Download

1 / 14

140 likes | 279 Views

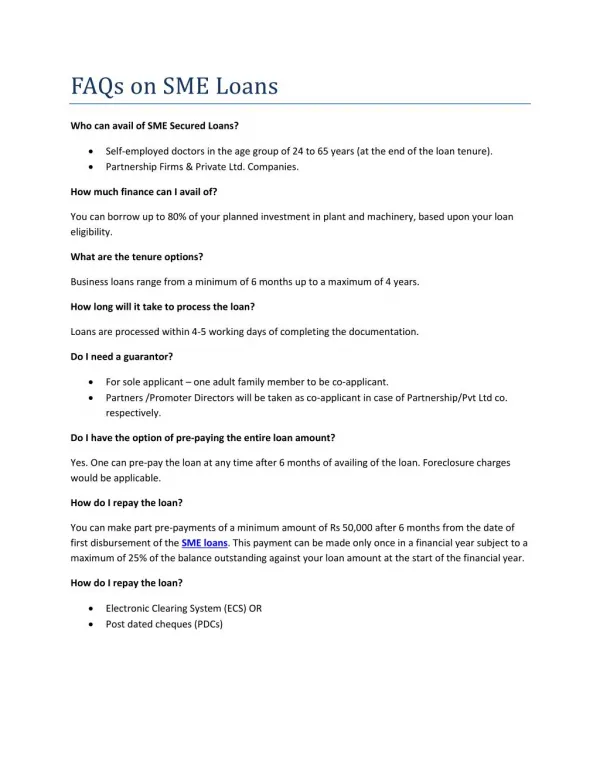

FAQs on. Revision of PRBS. November 18, 2014. How much more pension will I get in the revised scheme Everyone will get more pension in the revised scheme because of the following reasons:

E N D

FAQs on Revision of PRBS November 18, 2014

How much more pension will I get in the revised scheme Everyone will get more pension in the revised scheme because of the following reasons: The existing PRBS is styled as a “self-contributory” scheme. This is only encouraged and supported by the Management. The revised scheme will receive additional Direct contribution ( up to 15% of Basic + DA) from the Management, permitted by the DPE guidelines. This is part of the Pay Revision package (w.e.f. 2007). This significant additional contribution will be directly credited into the individual’s account in the books of the PRBS trust, It will also accrue interest based on investments made by the trust and will become payable on retirement / other specified situations There is no ceiling of eligible pension in the revised scheme, unlike the ceiling of 50% of notional pay in the existing PRBS FAQs on Revision of PRBS November 18, 2014

How safe is my money in the revised scheme? What is the guarantee for my pension benefits? In the Defined Contribution model, the pension corpus of each individual is as safe as CPF. At any given point of time, the assets of the trust will be equal to the sum of Corpus due (liability) to all the members of the pension scheme. Investments of the trust are governed by guidelines of the Government and is audited. Risk of losing money is almost zero. However, pension is based on the Balance Corpus in the account of the Beneficiary. The amount of Pension is not Defined in terms of Pay and hence not guaranteed. Repeat. Pension in terms of Pay is not guaranteed, but pension based on Balance Corpus available is safe and assured. FAQs on Revision of PRBS November 18, 2014

Will this revision be applicable retrospectively or prospectively? This revision of pension benefits is planned to be effective from 1.1.2007, the date from which the DPE guidelines (for additional direct contribution up to 30% of Pay) became applicable FAQs on Revision of PRBS November 18, 2014

Where is the source of money for the additional pension? In the DB model, the additional amount (Difference between eligible corpus and actual contribution) comes from the contribution of future retirees and the support extended by management in the form of grants, enhancement of monetized value etc. There is uncertainty in this form of support. In the DC model, the company contributes directly upfront to the pension corpus of every individual ( up to 15% of Pay as per DPE guidelines). In addition, individuals also contribute to increase the available corpus for a higher pension. Table below gives the amount contributed at four different salary points for the years 2007 – 2013 FAQs on Revision of PRBS November 18, 2014

