Download

1 / 30

300 likes | 461 Views

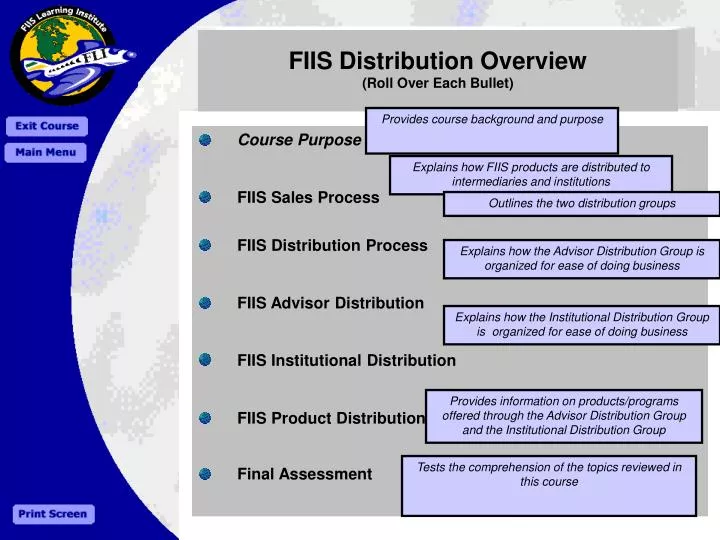

FIIS Distribution Overview (Roll Over Each Bullet). Provides course background and purpose. Course Purpose FIIS Sales Process FIIS Distribution Process FIIS Advisor Distribution FIIS Institutional Distribution FIIS Product Distribution Final Assessment.

E N D

FIIS Distribution Overview (Roll Over Each Bullet) Provides course background and purpose • Course Purpose • FIIS Sales Process • FIIS Distribution Process • FIIS Advisor Distribution • FIIS Institutional Distribution • FIIS Product Distribution • Final Assessment Explains how FIIS products are distributed to intermediaries and institutions Outlines the two distribution groups Explains how the Advisor Distribution Group is organized for ease of doing business Explains how the Institutional Distribution Group is organized for ease of doing business Provides information on products/programs offered through the Advisor Distribution Group and the Institutional Distribution Group Tests the comprehension of the topics reviewed in this course

Course Purpose Welcome to FIIS Distribution Overview! Background: Founded in 1979, Fidelity Investments Institutional Services Company, Inc., (FIIS) distributes Fidelity products, programs, and services through a variety of financial institutions, including banks, insurance companies, broker/dealers, financial planners, and pension fund administrators. Purpose: This course will provide you with an understanding of the FIIS distribution groups and how the process works. You will also learn about the different financials intermediaries that distribute FIIS products and programs to investors.

FIIS Sales Process Year-End 2002: Tax Fundamentals FIIS' distribution effort is comprised of Advisor Distribution Group and Institutional Distribution Group. Each distribution group has a sales force. The Sales Process: (click on each picture to learn about the process) FIIS Sales Force Comprised of wholesalers (Field sales and Inside sales) who work as a team to market FIIS products and services and provide sales support to investment professionals and intermediary firms. Intermediary Firms Represent varied financial institutions that, with a valid selling agreement, may sell the FIIS family of products to investors. Investors Includes individuals and institutions that work with an Investment Professional (IP) and pay a commission in exchange for investment advice.

Field Sales versus Inside Sales Field Sales are also referred to as outside wholesalers. Wholesalers are responsible for product and program sales in specific territories. Inside Sales partners with field sales teams by providing telephone sales support to clients and prospects. There are characteristics which differentiate Field Sales and Inside Sales. Drag each characteristic to the applicable column. Increase sales levels of producing investment professionals Live in their territory Work on sales desk in Smithfield Educate prospects and sellers about FIIS' product line and new offerings via the telephone Face-to-face client contact averaging 5.5 client meetings daily Partner with Inside Sales to distribute Fidelity products and programs to the intermediary marketplace Field Sales Inside Sales

