Download

1 / 53

530 likes | 685 Views

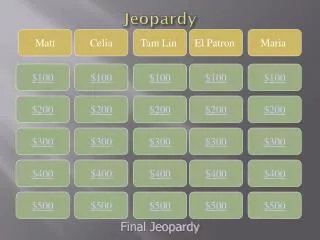

Types of Risk. Property & Liability Insurance. Health and Life Insurance. Risk Management. Insurance Terminology. 100. 100. 100. 100. 100. 200. 200. 200. 200. 200. 300. 300. 300. 300. 300. 400. 400. 400. 400. 400. 500. 500. 500. 500. 500.

E N D

Types of Risk Property & Liability Insurance Health and Life Insurance Risk Management Insurance Terminology 100 100 100 100 100 200 200 200 200 200 300 300 300 300 300 400 400 400 400 400 500 500 500 500 500

What is Pure risk?

Pure risk faced by a large number of people and the amount of loss can be predicted.

What is insurable risk?

Chance that loss may occur when your actions result in injuries to others or damages to someone else’s property

An organized strategy for controlling financial loss from pure and insurable risks.

What is risk management?

Lowering the chance for loss by not engaging in activities that could result in loss.

Taking precautions to reduce the chance of loss or severity of loss

Accepting the consequences of risk and the financial burden.

A specified amount, that you are responsible for, subtracted from covered losses.

Sums of money to be paid for specific types of losses under the terms of the policy.

A policyholder’s request for reimbursement for a loss under the terms of the insurance policy.

Protection from loss regarding your personal property and liability risks when you rent an apartment or a home.

Protects the insured, in the event of a car accident, against claims for bodily injury to another person and damage to another person’s property.

Protects your own car against damages from accidents or vehicle overturning.

Drivers receive reimbursement for their expenses from their own insurer no matter who is responsible for the accident.

A personal catastrophe policy which supplements your basic auto and property liability coverage.

The person named in a life insurance policy to receive benefits.

Health insurance coverage that pays for your hospital room and board and prescription drugs during your hospital stay.

The most common form of life insurance that only lasts for a specified period of time.

When a family has more than one insurance plan the insurers will share the costs of the claim, not to exceed 100% of allowable expenses.