Download

1 / 22

220 likes | 231 Views

This panel discussion will provide practitioners with an overview of the new IRS voluntary disclosure practice, including its history and modifications. Attendees will gain insights into the various iterations of the program and understand the implications for taxpayers with potential criminal liability or substantial civil penalties. The discussion will also cover alternative options available for taxpayers with unfiled returns or unreported income. Don't miss this essential update on the IRS voluntary disclosure practice.

E N D

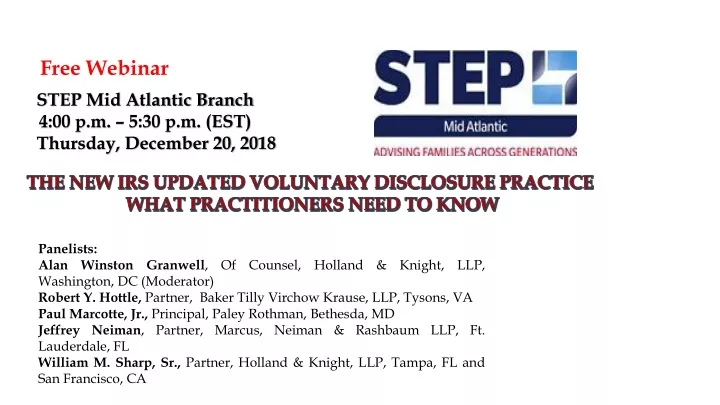

STEP Mid Atlantic Branch 4:00 p.m. – 5:30 p.m. (EST) Thursday, December 20, 2018 THE NEW IRS UPDATED VOLUNTARY DISCLOSURE PRACTICE WHAT PRACTITIONERS NEED TO KNOW Panelists: Alan Winston Granwell, Of Counsel, Holland & Knight, LLP, Washington, DC (Moderator) Robert Y. Hottle, Partner,Baker Tilly Virchow Krause, LLP, Tysons, VA Paul Marcotte, Jr., Principal, Paley Rothman, Bethesda, MD Jeffrey Neiman, Partner, Marcus, Neiman & Rashbaum LLP, Ft. Lauderdale, FL William M. Sharp, Sr., Partner, Holland & Knight, LLP, Tampa, FL and San Francisco, CA

Introduction – The History of “Official” Voluntary Disclosure Program • A brief history of the various “official” iterations of the offshore voluntary disclosure programs including: • January 14, 2003 Offshore Voluntary Compliance Initiative (“2003 OVCI”), expired on April 15, 2003. The 2003 OVCI resulted in only 1,300 disclosures. • March 23, 2009 Offshore Voluntary Disclosure Program (“2009 OVDP”), expired on October 15, 2009. The 2009 OVDP was generally a success and included 15,000 timely disclosures (and an additional 3,000 disclosures after the closing date). • February 8, 2011 Offshore Voluntary Disclosure Initiative (“2011 OVDI”), expired on September 9, 2011. The 2011 OVDI also was a success with 18,000 disclosures. • January 9, 2012 Offshore Voluntary Disclosure Program (“2012 OVDP”), which resulted in 12,000 disclosures and later modified and expanded on June 18, 2014 (the “2014 OVDP”). The 2014 OVDP expired on September 28, 2018. STEP Mid-Atlantic Branch

Introduction – The History of “Official” Voluntary Disclosure Program (continued) • The 2009 OVDP, 2011 OVDI, 2012 OVDP, and 2014 OVDP resulted in more than 56,000 disclosures and approximately $11.1 billion in back taxes, interest, and penalties. • August 29, 2013 the Department of Justice (“DOJ”) Program for Swiss Banks (various due dates depending on the category of the banks), in effect the first ever “official” voluntary disclosure program targeted to a given country and a specified industry – 80 Category 2 banks entered into non-prosecution agreements paying approximately $1.3 billion in penalties (“NPA”), five banks entered into Category 3 non-target letter resolutions (“NTL”), and zero banks qualified for Category 4. • With the expiration of 2014 OVDP on September 28, 2018, many practitioners immediately relied on the decades-old Internal Revenue Service (the “IRS”) “voluntary disclosure practice” as enunciated in Internal Revenue Manual (the “IRM”) 9.5.11.9 until November 20, 2018, the date of the newest Compliance News Flash. STEP Mid-Atlantic Branch