How does our Pension scheme compare with the pension schemes of other PSUs, especially IOC? There are several differences between our scheme and the schemes of other PSUs. IOC has been giving pension at 40% of Pay (Basic + DA) for a full service of 32 years from beginning (Nov 1987), whereas in PRBS, pension benefits are worked out on the basis of notional pay, which is less than actual Pay. IOC computes pension as 1.25% of pay for each year of service, whereas we have a more complex formula for computation. Pension for the discounted RPS is computed with the salary of 1991 with an accrual rate of 1.21 per year of RS. Pension for the escalated RFS is computed with the notional salary on DOR, with an accrual rate of 1.6% per year of RS. The increase in pension pay out with time in the case of IOC appears to be more linear than in the case of ONGC. This may be the result of the court cases and forced interventions to moderate the pay out of pension. FAQs on Revision of PRBS November 18, 2014

FAQs on Revision of PRBS The above table represents a computed case with minimum assumptions at the middle management level (E4/E5). It shows that the Pension pay out from PRBS of ONGC was much less than the pension pay out from SABF of IOC till 2006. Further, the pay out in the case of ONGC was stepped up by 43% (in Corpus) in 2007 by the MOU signed in April 2007. Now, this is further proposed for a steep increase in 2007 November 18, 2014

IOC has not attempted to step up the pension benefits on the conversion date ie., 1.1.2007. As a net result, the pension pay out on both sides of the conversion date is not drastically different. Proposal of ONGC is to make up for the difference in Pension and further to step it up to the level of 50% of Basic Pay ( This should actually be Pay, as ‘Total Pay’ and ‘Basic Pay’ as on 1.1.2007 is the same) In the case of ONGC, there will be a sharp shoot up of benefits after the conversion date. This happens because of 3 factors (1)The pension for the RPS is now to be computed based on the revised salary of 2007 in place of the salary of 1991, (2) Pension for RFS till 2007 is now to be computed differently, using the revised pay of 2007 as against the notional pay. ( pre-revised pay was about 50% more than the notional pay as on 1.1.2007. Revised pay has an additional fitment benefit of 30%, compensation for 50% DA merger and an annual increment of 3%) (3)Use of a target pension rate of 50% of revised Basic as on 1.1.2007 FAQs on Revision of PRBS November 18, 2014

Also, the individual contribution in the case of IOC is only 2% and this is proposed as 3% in the case of ONGC. IOC has worked out the additional direct contribution (as permitted by DPE guidelines) to be 14.62%, whereas this is proposed as 15% till 31.3.2013 by ONGC. ONGC has also proposed to retain the additional contribution from the individual members ( equivalent to the monetized value), thereby further increasing the individual contribution Though the pension planned in the case of ONGC is higher under the DC model (not guaranteed), there will also be significant higher ‘Individual Contribution’ compared to other PSUs. Pension benefits in the case of PRBS as well as similar schemes of other PSUs will tend to converge in the long run, as the additional contribution in the DC model begins to dominate. Overall, it may not be reasonable to justify our proposal on the basis of comparison with the pension schemes of IOC or any other PSU. It should be justified independently, on its own merits FAQs on Revision of PRBS November 18, 2014

Are there significant changes in the way pension benefits will be computed in the Revised Scheme? Yes. In the existing DB model of PRBS, the pension benefits are computed on the basis of non-contributory Reckonable Past Service till the date of joining PRBS and the contributory Reckonable Future Service from the date of joining PRBS till DOR. Pension benefit for the RPS is computed with the salary of 1991/1995, the actual date of joining PRBS and the Pension Benefit for the RFS is computed based on the Notional Salary that is escalated by 8% every year since 1995. In this model, the difference in career growth beyond 16.11.95 does not affect the Pension Benefits. In the proposed revision, the Pension Benefit for both the RPS and the RFS will be computed on the revised salary as on 1.1.2007. This means that (1)Members with higher RPS will draw more benefits and (2)Members who have had a better career progression after 16.11.95 will draw more benefits. In addition, a new factor based on the balance service as on 1.1.2007 has been introduced in the form of Discounting. This reduces the benefits from the existing DB fund considerably to those with a younger age profile, even though their actual contribution and the length of service may be the same. FAQs on Revision of PRBS November 18, 2014

