Download

1 / 20

370 likes | 1.5k Views

Chapter 8 : Fee-Based Retail Financial Services. Credit Card, Debit Card, Smart Card & Barter Card. Credit Cards. The term credit originated about 3000 years ago The first credit card was the Charge Card launched by Diners Club in 1950 in USA

E N D

Chapter 8 : Fee-Based Retail Financial Services Credit Card, Debit Card, Smart Card & Barter Card

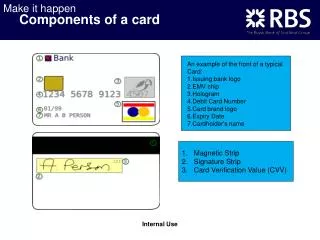

Credit Cards • The term credit originated about 3000 years ago • The first credit card was the Charge Card launched by Diners Club in 1950 in USA • In 1970, the magnetic strip was introduced on the credit cards • Credit cards have three functions: • A means of paying for goods and services; • A means of obtaining cash; • A source of revolving credit. • Today, Visa and Mastercard are the organizations issuing credit cards.

Credit Cards • Types of cards: • Bank-issued cards • Charge cards • JCB Cards • Gold cards • Co-branded cards • Affinity cards • Store cards • Electronic Debit Cards • Telephone cards • Fuel cards • Add-on-cards

Credit Cards • Credit card agreements: • Consensus of the parties (offer and acceptance) • Consideration • Capacity (the parties must be able legally to contract) • Formality (the document must be correct) • Legality (the purpose of the contract must be legal) • Intention to contract (the parties must share the same intention)

Credit Cards • Clauses generally contained in bankcard contracts: • Signature of the cardholder • Agreement to debit the amount spent by the cardholder to his account and pay the amount to the paying bank within a specified period • Daily interest calculation and monthly debit • Agreement by the cardholder to pay a minimum payment each month • Card remains the property of the issuer • Loss of card should be immediately notified to the issuer • Issuer has no liability if the card is not accepted by the supplier

Credit Cards • Credit Card Terms • Annual Percentage Rate • Periodic rate • Variable rate • Free period • Annual Fees • Transaction fees and other charges • Balance computation method for the finance charge • Average daily balance • Adjusted balance • Minimum payment • Previous balance • Two-cycle balances-Issuers

Credit Cards • Other Features • Special delinquency rate • Prohibition to issue unsolicited credit cards • Prompt credit card payment • Refund of credit balances • Errors in the bill • Unauthorised charges • Disputes about merchandise or services • In India, banks like Allahabad Bank, American Express, Andhra Bank, SBI, Bank of India, Bank of Baroda, Citi Bank, HDFC, ICICI, Standard Charted Bank, Axis Bank etc. offer credit cards

Credit Cards • RBI Guidelines on Credit Cards • Minimum net owned fund of Rs.100 crore • Net profit as per last two years audited balance sheet • CRAR of 10% for non-deposit taking NBFCs and 12 to 15% for deposit taking NBFCs • Role of NBFC should be only marketing of co-branded card • Compliance with KFC requirements • The risks of co-branded cards should be transferred to NBFCs • The co-branded credit card account should be maintained by the customer with the bank • NBFC should maintain the confidentiality of the customer’s account

Credit Cards • RBI Guidelines on Credit Cards • Suitable mechanism for the redressal of customer grievances • Legal risk for banks • Fair practices code should be followed • KFC norms and provisions of Prevention of Money Laundering Act should be adhered • RBI guidelines regarding acceptance of public deposits and Prudential norms should be complied with. • NBFC should comply with the terms and conditions stipulated by the bank • RBI can withdraw the permission by giving three months’ notice.

Debit Card • Debit cards are generally known as ATM cards • Unlike credit cards, the cardholder has to maintain sufficient balance in his savings/ current account in order to debit the amount as and when the bill is received • No credit is available in the case of debit cards • The withdrawals in the case of international debit cards will be in the currency of the country where it is put to use. • Debit cards enable the tracking of payment. • Debit cards also save the interest charges. • Debit cards also have daily limits

Debit Card • RBI Guidelines: • Banks with minimum net worth of Rs.100 crore can issue debit cards • No RBI approval is necessary for online debit cards where Straight-through processing is done • RBI approval is necessary for off-line debit cards • The stipulation of minimum net worth of Rs.100 crore is applicable only in the case of off-line debit cards.

Smart Cards • Plastic card embedded with microchip • Data can be stored • Unlike credit/debit cards, the credit balance is transferred to the card • The merchant establishment can debit the payment to the card using a chip reader • The balance will be reduced as and when payments are effected • Recharge is possible through card encoders

Smart Cards • Petro cards/ Loyalty cards are smart cards • Multiple currencies carried in a smart card • Smart card enables multiple uses through a single card • Smart card is extensively used for payment of utilities • Smart cards offer confidentiality and security

Smart Cards • E-cash and Smart Cards • E-cash is an alternative to physical cash • Dispenses with cash electronically • Can be used in out-lets where e-cash is accepted • Five separate currencies can be stored • Customer gets an instant statement • Safer and less expensive than conventional currencies • Benefits like revolving credit, interest-free period etc. are offered • Can spend only upto the value loaded in the card • An electronic wallet is a pocket-sized device with one or two card readers and its own electronic purse, a keyboard, and a screen • Electronic wallet enables transfer of value to and from electronic cash smart cards.

Smart Cards • RBI Guidelines • The guidelines covers all smart card involving electronic payments, ATM cards and cards containing real value in the form of electronic money • No cash withdrawals at the point of sales • Issue of cards should be restricted to customers of good financial standing • Balance in the cards should be considered for calculating the reserve liability • No interest should be paid on card balance

Smart Cards • RBI Guidelines • Security and other aspects • Banks should ensure full security • Issue of unsolicited card is prohibited except in the case of replacement of an existing card • Sufficient time should be provided for tracing operations and rectification of errors • Provide the cardholder with written record of transactions • Loss up to the time of notifying the loss should be born by the cardholder up to a specified limit. • 24 hour loss notification facility to be provided • Immediate deactivation of card on receipt of notification of loss

Smart Cards • RBI Guidelines • Terms and Conditions for issue • Contractual terms for issuing cards should be given to the customer in writing • The terms and conditions should be expressed clearly • Basis of charges should be specified • Time taken for debit should be specified • Changes to be made only after giving sufficient notice to the cardholder

Smart Cards • RBI Guidelines • Terms and Conditions for issue • Should stipulate the customers liability to preserve the card and the PIN code • Recording of PIN code in form is prohibited • Obligation to notify the bank in the event of • Loss, theft or copying of the card • Recording of any unauthorised transaction in the account • Any irregularity in maintaining the account by the bank • Specify the contact point to which the information should be passed • Cardholder should not countermand the order given through the card

Smart Cards • RBI Guidelines • Terms and Conditions for issue • Extreme care should be taken in handling the PIN code and cardholder’s PIN code should be disclosed to him only • All losses to the cardholder due to a malfunction of the system are to the bank except technical failures which could be noted by the cardholder • The responsibility ofthe bank for the non-execution or defective execution of the transaction is limited tothe principal sum and the loss of interest subject to the provisions of the lawgoverning the terms

Barter Cards • Cards issued for exchange of commodities • Barter Card International (BCI) is providing the Barter Card service • BCI was established in Australia in 1991 and in UK in 1996 • Medium of exchange is Trading Pound • Barter card acts as a clearing house • Barter card is operated through franchisees who get a commission • Barter card system is not common in India