Download

1 / 130

1.31k likes | 1.62k Views

The PC Manufacturer Industry. Business 417 Presentation: Ali Pourdad Claire Yan Jessica VandenAkker Benny Cheong. Agenda. Industry Analysis Industry Overview Industry Profile Industry Trends Company Analysis Gateway, Inc. HP/Compaq Inc. Dell, Inc. Industry Overview.

E N D

The PC Manufacturer Industry Business 417 Presentation: Ali Pourdad Claire Yan Jessica VandenAkker Benny Cheong

Agenda • Industry Analysis • Industry Overview • Industry Profile • Industry Trends • Company Analysis • Gateway, Inc. • HP/Compaq Inc. • Dell, Inc.

How the Industry Operates • 1980s • Today: 20% - Servers 78% PCs 2% Workstations

Computer Form Factors • Every type of Computer comes in a variety of “form factors,” or physical designs apart from the computer’s main electronics that play a large role in determining the computer’s potential uses and markets. • The Most common form factor distinction in the PC market is between the desktop and notebook.

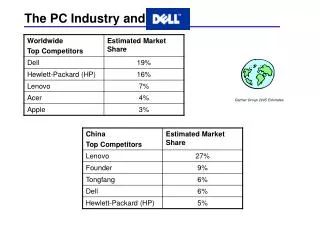

Worldwide PC Shipments Market Share(In percent, based on units shipped) Fujitsu – 4.2% Toshiba – 3.3% Fujitsu – 4.2% Toshiba – 3.2% IBM – 5.9% IBM – 5.9% Dell – 15.1% Dell – 16.9% Others - 55.6% Others – 53.3% HP/Compaq 16.0% HP/Compaq 16.4% Total Units: 136.9 Million Total Units: 152.6 Million

Worldwide PC Shipment Growth(In percent, based on units shipped)

US PC Industry • Computer hardware mature in the latter half of the 90s?

Business Models • Contract Manufacturing vs. J.I.T. delivery • Everyone vs. Dell • Retail Store Model - MAC • White Box Competition

White Box Competitors • Highly fragmented • Selling unbranded “white box” computers • Accounts for over 50% of global market share in 2002, 2003, and 2004 to-date. • In the United States: • Small and medium size businesses are primary purchasers of white box. • White box computers had the largest share of the small business market in the US, with almost 40% in 2002.

IT Trends • White box have benefited from a niche market growing in the area of high performance PCs that are optimized for video game applications. • The price gap between top-tier vendors’ machines and those manufactured by second/third tier vendors has narrowed. • Third and fourth quarters are always the biggest in the PC manufacturer industry – Back-to-school and Holidays • Standard & Poor’s believes that industry revenues may be up 3% to 4% in 2004, given the competitive pricing environment and the gradual upturn in IT investment expected.

Dow Jones Computer Index 5 Years

Dow Jones Computer Index • 142 securities in this index • Some of the big names include: • Apple Computer, Inc. (AAPL) • HP/Compaq (HPQ) • Dell, Inc. (DELL) • Gateway, Inc. (GTW) • Others: Quantum Corp., Seagate Technology,, Logitech, Lexmark, Synaptics Inc

Dow Jones Computer Index Last 3 Months – Beside NYSE Index

Dow Jones Industry Index INDUSTRY INDEX STATISTICS • Price:391.76 • Price Change:5.91 • % Price Change:1.53% • Market Cap:262.6 Billion • Dividend Yield: n/a • P/E Ratio:53.14 • 52-Week Range:324.06 to 410.35 • 1-Yr % Change:1.32%

NASDAQ Computer Index • 645 securities are on the Nasdaq Computer Index (IXCO) • Some of the big names: • Dell, Inc. (DELL) • Microsoft, Corporation (MSFT) • Intel Corporation (INTC) • Google, Inc. (GOOG) • Apple Computers (AAPL)

Preliminary worldwide PC vendor unit shipments estimates for Q2 2004 In the United States, PC shipments totaled 14 million units in the second quarter of 2004, an 11.4% increase from the second quarter of 2003.

Key Industry Ratios and Statistics • Index of leading economic indicators • Business Capital Spending • Consumer Confidence • Base year was 1985 (1985=100) • High Levels - Computer Sales Improve • Low Levels – Computer Sales Decline • Real growth in GDP

Company Overview • Founded in 1985 • Started by a $10,000 loan • Previously called Gateway 2000 • In 1993, it went public, traded on NASDAQ • In 1997, added to NYSE • In March 2004, acquired eMachines ($235 million) • As of July 2004, approximately 3400 employees

Value Proposition --- Offering products directly to customers, providing them with the best value for their money and unparalleled service and support

Executives & Management Wayne Inouye (Mar. 2004) President & CEO Adam Andersen(Mar. 2004) Senior Vice President, Chief Administrative OfficerScott Weinbrandt (Jan. 2003) Senior Vice President, DirectBob Davidson(Mar. 2004)Senior Vice President, U.S. Retail Greg Memo(Mar. 2004)Senior Vice President, Platform Development & Operations Rod Sherwood (Sep. 2002) Senior Vice President, Chief Financial Officer

Products • PCs: desktops, notebooks, all-in-ones, professional PC systems (networking, servers and storage) • Consumer Electronics: digital TVs, digital camera, MP3 players, DVD players etc. • Other: accessories and services

Distribution Channels • Direct Distribution: web, phone, 189 retail stores • Third party sales through partners such as: Costco, Home Shopping Network, etc. • Limited reseller relationships in Canada & Mexico

Major Competitors • IBM • Cisco Systems • HP/Compaq • Dell Inc.

News Highlights • eMachines acquisition in March, 2004 • Buy back shares from AOL

New Strategy • New Multi-Brand Segmentation Strategy • Segmented two-tier branding/positioning model • Traditional eMachines + GTW brand (e.g.Lexus & Toyota) • Expanding eMachines’ Distribution Internationally • Japan: nearly 200 stores • UK: 730 stores • Mexico: 475 stores • Follow-on expansion for Germany & France

Market Share • U.S. PC Market Share (by dollar amount) • 2001: 10% • 2002: 5.5% - 6% • Decreased 4% • 2003: 3.3 – 3.8% • Decreased 2% • With its acquisition of eMachines now complete, Gateway is the third-largest PC company in the U.S. and among the top ten worldwide.