Background and Overview of Updated Voluntary Disclosure Practice • The Deputy Commissioner for Services Enforcement issued a memorandum entitled “Updated Voluntary Disclosure Practice” (the “Memorandum”) on November 20, 2018. • The new practice has a de facto retroactive effect since the Memorandum addresses a new process for all voluntary disclosures, both domestic and offshore, following the September 28, 2018 expiration of the 2014 Offshore Voluntary Disclosure Program. • Consistent with the above history, the Memorandum charts the history of the 2014 OVDP as a modified version of the 2012 iteration that followed the programs issued in 2011 and 2009. • The Memorandum notes the intent of the official voluntary disclosure programs was to address taxpayers with either: • Potential criminal liability, or • Substantial civil penalties due to a willful failure to report foreign financial assets and pay appropriate income tax thereon • The Memorandum comments that the earlier voluntary disclosure programs provided taxpayers with potential criminal exposure or substantial civil penalties with terms and conditions for resolving their civil tax and penalty obligations. STEP Mid-Atlantic Branch

Background and Overview of Updated Voluntary Disclosure Practice(continued) • The Memorandum also notes relief for taxpayers with unfiled returns or unreported income lacking either criminal liability or substantial civil penalties based on willful noncompliance to consider coming forward under the Streamlined Filing Compliance Procedures (“SFCP”), the Delinquent FBAR submission procedures or the Delinquent International Information Returns Submission Procedures. • The Memorandum cautions once again that such non-wilfull remedies are available but could be “discontinued at any time.” • In citing the Internal Revenue Manual’s (the “IRM”) long-standing voluntary disclosure practice at § 9.5.11.9, the Memorandum prescribes that the intent of the new process is to update that decades-old informal practice. • Under IRM § 9.5.11.9, practitioners had substantial flexibility in submitting remedial filings under the voluntary disclosure package, and generally speaking, the results were much more beneficial in comparison to the official voluntary disclosure programs or other alternatives. STEP Mid-Atlantic Branch

Background and Overview of Updated Voluntary Disclosure Practice (continued) • Although the IRM does not describe an exact submission forms procedural process or a prescription of the prior years on non-compliance to be covered or penalties and taxes to be proffered, by way of example, the IRM illustrates the submission of amended returns with a “lawyer’s letter” outlining the disclosure. • The IRM adds emphasis that the disclosure must be “timely” – generally meaning submitted before the IRS has initiated a civil examination or criminal investigation or has become aware of the noncompliance. The previous iterations of the voluntary disclosure programs generally mirrored the IRM’s “timely” requirement. STEP Mid-Atlantic Branch

Background and Overview of Updated Voluntary Disclosure Practice (continued) • Interestingly, the Memorandum also comments that the taxpayers who did not commit any tax or tax-related crimes and thus do not need the voluntary disclosure practice due to the absence of potential criminal prosecution can still come forward to rectify historical mistakes by utilizing one of the procedures mentioned above (e.g., SFCP) or alternatively by filing an amended return or past due tax return. • However, amended returns filed in this manner will be reviewed by IRS examiners following existing law and guidance governing audits of those issues but not necessarily imposing the tax and penalties prescribed by the Memorandum (although this is a debatable point – the key point being was the taxpayer’s conduct was non-willful, or alternatively, willful and, if the latter, to what degree?). STEP Mid-Atlantic Branch

Timing of the New Procedures • The new procedures will be effective for all voluntary disclosures – both domestic and offshore, submitted after the September 28, 2018 closing of the 2014 OVDP. • Submissions made on the eve of the September 28, 2018 deadline will be treated under the 2014 OVDP so long as such submissions include a postmark date no later than September 28, 2018. • Interestingly, for domestic voluntary disclosures (i.e., non-offshore) received by the IRS on or before September 28, 2018, the Memorandum prescribes that the IRS has the discretion to apply the procedures described in the Memorandum. STEP Mid-Atlantic Branch