What is the actual concern of ASTO with regard to this revision of PRBS ? Though the scheme is beneficial overall, there are serious concerns about the finer details. It has been estimated by ASTO’s committee on PRBS that the pension that is likely to be available for future retirees is likely to be only in the range of 30% and this is dependent on inflation. Higher the inflation, lesser the pension benefits. When such is the case, it is not reasonable to plan for 50% pension pay out as on 1.1.2007. For retirees of 2007 and soon after, the bulk of the funds comes only from the existing DB fund. The design criteria needs to be revisited and moderated to about 35% to 40% of Pay, so that everyone will be able to avail similar pension benefits. FAQs on Revision of PRBS November 18, 2014

Use of ‘Discounting’ in computing the liability of the PRBS trust to each individual member as on 1.1.2007 has led to a huge distortion and denial of benefits to a large cross section of ONGCians in the younger age profile. This will actually translate into disproportionately reduced pension benefits to all these members for their service till 1.1.2007 The proposed changes result in reduced weightage to the actual service and actual contribution to the pension fund as compared to the existing scheme. Employees with similar date of recruitment, level, length of service and contribution to the fund as on 1.1.2007 are likely to be discriminated heavily based on their ‘Age Profile’ (ie., balance service as on 1.1.2007). Only the broad picture of the proposed changes are being shared and the justification for the proposed changes is only on the basis of select examples and comparison with pension schemes of other PSUs. This non-transparent approach is very risky and not reasonable. FAQs on Revision of PRBS November 18, 2014

The discounting rate used is 9.5% which is above the average returns earned by the PRBS trust as also the CPF interest rate. This rate is not likely to be sustained in the long run. It is common knowledge that Government is making every effort to reign in inflation and in a low inflation regime, the average rate of return will fall. This means that the liability of the trust to individual members has been underestimated and this difference is being made available as additional benefit to members retiring in 2007 and soon after. The only way to overcome this uncertainty is to totally do away with the discounting principle. When the notional salary or the actual salary of 1.1.2007 is used to compute the liability for service up to 1.1.2007, the liability should be actual as on 1.1.2007. The liability of the trust to the individual as on the date of retirement, even for the service up to 1.1.2007, should be computed using the salary as on the date of retirement and the service length up to 1.1.2007 Minimum assured pension for cases of Death / TPD is planned to be removed in the proposed scheme. ASTO has desired that this feature should be retained and the cost can be distributed to all members. FAQs on Revision of PRBS November 18, 2014

Has ASTO proposed any solution to the Current Deadlock? Yes. There are different alternatives suggested. (1)The best option would be to drop the Discounting method for computing the liability to members as on 1.1.2007. The % pension as target benefit has to be reworked in this case (2)The minimum guaranteed benefit from the existing DB fund (liability as on 1.1.2007) should be defined as 10% of actual contribution per year of Reckonable Service to all members in addition to their actual contribution and interest earned on this contribution. To explain, this will mean a minimum guaranteed benefit of 50%, 100%, 150%, 200% etc. of actual contribution for members who have a RFS of 5, 10, 15, 20 years etc. as on 1.1.2007. This is benchmarked against the estimated benefit of around 1500% for members retiring in 2007 with RS of 33 years. Accordingly, the % pension as target benefit can be reworked (3)The minimum assured pension in cases of Death /TPD should be retained. This could be set as 40% of last drawn pay and the additional corpus, wherever required, shall be provided by members through a fair sharing formula. Or, this can be adjusted against the annual earnings of the trust on its investments before giving credit to the individual members FAQs on Revision of PRBS November 18, 2014