Download

1 / 8

80 likes | 328 Views

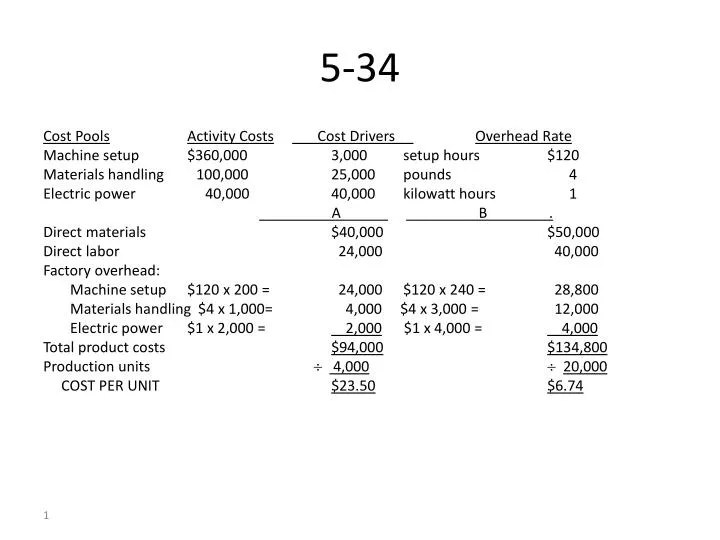

5-34. Cost Pools Activity Costs Cost Drivers Overhead Rate Machine setup $360,000 3,000 setup hours $120 Materials handling 100,000 25,000 pounds 4 Electric power 40,000 40,000 kilowatt hours 1

E N D

5-34 Cost PoolsActivity Costs Cost Drivers Overhead Rate Machine setup $360,000 3,000 setup hours $120 Materials handling 100,000 25,000 pounds 4 Electric power 40,000 40,000 kilowatt hours 1 A B . Direct materials $40,000 $50,000 Direct labor 24,000 40,000 Factory overhead: Machine setup $120 x 200 = 24,000 $120 x 240 = 28,800 Materials handling $4 x 1,000= 4,000 $4 x 3,000 = 12,000 Electric power $1 x 2,000 = 2,000 $1 x 4,000 = 4,000 Total product costs $94,000$134,800 Production units 4,00020,000 COST PER UNIT $23.50$6.74

6-38 Estimated cost of electricity equals $210 (from information about August and December) ($870 - $210)/(20 - 60) = - $16.50 /degree At 60 degrees F: $210 = intercept + (-$16.50 x 60) $210 = intercept - $990 intercept = $1,200 Cost equation: Utilities cost = $1,200 - $16.50 x degrees above zero A reliable cost estimate for January is not available since the average temperature of 10 degrees is outside the relevant range of the data used to develop the high-low estimate. Would be calculated $1,200 - $16.50 x 10 = $1,035 The cost estimate for February is: $1,200 - $16.50 x 40 = $540

7-36 1. BE units = F + N = $150,000 = 15,000 hats p - v $30 - $20 BE $ = Fixed costs = Fixed costs = $150,000 = $450,000 CMR p - v $30-$20 p $30 2. 20,000= $150,000 + N $30 - $20 $200,000= $150,000 + N operating profit = $50,000 3. Margin of safety = 25,000 – 15,000 = 10,000 hats Margin of safety ratio = 10,000/25,000 = 40% 4. BE units = F = $150,000 + $82,000 = 16,000 p - v $30 - $15.50 20,000 = $232,000 + N $30 - $15.50 N = operating profit = $58,000 5. A key strategic issue is that Frank’s sales staff is a critical success factor for the business. His knowledgeable and courteous staff help to bring in and retain customers. If the salary/commissions plan would alienate his sales staff, the plan could be a big mistake. Frank should proceed with caution, and be sure that his sales staff will be as highly motivated under the salary plan as they were under the commissions plan.

7-30 1. Sales = variable cost + fixed cost + target operating profit 30,000($65) = 30,000($34) + $465,000 + N N = $465,000 2. BE units: $65Q = $34Q + $465,000 Q = 15,000 units 3. Operating profit: 35,000($65)-35,000($34)-$465,000-$200,000= N N = $420,000 (operating profit falls by $45,000, from $465,000 to $420,000 as a result of the plan to increase sales with increased advertising) 4. BE units: $65Q = $34Q + $665,000 Q = 21,452 units (operating profit is lower, per part 3 above, and breakeven is also higher) 5. $65Q = $34Q + $665,000 + $465,000 Q = 36,452 units (to justify the advertising plan, sales would have to rise to at least 36,452 units, somewhat above the projected 35,000 units)

Class problem Ardel Co. budgeted to sell 200,000 units of Zbox in September. Production of one unit of Zbox required two pounds of aluminum and five pounds of steel. The beginning inventory and the desired ending inventory in units are: • How many units of Zbox are to be manufactured during September? 189,000. (200,000 + 13,000 – 24,000) • How many pounds of aluminum does Ardel Co. need to purchase during September if Ardel plans to manufacture 150,000 units of Zbox in September? 293,000 pounds ((150,000 x 2) + 23,000 – 30,000) • How many pounds of steel powder does Ardel Co. need to purchase during September if Ardel plans to manufacture 150,000 units of Zbox in September? 755,000 pounds.((150,000 x 2) + 31,000 - 26,000)

P 8-35 1. Budgeted Cash Receipts: November: ($100,000 x 0.95) x 0.35 x 0.80 x 0.98 = $26,068 ($100,000 x 0.95) x 0.35 x 0.20 = $ 6,650 ($150,000 x 0.95) x 0.65 x 0.80 x 0.98 = $72,618 ($150,000 x 0.95) x 0.65 x 0.20 = $18,525 $123,861 December: ($150,000 x 0.95) x 0.35 x 0.80 x 0.98 = $39,102 ($150,000 x 0.95) x 0.35 x 0.20 = $ 9,975 ($ 90,000 x 0.95) x 0.65 x 0.80 x 0.98 = $43,571 ($ 90,000 x 0.95) x 0.65 x 0.20 = $11,115 $103,763

P 8-35 2. Budgeted Cash Disbursements: November: ($170,000 x 0.75) x 0.25 = $31,875 ($270,000 x 0.75) x 0.75 = $151,875$183,750 December: ($200,000 x 0.75) x 0.25 = $37,500 ($170,000 x 0.75) x 0.75 = $95,625$133,125

8-40 Cash Available Cash balance, beginning $ 10,000 Cash collections from customers + 150,000 Total cash available $ 160,000 Cash Disbursements Direct materials purchases $ 25,000 Operating expenses $50,000 Less: Depreciation expenses - 20,00030,000 Payroll 75,000 Income taxes 6,000 Machinery purchase + 30,000 Total cash disbursements prior to financing $ 166,000 Financing: Cash excess (shortage) before financing ($ 6,000) Minimum cash balance desired - 20,000 Financing need $ 26,000