Timing of the New Procedures (continued) • Contrary to the “take-it-or-leave-it” prescription set forth beginning with the 2009 OVDP and adopted in follow-on iterations thereof, the Memorandum delegates potential civil penalty mitigation by focusing on a specific disclosure timeframe along with the application of “examiner discretion” based on all relevant facts and circumstances. • The Memorandum stresses that examiner discretion is a function of a “prompt and full cooperation” during the civil examination of the voluntary disclosure. • The Memorandum assigns responsibility to IRS managers to ensure that penalties are “applied consistently, fully developed, and documented in all cases.” • Finally, the Memorandum stresses that the terms and conditions set forth in the Memorandum are only applicable to taxpayer submissions that are made on a timely basis and assuming the timeliness requirement is met. STEP Mid-Atlantic Branch

Criminal Investigation Procedures • The Memorandum sets forth that procedure by which taxpayers wishing to make a voluntary disclosure may submit a pre-clearance request. • Upon submission, IRS Criminal Investigation (“CI”) will screen all voluntary disclosure requests, whether domestic or offshore, to determine taxpayer eligibility. • Eligibility will hinge extensively if not solely on the timeliness requirement. • The Memorandum directs taxpayers seeking to participate in the voluntary disclosure process to submit a pre-clearance request on an upcoming revised version of Form 14457. • The rules for determining taxpayer eligibility will still be governed by IRM 9.5.11.9. • Assuming CI grants a pre-clearance status, taxpayers must “promptly” submit to CI all required voluntary disclosure documents based on the forthcoming revision of Form 14457. STEP Mid-Atlantic Branch

Criminal Investigation Procedures (continued) • Not surprisingly, Form 14457 will require information related to taxpayer noncompliance, a narrative providing the facts and circumstances, assets, entities, related parties and any professional advisors involved in the noncompliance. • Is there a potential Catch-22 with pre-clearance – what if taxpayer provides IRS with roadmap of compliance issues, but does not ultimately receive pre-clearance? • After receipt of the voluntary disclosure documents, CI will determine whether or not the taxpayer is preliminarily accepted into the voluntary disclosure process and notify the taxpayer of its decision. • Acceptance notification will be made by letter and simultaneously CI will forward the voluntary disclosure letter with all attachments to LB&I Austin unit for case preparation before examination. • The Memorandum notes that CI will not process tax returns or payments, rather this will be handled pursuant to the Civil Processing segment described below. STEP Mid-Atlantic Branch

Civil Processing • Upon receipt of the relevant information from CI, LB&I Austin, Texas will route the case as appropriate. • Austin in effect will become a “traffic director” unit and no additional documentation will be provided to the Austin unit. • However, in order to mitigate interest exposure, LB&I Austin will accept payment prior to case assignment for those taxpayers wishing to make a prompt payment. • LB&I Austin also will establish the most recent tax year covered by the voluntary disclosure for field examination. • As the traffic director, Austin will forward cases for “case building and field assignment” to the appropriate Business Operating Division and Exam reflection for civil examination. • The Memorandum directs civil examiners receiving the disclosure to establish any additional controls necessary on IRS systems. STEP Mid-Atlantic Branch

Case Development • All distributed voluntary disclosures from LB&I Austin handled by IRS exam will follow standard examination procedures. • Unlike the earlier “take it or leave it” offshore voluntary disclosure programs, examiners are directed to develop cases by using appropriate information-gathering tools to determine proper tax liabilities and applicable penalties. • The Memorandum cautions that under the new voluntary disclosure practice, taxpayers are required to promptly and fully cooperate during civil examinations. • The IRS expects that all disclosures made under the practice will be resolved by a closing agreement with full payment of taxes, interest and penalties for the relevant disclosure period. • Failure to cooperate with civil examination could result in the IRS examiner requesting CI to revoke the preliminary acceptance. • The Memorandum relies on IRM 9.5.11.9.4 for purposes of providing guidance on the meaning of cooperation. • Will required cooperation include an in-person interview of taxpayer? STEP Mid-Atlantic Branch

