Download

1 / 10

110 likes | 135 Views

Explore the fundamental economic concepts of supply, demand, and price. Learn how consumer preferences, market conditions, and production costs influence pricing. Discover the laws and factors affecting demand and supply to grasp the dynamics of pricing in various scenarios.

E N D

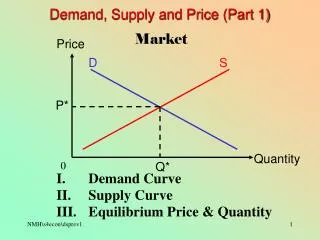

One of the most basic concepts of economics is Supply and Demand. They are really two separate things, but they are almost always talked about together

DEMAND Demand is the quantity of a good or service that consumers are willing and able to buy at a particular price. Since each of us has different needs and wants, we each have different demands. When we buy a particular good or use a particular service, we are expressing demand for it.

Price Demand Law of Demand • Consumers buy more as price decreases. • As price increases consumers buy less.

Four conditions that create demand: 1. Consumers must be aware of and interested in the product. - advertising 2. Enough supply of product 3. Prices are reasonable and competitive 4. Product must be accessible to consumers.

Four factors that affect demand (increase or decrease) 1. Changing consumer income – income increases , people buy more 2. Changing consumer tastes – fashion changing 3. Changing expectations for the future – if price to increase – buy more (HST intro) 4. Changes in population – number of people, ages

SUPPLY • Supply is the quantity of a good or service that businesses are willing and able to provide within a range of prices that people would be willing to pay.

Price Supply Law of Supply: • As prices increase, the quantity supplies will increase.

Five conditions that affect Supply: 1. Change in the number of producers. 2. Changes in price. – Roses after Valentines Day 3. Changes in technology. – Able to produce items more efficiently 4. Changing expectations for the future 5. Changing production costs. – price of oil

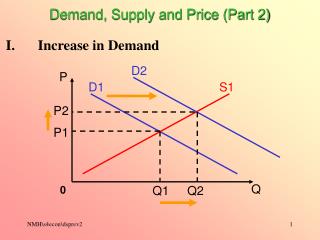

PRICE Price is determined by both supply and demand and the cost of producing a good or service. 1. If the demand for a product increases and the supply is low the price will increase. Example: Concert, sporting events • If the demand for a product decreases and the supply is high the price will decrease. Example: Christmas wrapping paper on Boxing Day