Territory Map • The Territory Map depicts how various geographical areas are divided amongst FIIS’ sales force. • Click here to link to additional territory maps: • http://fnw.fmr.com/fiisnet/distribution/sales_resources/territory_maps/index.html

FIIS Distribution Groups • FIIS has two sales distribution groups committed to acquiring, developing and retaining high quality clients. Each distribution group has different strategies and support designed to address the needs of a particular type of client. • Advisor DistributionGroup (ADG) provides sales and relationship management support to Advisor Broker/Dealer clients and prospects. Fidelity Advisor products, programs, and services are distributed through FIIS' sales force to investment professionals. • Institutional DistributionGroup (IDG) is responsible for the development and management of relationships with senior management, home office contacts, and various decision-makers at intermediary firms that sell FIIS products to their clients.

FIIS Distribution Process Slide in Yellow Boxes (add lead in sentence) Advisor Distribution Group Institutional Distribution Group Fidelity Product Fidelity Product FIIS Sales Force FIIS Sales Force Investment Professional Client Firms Sales Force Investor (i.e. Individuals & Institutions) Investment Professional Investor (i.e. Capital Markets & Corporations)

FIIS Distribution Overview • FIIS categorizes like clients into distribution groups for ease in doing business particularly for trading, marketing, and communication purposes. • Distribution groups are formed according to the following criteria: • -The infrastructure at the intermediary • The service it provides to its own clients • The potential types of business the intermediary can bring to Fidelity • Distribution Group Distinctions:Each financial intermediary runs differently. Use of technology, the sales culture, and a variety of other factors distinguish one distribution group from another. Differences in distribution groups and the clients within demand that FIIS manage the relationships between varied intermediaries in a customized fashion.

FIIS Distribution Groups • FIIS Sales is committed to acquiring, developing, and retaining high quality clients. The table below lists the types of intermediaries within each distribution group.

Check Point 1. FIIS categorizes like intermediaries into ___________ for ease of doing business.A. MarketsB. BranchesC. Distribution GroupsD. Channels 2. Distribution Groups are formed according to the following criteria (select all that apply): A. Infrastructure at the intermediary B. Service it provides to its own clients C. Potential types of business the intermediary can bring to Fidelity D. Product Sales in a specific territory

FIIS Advisor Distribution Fidelity Advisor products may be sold by intermediaries with valid agreements on file at Fidelity. Fidelity Advisorproducts and programsare distributed through the intermediaries sales force of investment professionals. The investment professionals sell to the individual investor. The Advisor Distribution Group sells to the following:

Wirehouse and Regional Wirehouse: A wirehouse is a national or international intermediary whose branch offices are linked by a communications system that allows rapid dissemination of prices, information, and research related to financial markets and individual securities. Today, the term “wirehouse” refers to the biggest brokerage houses (e.g. Merrill Lynch and Prudential Securities). Regional: Although smaller regional intermediaries currently have access to similar data as a wirehouse, regional firms are considered to be the next 50 largest full service intermediaries. Some full service intermediaries are national in scope (e.g. First Union Securities and RBC Dain Rauscher). Full service means that FIIS offers a high level of automation to support these firms.

Wirehouse and Regional Comparison Wirehouses can be distinguished from regional intermediaires through several major categories. (hot words = Clearing, Proprietary, NSCC, Omnibus)(Change broker to IP?) Proprietary fund business means that a brokerage firm manages and distributes its own family of funds. The Advisor Funds are in direct competition with these proprietary funds.

Fidelity Intermediaries and Planners (FIP) FIP Bank Broker/Dealer (Roll Over) In an effort to expand their revenue generating businesses, banks are cross-selling and changing the way they sell and deliver their products (e.g. Fleet and Well Fargo). Banks are working towards offering “one stop shopping” for clients by offering products and services beyond the traditional bank products to include things like: Mutual funds Individual securities like stocks and bonds Retirement plans FIP Independent (Roll Over) The Independent market includes firms that provide securities transaction services to independent investment professionals, as known as financial advisors (e.g. Royal Alliance and American Express). Independent investment professionals are contractors of the intermediary firm, not employees to the firm. FIP Insurance Agency (Roll Over) The Insurance Agency market uses investment professionals of insurance companies to distribute Advisor products and services to customers (e.g. Met Life and Allmerica). A registered investment professional at an insurance agency may sell mutual funds, insurance products, retirement products and securities to clients.