Civil Resolution Framework • The Memorandum introduces a new “Civil Resolution Framework” and grants the IRS discretion to extend this framework to non-offshore (i.e., domestic) voluntary disclosures that have not been resolved but received on or before September 28, 2018. • Following is the protocol governing the Civil Resolution Framework: • In general, a six-year disclosure period (down from eight in the 2014 OVDP) will apply to all voluntary disclosures • However, while this is a general rule to apply to the most recent six-tax years, disclosure and examination periods may vary as follows: • For voluntary disclosures not resolved by agreement, discretion is delegated to the examiner to expand the scope of the years at issue (i.e., beyond six years) to include the full duration of the non-compliance and may also asset maximum penalties under the law with the approval of IRS management. STEP Mid-Atlantic Branch

Civil Resolution Framework (continued) • The practitioner needs to carefully consider the applicable “open” tax years at issue and is a corollary to those years that might be time barred by the applicable limitations. • A major hazard here is Section 6501(c)(8) which can open up tax years back to 1998. • However, in cases involving fewer than the most recent six tax years, the Memorandum prescribes that the voluntary disclosure must correct non-compliance for all years involved. • With IRS review and consent, the six-year disclosure period may be expanded for cooperative taxpayers who wish to include additional tax years for various reasons: • Correcting tax issues with other governments that require a lengthier tax period. • Correcting tax issues before the sale of acquisition of an entity. • Correcting tax issues related to unreported taxable gifts and prior tax periods. STEP Mid-Atlantic Branch

Civil Resolution Framework (continued) • Under the Civil Resolution Framework, taxpayers must submit all required returns and reports for the disclosure period. • Based on such submission examiners will determine applicable taxes, interest and penalties based on existing law and procedures. • As to the assertion of penalties, the Memorandum provides prescriptive guidance as reviewed below. • The civil fraud penalty set forth in Section 6663 will apply to the one tax year with the highest tax liability. Alternatively, the civil penalty under Section 6651(f) for the fraudulent failure to file tax returns can apply (this is a new wrinkle). • In “limited circumstances” IRS examiners may apply the civil fraud penalty (whether based on Section 6663 or Section 6651) to more than one year within the six-year disclosure period and possibly up to all six years based on “facts and circumstances of the case” (e.g., no agreement is reached as to tax liability). • In the event taxpayers fail to cooperate and resolve the examination by agreement, examiners are authorized to potentially apply the civil fraud penalty beyond the six-year disclosure period – presumably for all “open” tax years. STEP Mid-Atlantic Branch

Civil Resolution Framework (continued) • Willful FBAR penalties will be asserted in accordance with existing IRS penalty guidelines under IRM 4.26.16 and 4.26.17 (i.e., for one year during the disclosure timeframe). • This would be tantamount to a willful FBAR penalty equal to 50 percent of the maximum aggregate undisclosed amount of offshore assets, potentially subject to expansion to 100 percent in extraordinary cases. • Taxpayers are permitted to request imposition of accuracy-related penalties under Section 6662 in lieu of civil fraud penalties or non-willful FBAR penalties instead of willful penalties. • The Memorandum cautions that given the “objective of the voluntary disclosure practice” granting such requests for lesser penalties “is expected to be exceptional.” • No examples are given; however, the taxpayer must provide convincing evidence to justify why the civil fraud and willful FBAR penalties should not be imposed where the facts and law support such penalties. STEP Mid-Atlantic Branch

Civil Resolution Framework (continued) • Penalties for failure to file information returns will not be automatically applied (e.g., failure to file Forms 5471, 8858, 926, etc.). • IRS examiners are granted discretion to take into account the application of other penalties such as the civil fraud penalty and the willful FBAR penalty and resolve the examination by agreement. • The Memorandum specifically indicates that penalties relating to excise taxes, employment taxes, estate and gift tax, etc. will be addressed by IRS examiners based on the facts and circumstances, and examiners are directed to coordinate with appropriate subject matter experts. • Note that the mark-to-market alternative to the statutory PFIC calculation provided by former OVDP FAQ #10 does not appear applicable under new procedures if Form 8621 needs to be filed. STEP Mid-Atlantic Branch

