Download

1 / 17

170 likes | 177 Views

This text discusses methods for dealing with options on dividend-paying stocks, including continuous and discrete dividend yields. It also covers the use of dollar dividends and provides an example. Additionally, the text comments on and extends the model to options on indices, currencies, and futures contracts. It includes information on time-dependent interest rates, time-dependent volatility, trinomial trees, and adaptive mesh models. Further reading suggestions are provided.

E N D

2. Lattice Methods 2.3 Dealing with Options on Dividend-paying Stocks (Hull, Sec. 17.3, page 401)

With Dollar Dividend • A better procedure: • Draw the tree for the stock price less the present value of the dividends • Create a new tree for the stock price by adding the present value of the dividends at each node • This ensures that the tree recombines and makes assumptions similar to those when the Black-Scholes model is used

Example 1: American put option on a stock: S0= 52; K = 50; D = $2.06r =10%; s* = 40%; T = 5 months; = 3.5 monthst = 1 month

Example 1: Tree model for S* +$2.05

2. Lattice Methods 2.4 Comments and Extensions of the model

Trees for Options on Indices, Currencies and Futures Contracts (Hull, Sec. 11.9, Sec. 17.2) • As with Black-Scholes: • For options on stock indices,replace the continuous dividend yield D0with the dividend yield on the index • For options on a foreign currency, D0equals the foreign risk-free rate rf • For options on futures contracts D0 = r

Time Dependent Interest Rate and Dividend Yield (page 409) • Making interest rate r or dividend yield D a function of time does not affect the geometry of the tree. The probabilities on the tree become functions of time • Discounting factor becomes a function of time as well

Time Dependent Volatility (page 409) • Changing s at each time step does affect the geometry of the tree. (The probabilities on the tree become functions of time) • Or we can make s a function of time by making the lengths of the time steps inversely proportional to the variance rate.

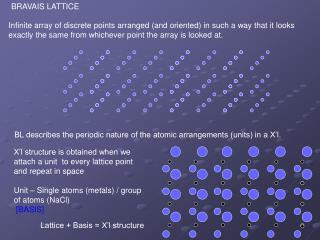

Su pu pm S S pd Sd Trinomial Tree (see Technical Note 9, www.rotman.utoronto.ca/~hull)

Adaptive Mesh Model • This is a way of grafting a high resolution tree on to a low resolution tree • We need high resolution in the region of the tree close to the strike price and option maturity • Numerically efficient over a binomial or trinomial tree • Figlewski and Gao, “The adaptive mesh model: a new approach to efficient option pricing”, J. of Financial Ecomonics, 53:313-351 (1999)

Further Reading • L. Clewlow and C. Strickland. Implementing Derivatives Models. Wiley, Chichester, West Sussex, England, 1998 (relationship between finite differences and trinomial trees) • D J Higham. Nine Ways to Implement the Binomial Method for Option Valuation in Matlab. SIAM review, 44:661-677, 2002 (issues of implementing binomial trees) • J C Hull. Option, Futures, and Other Derivatives. Prentice Hall. (classic reference) • G. Levy. Computational Finance. Numerical Methods for Pricing Financial Instruments. Elsevier Butterworth-Heinemann, oxford, 2004 (implied lattices and efficient implementations)