Download

1 / 21

260 likes | 497 Views

Lecture IV Monetarism and Milton Friedman. Attack on Keynesianism. The first major challenge to Keynesian ideas came from members of the so-called monetarist school that believed that the principal source of economic instability was monetary fluctuations

E N D

Attack on Keynesianism • The first major challenge to Keynesian ideas came from members of the so-called monetarist school that believed that the principal source of economic instability was monetary fluctuations • In this regard, monetarists not only challenged Keynesian ideas but the classical model as well, which believed that money was neutral and that the economy was fundamentally stable with occasional, brief deviations from full-employment equilibrium • In this one respect, Keynesians and monetarists see eye to eye; beyond that, there is little on which the two agree

Monetary Economics and James Tobin • Monetarism is distinct from monetary economics, which deals more generally with the effects of changes in the money supply on real and nominal economic variables • The “father” of monetary theory is James Tobin of Yale University • Despite his belief in the power of money in the economy, Tobin was and still remains a leading Keynesian and believes that discretionary fiscal policy is the most efficient way to deal with recessions and depressions.

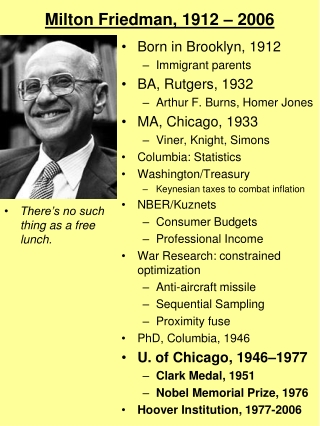

Milton Friedman • By contrast, Milton Friedman, perhaps the most influential economist in the second half of the 20th century, believes that money, and only money, is the source of all major economic swings • His most convincing evidence of this proposition lies in his Monetary History of the United States,1867-1960, which he co-authored with Anna Schwartz • In the Monetary History, Friedman and Schwartz show how every major economic expansion and contraction was accompanied by a corresponding expansion or contraction, respectively, of the U. S. money supply

The Fed and the Great Depression • While this is not proof that these monetary changes caused the swings in the economy, it does provide evidence that these episodes could not have occurred without the corresponding monetary swings • Thus, the monetary authority, had it acted counter-cyclically rather than pro-cyclically, might have avoided these episodes • For a long time many economists have blamed the Fed for its weak response to the financial crisis in not providing enough liquidity to the market in 1930 • Some claim that had Benjamin Strong not died in 1928, the Great Depression might have been avoided; we’ll never know • Strong was the former Chairman of the Federal Reserve Bank of New York and most influential member of the Fed

Friedman and Schwartz on the Great Depression The following is from Snowdon and Vane Even more controversial was the reinterpretation of the Great Depression as demonstrating the potency of monetary change and monetary policy. Friedman and Schwartz argued than an initial mild decline in the money stock from 1929 to 1930 was converted into a sharp decline in a wave of bank failures which started in late 1930. Bank failures produced an increase in both the currency-to-deposit ratio, owing to the public’s loss of faith in the banks’ ability to redeem their deposits, and the reserve-to-deposit ratio, owing to the banks’ loss in faith to the public’s willingness to maintain their deposits with them. … the consequent decline in the money stock was further intensified by the Federal Reserve System’s restrictive action of raising the discount rate in October 1931, which in turn led to further bank failures.

Quantity Theory of Money • The starting point of monetary economics and monetarism is the quantity theory of money and its equation of exchange MV = PY, where M is the nominal money supply, usually defined as broadly as possible to include all money that can be used easily in market transactions • P is the “aggregate” price level, where P is the price of whatever Y measures • Y is final output of goods and services, or GDP • V is the “velocity” of money; this needs to be defined so as to be the velocity of money in carrying out the transactions define by Y

More on money velocity • Irving Fisher, in order to simplify defining V, used the equation MV = PT, where transactions include all transactions, for final and intermediate product • A natural definition of V, therefore, is V = PY/M • A tenet of monetarism is the stability of V • On this point Tobin disagrees with monetarists • Like Keynes, Tobin believes that V may be very unstable over the business cycle, increasing during periods of an over-heated economy and contracting during contractions; that is, V is very pro-cyclical • Only through aggressive action can the monetary authority maintain monetary stability • Recent economic events have demonstrated just how unstable money velocity can be • This fact alone has diminished the influence of the purest form of monetarism

The monetarist argument against Keynesianism • Friedman was always very wary of the intrusiveness of government into economic affairs and argued vehemently for economic freedom and his 1990 Free to Choose: A Personal Statement speaks of his libertarian views • In addition to his concerns about the loss of economic freedom, Friedman also felt the discretionary fiscal policy suffered severe effectiveness constraints due to a variety of lags, which he call recognition, action, and effect lags

Recognition Lag • The first is the recognition lag; it often is not until months into a recession, for example, that policy makers are even aware of the problem and many more months until its magnitude can be determined • For example the National Bureau of Economic Research, which dates the stages of the business cycle, requires two quarters (not months), of negative real GDP growth before declaring a recession; it’s often not until a year into a recession that one is declared • Revisions of macroeconomic data can be substantial and occur for months after the quarter of interest • The most recent U. S. recession was declared over as of June 2009; this determination was announced in September 2010!

