Download

1 / 45

450 likes | 573 Views

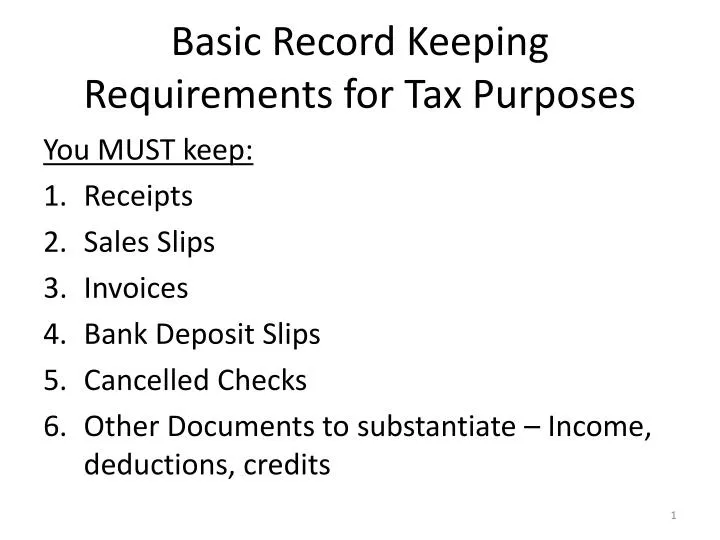

Basic Record Keeping Requirements for Tax Purposes. You MUST keep: Receipts Sales Slips Invoices Bank Deposit Slips Cancelled Checks Other Documents to substantiate – Income, deductions, credits. Adequate and complete Recordkeeping. Explain items on your income tax return.

E N D

Basic Record Keeping Requirements for Tax Purposes You MUST keep: • Receipts • Sales Slips • Invoices • Bank Deposit Slips • Cancelled Checks • Other Documents to substantiate – Income, deductions, credits

Adequate and complete Recordkeeping • Explain items on your income tax return. • Source documents are your proofs of your deductible expenses • Log or diary for deductions for travel, transportation, entertainment, business gifts • Time and place

IRS Publication 583 Starting a Business and Keeping Records Order Publications at www.irs.gov

How long should records be kept? • 3 years after the return is due for filed, or, • 2 years from the date the tax is paid, whichever is later

Indefinitely! • Change your method of accounting • Property – basis of original or replacement property

Employee Records • 4 years after the date on which the tax return becomes due or the tax is paid, whichever is later. • Publication 15 Employer’s Tax Guide

Separate Checking Accounts • IRS recommend opening a separate checking account for your business.

Accounting Methods Cash Method – • Report all income in the year you receive it • Deduct expenses only in the tax year in which you pay them

Accrual Method • Report income in the year you earn it regardless of when you receive the payment • Deduct expenses in the tax year you incur them, regardless of when you pay them • Business that have inventory for sale to customers must use an accrual method for sales and purchases

Publication 538 Accounting Periods and Methods

Accounting Computer Software Quickbooks – www.journeyed.com www.quickbooks.com Free Trial Peachtree – Staples (rebate)

Sole Propietor • Schedule C or C-Ez • Form 1040 • Schedule SE – Self Employment Tax

Pub 541 Partnership • Schedule K-1 • Form 1040 • Form 1065

LLC • One person – Sole proprietor • 2 or more - Partnership

Form 8832 Entity Declaration • 2 or more people --- Partnership • 1 person business ----Sole proprietor

Paid Preparer • You are legally responsible for your tax return • Avoid preparers who claim they can obtain larger refunds than other preparers • Avoid preparers who base their fee on amount of your refund • Ask questions and get references • Person’s credentials • Never sign a blank tax return • Will the preparer be around months or years from now?

Deductions Everyday costs of doing business: • Utilities • Office supplies • Licensing Are deductible

Travel, Transportation, Entertainment Traveling overnight away from home: • Public Transportation • Operating and maintaining your car • Meals, Publication 463 (per diem rates) • Lodging • Keep your receipts!

Transportation • Getting from one work place to another in the course of your business • Not away from home

Business Entertainment Expense • Necessary – you can proof it • Taking your clients out to lunch. • Publication 463, 50% limit

CAR (all business) • Use for business only 100% • Full cost of operating it • Deduct it all

CAR (both business & personal) • Divide expenses on the basis of mileage • Compute a business percentage • Standard Mileage Rate – reduce burden record keeping. • Business mileage x standard rate, must use the mileage rate the first year. • Later years you can alternate. • Actual business expense. • Parking fees and tolls are deductible

Business use of home • Maintaining your home as a business expense • Regular use of your home. • Mortgage interest • Insurance • Utilities • Repairs • Depreciation or Rent

Other Requirements • Store inventory • Child Care Business • Form 8829 & Form 1040 • Publication 587 Business use of your home

Start Up Costs • Expense to set up your business • After a 180 months period to deduct • Publication 535

Depreciation • Used in the business • Useful life longer than 1 year • Wears out, becomes obsolete • Deduct over a number of years Can not depreciate land

Method • MACRS • Modified Accelerated Cost Recovery Systems

Section 179 Deduction • You can to recover all or parts of the cost of certain qualifying property up to a limit by deducting it in the year you place the property in service • Disadvantage : cannot take Earned Income Credit and other credits, full exemption and deductions • Publication 946 How to depreciate property • Publication 535 business deduction

Self Employment Tax • SS • Medicare • When you are employed your employer paid half and you paid half • When you are Self employed, you pay all

Estimated Tax • Estimated Tax • Use form 1040 ES Worksheet to figure amount of Estimated Tax

Regular use test • Occasional or incidental

Operate your business out of your home • Home: house, apartment, garage, condo, mobile home, studio, barn, greenhouse

Qualifying for a deduction • Exclusive • Regular • For your business The business part of your home must be one of the following: • Principal place of business • Place where you meet clients • Separate structure

Exclusive Use Test • Use an area for business only • Room or separate identified space

Exception to the Exclusive Use Test • Inventory or product storage • Day-care facility

Principal Place of business • Exclusively and regularly for administrative or management activities • No other fixed location

What are Administrative/Managerial Activities? • Billing • Books and records • Ordering supplies • Appointments • Forwarding orders or writing reports

Business Percentage 2 methods • Area Method • Number of rooms method

Area Method • Area Method (square footage) Area used by business Total area of your home Example: Office 240 square feet Home 1200 square feet Form 8829

# of rooms method • Number of rooms Method. The number of rooms used for business The total number of rooms • You can use this method if the rooms in your house are about the same size. • Form 8829

Types of Expense • Business activity: Expenses related to the business activities are fully deductible advertising, taxes, car, salaries, travel • Use of home: • Direct: painting, repair in area of business • Indirect: hoa • Unrelated:

Expenses • Landscaping • Painting business office • Utilities • Repair to roof of house • Repair to business office • Painting of family room

expense • Real estate tax • Mortgaget interest • Insurance • Rent • Repairs • Utilities an services • Depreciation • Carry forward to future years • Pub 587

IRS Training • www.irs.gov • Click on the Business tab • On the left click on the Starting a Business link • At the bottom click on the Online Learning and Education Products bullet • Click on the Small Business/Self Employed Virtual Small Business Tax Workshop

Order Publications IRS (free) How to order publications: • www.irs.gov • Click on the Business Tab • On the right, click on the Forms and Publications link. • In the Order section, click on Forms and Publication by U.S. Mail • In Search box type in the Publication you want to order. Continue with the ordering process.