Civil Resolution Framework (continued) • In a major departure from the prior “take-it-or-leave it” voluntary disclosure iterations, taxpayers “retain the right to request an appeal” with the IRS Office of Appeals. • The Memorandum indicates that the IRS will provide specific procedures for IRS civil examiners to request revocation of the preliminary acceptance when taxpayers fail to cooperate with civil disposition of cases. • Finally, the Memorandum prescribes that relevant IRM sections will be updated within two years of November 20, 2018 (why is this taking so long?) • Interestingly, the contact persons for inquiries are LB&I Austin representatives, no surprise. STEP Mid-Atlantic Branch

Panelists STEP Mid-Atlantic Branch

Alan Winston Granwell (Moderator) is an international tax attorney. His tax practice encompasses counseling both corporate and private clients. In his private client practice, Mr. Granwell advises high-net-worth individuals on cross-border income, estate and gift tax planning, controversy and compliance, to include foreign persons becoming U.S. persons, and U.S. persons moving offshore or expatriating. He also advises on FATCA and CRS matters and assists clients with bilateral treaty mutual agreement procedures. Mr. Granwell is a former International Tax Counsel and Director, Office of International Tax Affairs, of the U.S. Department of the Treasury. Holland & Knight LLC | 800 17th Street N.W., Suite 1100 | Washington DC 20006alan.granwell@hklaw.com | Phone +1 202 469-5455 | Mobile +1 202 378-0344 Robert Y. Hottle a CPA and personal financial advisor, provides tax and financial advice to high-net worth individuals and families, corporate executives and closely held-businesses. He is a member of Baker Tilly's Private Client Group and serves as a technical reviewer for matters related to high-net-worth individuals including income, estate, gift tax, trust and tax exempt foundation returns. He also reviews international tax reporting for individuals and corporations. Baker Tilly Virchow Krause, LLP | 8219 Leesburg Pike, Suite 800, Tysons, VA 22182-262 Robert.Hottle@bakertilly.com | +1 703 923 9335 Paul G. Marcotte, Jr. is Chair of his firm’s tax practice. He concentrates his practice on federal, state and international tax matters, to include planning, compliance and controversy matters, estate and wealth preservation and business succession planning. He represents a broad spectrum of U.S. and foreign based clients. Paley Rothman | 4800 Hampden Lane, 6th Floor, Bethesda, MD. 20814-2930 pmarcotte@paleyrothman.com | +1 301 656 7603 STEP Mid-Atlantic Branch

Jeff Neiman is an experienced trial lawyer who regularly defends individuals and corporations in white collar criminal litigation matters. As a former Assistant United States Attorney for the Southern District of Florida, he worked at the forefront of the U.S. government’s offshore tax enforcement efforts. He has deep experience in assisting clients who find themselves with unreported or undeclared bank accounts outside of the U.S., and advises clients regarding the IRS Voluntary Disclosure Programs, as well as clients who face civil and criminal penalties for failing to file FBARs. Marcus Neiman & Rashbaum LLP | One Financial Plaza, 100 Southeast Third Ave., Suite 805 jneiman@mnrlawfir.com | +1 305 400 4260 William M. Sharp, Sr. (Speaker) is an international tax attorney with more than 35 years of experience representing clients in a wide variety of international tax planning and controversy matters. His tax practice also focuses on globally oriented high-net-worth clients, including U.S. and foreign-based family offices. Mr. Sharp has served as lead counsel with respect to U.S. Tax Court, Internal Revenue Service (IRS) appeals and examination cases and FBAR cases in Federal District Court. He also has served as lead counsel or co-counsel in well over 1,500 IRS voluntary disclosure cases. Holland & Knight | 100 North Tampa Street, Suite 4100 | Tampa, FL 33602william.sharp@hklaw.com | Phone +1 813 227-6387 | Mobile +1 813 220-7184 Holland & Knight LLC | 50 California Street, 28th Floor | San Francisco, CA 94111Phone +1 (415) 743-6966 | Mobile +1 81) 220-7184 STEP Mid-Atlantic Branch