Download

1 / 27

270 likes | 505 Views

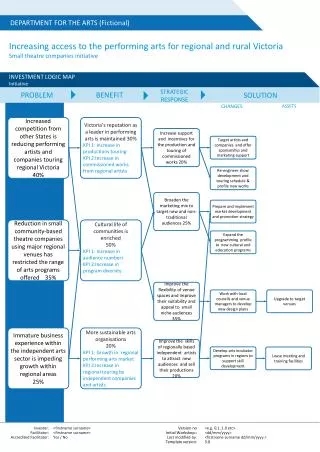

Benefit Payment Control. Modified Wage-Benefit Cross match Presented by John McLandrich, Director, Benefit Payment Control (512) 936-3061. April 21, 2010. Overview. Previous Workflow Process Identify Deliverables Develop Framework Project Implementation Goals Post Implementation

E N D

Benefit Payment Control Modified Wage-Benefit Cross match Presented by John McLandrich, Director, Benefit Payment Control (512) 936-3061 April 21, 2010

Overview • Previous Workflow Process • Identify Deliverables • Develop Framework • Project Implementation • Goals • Post Implementation • Lessons Learned • Current Initiatives

Previous Workflow Process • Wage/benefit cross-match ran six months after quarterly wages posted • Laborious • Antiquated • Untimely • Event took four days

Previous Workflow Process Day 1 – Request made to identify wage/benefit cross match hits Day 2 – Report received showing hits for 1 to 13 benefit weeks – supervisor selects sample population, normally 30,000 to 40,000 per quarter Day 3 – Receive sample of 5 casesand check • If 5 samples good, supervisor runs the job • Supervisor also runs special job to detect agency employees Day 4 – Run job to generate audit form mailings

Previous Workflow Process • 40%-60% of investigator’s time spent performing clerical duties • Opening mail • Physically sorting earnings audits • Preparing fraud letter • Preparing certified mailings (manual process) • Keying earnings • Preparing file folder for paper documents • Contacting employer to reconcile payroll records to benefit weeks • Average wage/benefit cross-match hit overpayment $2200-$2300 range

Identify Deliverables • May 17, 2005 USDOL issued “Region IV Workforce Investment Memorandum No. 16-05” notifying states about FY 2005 funding opportunities • Applied for and received funding specifically to improve UI performance: • $100,000 – Case Management for Investigations • $500,000 – Predictive Analysis • $500,000 – OCR Scanning, Imaging and Internet Receipt Audit Response • $500,000 – Modified Wage Benefit Cross match

Identify Deliverables (cont.) Case Management for Investigations - $100,000 • Enhance procedures to manage New Hire and Wage Benefit cross match investigations by automating case management and improving overpayment investigation tracking • Major Work Activities • Maintains documents and management information • Helps create paperless cases • Distributes case loads evenly • Organizes staff assignments • Maintains case files electronically • Provides employer information online

Identify Deliverables (cont.) Predictive Analysis - $500,000 • Incorporate predictive analysis and case weighting strategies to improve Benefit Payment Control (BPC) activities

Identify Deliverables (cont.) OCR Scanning & Internet Receipt Audit Response – $500,000 • Provide employers with an electronic means to respond • Optical Character Recognition • Internet • Machine-to-Machine Interface • Automatically populate and save earnings data

Identify Deliverables (cont.) Modified Wage Benefits Cross match – $500,000 • Modify to detect issues as soon as possible • Prioritize workload based on claims status to prevent additional overpayments • Automatically send call-in to claimant • Automatically send Wage Audit Form (Earnings) to employer

Develop Framework • Once approved, we developed a project framework • Fortunately the Texas Department of Information Resources provided the framework and all templates to execute a technology project • See handout: Texas Project Delivery Framework

Develop Framework (cont.) • Gather team • Develop functional diagrams • Always consider dependencies and constraints • Develop requirements in detail • Create weighting concept and details • Redesign form

2006 • In late 2006, the agency implemented the National Directory of New Hire (NDNH) cross match • UI director decided to investigate all new hire cases to “stop the bleeding” • At that time, BPC Investigations and Tele-Centers shared the new hire investigations workload • BPC Investigations focus changed from wage/benefit cross match to new hire – keep in mind wage/benefit cross match hits were handled only by BPC Investigations • Incorporating this change greatly impacted the wage/benefit cross match process design

2008 – Project Implementation • April – new wage/benefit cross match process implemented • August – project officially completed

Goals • Increase productivity and efficiency • Detect earnings issues ASAP • Address earnings issues ASAP • Decrease average wage/benefit overpayment amount • Provide claimants, employers and agency an easier and more comprehensive means of handling earnings information • Provide a system that enables users to adjust workload • Improve overall performance

Post Implementation • Average wage/benefit cross match has dropped to as low as $607 for 3rd quarter 2009 with a $717 average since implementation • The highest was $3164 in 3rd quarter 2001 • The lowest quarter prior to project implementation was $832 for 3rd quarter 2007; due to pulling the BPC staff off investigations to take disaster claims for hurricanes Rita and Katrina

Post Implementation (cont.) • Average wage/benefit investigations in 53 quarters preceding project implementation was 1,077 per quarter • Average wage/benefit investigations after project implementation is 4,140 per quarter • Of 4,140 average per quarter, 3,994 per quarter were done without human intervention – 96.47%

Post Implementation (cont.) • Investigators now spend their time working on investigations and handling the increased call volume • As GPRA declines, this tool allows the agency to adjust and redirect attention to larger earnings investigations

Lessons Learned • Establish a functional working relationship with IT staff and contractors • Contractor staff changes can be good and bad – in our situation contractor turnover was to our advantage • Different set of eyes, ears and ideas • Some contractors are there only to perform their specific function • For continuity, contract management needs to be there for the duration • Maintain momentum • There will be roadblocks, expect them and work through them • Keep everyone focused

Lessons Learned (cont.) • Revisit and rethink processes and procedures • Quite a few procedures that could be changed or eliminated • Eliminated requirement to send fraud correspondence via certified mail • Form used to verify earnings information was reworked and simplified • Interpreting employer payroll records was nearly eliminated (automation enables employers to provide the information in the format the agency needs) • Non fraud overpayments are being established without human intervention

Lessons Learned (cont.) • Even after testing, problems and issues will come up • This is normal and should be expected • Other benefit programs outside BPC may try to blame project programming for system problems • Keep focused on the future and encourage others to support the purpose of the automation

Current Initiatives • New Hire case weighting • Begins May 2010 • One year automation project • $652,300 funded by USDOL grant • Replace Earnings Verification Form (EVF) with letter directing employers to use web • Machine-to-machine interface of earnings information • Requirements are complete, currently seeking participation • Working with TALX and Wal-Mart

Summary • Previous Workflow Process • Identify Deliverables • Develop Framework • Project Implementation • Goals • Post Implementation • Lessons Learned • Current Initiatives