder’s claim is: Min[$F,$X] = $F. The sum of these is = $X Debt holders are promised $F.

Corporate Governance Separation of Ownership and Control Board of Directors Management Debtholders Shareholders Debt Assets Equity

Asymmetric Information and Agency Costs • There is asymmetric information between shareholders and managers. • How to induce managers to act in the shareholders’ interests ? • The shareholders can devise contracts that align the incentives of the managers with the goals of the shareholders. • The shareholders can monitor the managers behavior. • (Agency Cost) This contracting and monitoring is costly.