Download

1 / 1

10 likes | 132 Views

Corporate Governance Regulatory Framework in Brazil. IBGC Principles: Transparency, Fairness, Accountability and Corporate Responsibility

E N D

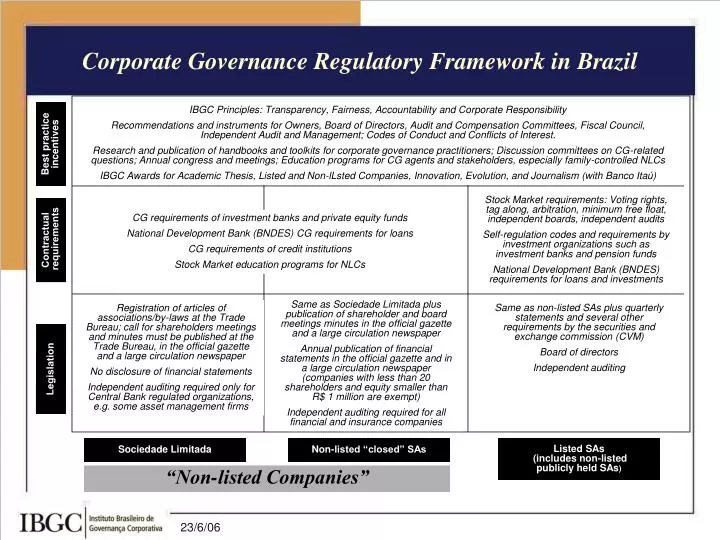

Corporate Governance Regulatory Framework in Brazil IBGC Principles: Transparency, Fairness, Accountability and Corporate Responsibility Recommendations and instruments for Owners, Board of Directors, Audit and Compensation Committees, Fiscal Council, Independent Audit and Management; Codes of Conduct and Conflicts of Interest. Research and publication of handbooks and toolkits for corporate governance practitioners; Discussion committees on CG-related questions; Annual congress and meetings; Education programs for CG agents and stakeholders, especially family-controlled NLCs IBGC Awards for Academic Thesis, Listed and Non-lLsted Companies, Innovation, Evolution, and Journalism (with Banco Itaú) Best practice incentives Stock Market requirements: Voting rights, tag along, arbitration, minimum free float, independent boards, independent audits Self-regulation codes and requirements by investment organizations such as investment banks and pension funds National Development Bank (BNDES) requirements for loans and investments CG requirements of investment banks and private equity funds National Development Bank (BNDES) CG requirements for loans CG requirements of credit institutions Stock Market education programs for NLCs Contractual requirements Same as Sociedade Limitada plus publication of shareholder and board meetings minutes in the official gazette and a large circulation newspaper Annual publication of financial statements in the official gazette and in a large circulation newspaper (companies with less than 20 shareholders and equity smaller than R$ 1 million are exempt) Independent auditing required for all financial and insurance companies Registration of articles of associations/by-laws at the Trade Bureau; call for shareholders meetings and minutes must be published at the Trade Bureau, in the official gazette and a large circulation newspaper No disclosure of financial statements Independent auditing required only for Central Bank regulated organizations, e.g. some asset management firms Same as non-listed SAs plus quarterly statements and several other requirements by the securities and exchange commission (CVM) Board of directors Independent auditing Legislation Sociedade Limitada Non-listed “closed” SAs Listed SAs (includes non-listed publicly held SAs) “Non-listed Companies”