Fidelity Intermediaries and Planners (FIP) Clearing firms offer the ability to execute, settle, andmaintain custody for mutual funds and provide the facilities to process dividend reinvestment, exchanges, and systematic withdrawals.

Check Point The Advisor Distribution Group consists of (select all that apply): A. Cash Business Unit B. Financial Intermediaries and Planners (FIP) C. Bank Business Unit D. Wirehouse and Regional The Financial Intermediaries and Planners consists (select all that apply): A. Insurance Agency B. Bank Broker/Dealer C. Cash Business Unit D. Independent

FIIS Institutional Distribution The Institutional Distribution Group focuses on sales and relationship management for institutional clients.

Insurance Wholesale The Insurance wholesale group coordinates relationship management and sales with insurance companies. Change Background & Font Colors

Bank Business Unit The Bank Business Unit, formerly known as Bank Trust, is responsible for the product strategy, marketing, and relationship management of Fidelity Advisor Fund sales through bank trust departments (e.g. PNC and Brown Brothers). In addition, the Bank Business Unit supports sales of 401(k) and Advisor 529 plans.

Cash Business Unit The Cash Business Unit, formerly known as Cash and Liquidity Management Services (CALMS), distributes money market funds to cash management professionals. The Cash Business Unit distributes directly through cash managers at corporations and through intermediaries that sell funds to cash management professionals. Fidelity Institutional Money Market (FIMM) Funds are utilized by a variety of institutional clients including banks, insurance companies, and broker/dealers. The Cash Business Unit is organized as follows: Roll Over - Client corporations purchase FIMM Funds directly without an intermediary (e.g. AT&T and Hewlett Packard) • Roll Over - ICS group distributes all share classes of the Fidelity Institutional Money Market (FIMM) Funds and all share classes of the Fidelity Cash Management Funds to the following organizations: • Bank Capital Markets(e.g. Fleet Capital Markets and Wachovia Capital Markets) • Trust (Custody, Personal Trust, Institutional Trust, Cash Management, Corporate Trust, Asset Management, Investment Management) (e.g. State Street Bank and Bank of New York) • B/D ( e.g. ABN AMRO ) and Insurance (e.g. GE)

Check Point Change Background & Font Colors • DRAG & DROP

Product/Program Distribution Grid • This grid provides information on the Products/Programs offered to intermediaries through Advisor Distribution and Institutional Distribution.(Make all Name Changes)

Retirement Product Distribution Change Background & Font Colors

Course Summary The goal of this training program has been to provide you with an understanding of how the distribution process works and the different financial service organizations that distribute FIIS products to investors. Add links to Departments (FIIS NET)

Change Background & Font Colors Distribution Group Differences • Distinguishing factors, between FIIS’ Distribution Groups, are outlined below. Click on each factor to learn about the key questions raised by the sales force and why. Click on left column-have coinciding descriptions pop up.

Segmentation • FIRM • A key component of FIIS’ business plan is a segmentation strategy that has been developed on the intermediary firm level. This strategy is applied to determine who the most profitable clients are and how FIIS can service them effectively. • Segmentation objectives include the following: • Focus on fewer intermediaries • Differentiate offerings based on client need and value • Maximize growth opportunities • Retain clients with large assets • INVESTMENT PROFESSIONAL

Check Point The firm segmentation strategy is used to determine the (select all that apply): A. Sales territories B. Most profitable intermediaries and how to service them C. Compensation structure D. Level of automation of each intermediary Factors that distinguish one group from another include (select all that apply): A. Organizational size B. Proprietary product line C. Sales strategy D. Ability to accept compensation

Check Point The Institutional Distribution Group consists of (select all that apply): A. Cash Business Unit B. Wirehouse and Regional C. Bank Business Unit D. Insurance