Action Lag • Even after the recession has been declared, the legislature must act on this information • Even if the legislators agree that action must be taken, and that’s a big IF, it may still be months before legislation is drafted, voted on, and finally signed into law by the executive • And even then, the time from the authorization of funds and their final expenditures will be many months, even years later • One of the main complaints about the U.S. stimulus package is how long it took to spend the money; there’s still some left over almost two years after passage of the bill

Effect Lag • Even after funds have been allocated and spent, the economy requires time for the complete effects to be felt • The Keynesian multiplier effect is not instantaneous but requires time for the secondary impacts to occur • By the time the entire process has run its course, the economy may be well into its recovery phase, just in time for the fiscal stimulus to expand the next “bubble”

Effectiveness of Monetary Policy • By contrast, monetarists see monetary policy as more direct and able to avoid the action lag • Inflation data, for example, are available monthly • The Fed meets about once a month and can take immediate action through the Federal Reserve Banks to lower borrowing rates and to purchase government securities (open-market operations) • The effect lag is still a problem, probably about the same as for fiscal policy; Friedman estimated between 9 and 18 months for money to work its way fully into the economy • Because of this last problem, monetarists are consistent in their arguments against the use of discretionary policy, both fiscal and monetary

The Monetarist Rule • Friedman argued that since discretionary government policies to regulate the economy may have adverse effects because of timing and intensity, the Fed should follow a constant monetary growth policy • He settled on a 3% growth in the money supply arguing that if real GDP growth is in the neighborhood of 2.5% to 3%, this will maintain stable prices or very moderate inflation • The Fed has in fact been operating on monetarist principles, but has often erred in attaining the desired growth rate of the money supply • Fed Chairs have frequently admitted that they under or overestimated the economic stimulus provided

How to target money growth • The central bank is unable to actually observe the money supply at any given time • What it does know is the size of the monetary base or “high-powered” money it has created • How the monetary base actually translates into “money” depends on both banks and the public • If banks do not lend the reserves (recall F&S on the increase in the reserve-to-deposit ratio in 1930) for fear that loans will not be repaid, or if the public desires to hold more currency, then the money supply may actually contract despite the good intentions of the Fed • Today the existence of deposit insurance mitigates the public’s fear of bank failure, but low interest rates may still lead to higher currency holdings

Interest rate targeting • In the absence of direct knowledge of the actual money supply, the Fed often uses some interest rate target to assess market liquidity • Most often it uses the shortest of these rates, and the one over which the Fed has most control, the Fed Funds rate, which is the rate at which member banks can borrow overnight • The short rates, however, may or may not be in synch with longer rates, which are more important in investment decisions • Today despite considerable “quantitative easing” of money, long rates have not risen, a signal that the market does not foresee inflation in the near or distant future • In any event, interest rate targeting becomes useless at the lower bound, where we are right now

Other targeting mechanisms • A relatively new proposal by Lars Svensson and promoted by Scott Sumner is to target nominal GDP, or NGDP targeting • Let’s suppose the central bank wants a 5% growth in PY; this can be divided any way between money growth and real output growth • MV = PY can be written in growth rate terms as m + v = p + y, where lower case means growth rate • So if p + y = 5%, we can have p = 3%, y = 2%, which is OK • And if p = 5% and y = 0%, we’re not happy, but at least we’re not in deflation • And if we hit deflation and p = -2%, at least y = 7%, and that’s great!

Rate or level targeting • One issue that arises in NGDP targeting is whether to target the growth rate or level of NGDP • If you target growth at say 5% per year, if you miss by 1%, say p + y = 4%, then next year you again target 5% • If on the other hand you want the level to attain a target for each year, the shortfall of one percent the first year requires a 6% target rate for year 2 • The idea of central bank credibility is greater with level than with rate targeting as the actions will be even more expansionary (larger open market purchases) with level versus rate targeting

Friedman and the Phillips Curve • One of the tenets of Keynesian economics is the idea of a tradeoff between unemployment and inflation; Friedman disagreed with the argument of a permanent and stable relationship between inflation and unemployment • He used the idea of adaptive expectations to argue that over time economic agents would change their behavior as they incorporated inflation into their perceptions • For example, if policy makers believe that the current 6% unemployment rate is unacceptable, they can raise inflation from 0% to 2% and individuals initially increase their work effort as wages rise when firms compete to hire new workers • As workers see the real wage has not increased, and maybe even fallen, they quit their jobs (or new workers decline to work) and the unemployment rate returns to its original rate

Historical reaffirmation • The U. S. stagflation of the late 1970’s confirmed the idea that higher inflation rates could not ward off real OPEC oil price shocks • And the Volcker recession of the early 1980’s demonstrated the pain involved in reducing inflationary expectations • Today, all major central banks accept the idea of inflation targeting to try to avoid the pain that will eventually occur from inflation reduction • Later versions of the natural rate hypothesis actually deny even a short-run Phillips curve as economic agents become increasingly aware of the likely actions of plicy makers • This results in a vertical Phillips curve with unemployment stuck at the natural rate barring unanticipated demand shocks • This story will be part of the next lecture on rational expectation