Download

1 / 12

120 likes | 135 Views

Explore market opportunities in Vietnam's food, lifestyle products, health & beauty, textiles, garments, automobiles, leather, and service industries. Learn about market trends, challenges, and potential solutions for foreign exporters.

E N D

Industry of VietnamSOME MARKET INFORMATION MS. Busaba Butrat Thai Trade Center Hanoi May 2012

Some industries with their market information The focus will go to: • Food & Foodstuff; • Lifestyle products/ fast moving consumer products; • Health & Beauty products; • Textiles & Garments; • Automobiles; • Leather products; • Service industry.

Potential Market Have good significant opportunities due to the strong growth in Vietnam food & foodstuff sector with increased trade liberalization; Increasing in demand for imported foods and foodstuff especially in the large urban centers such as Hanoi, HCMC, Danang, Hai Phong, Can Tho; Favour destination for tourists; Domestic food manufacturing increased; Increasing demand for higher value chilled frozen and grocery products in Vietnam The country processed food industry is growing rapidly with the ingredients importing increased 10% year on year for the last 6 years. Market segmentation Supply chains are highly fragmented, inefficient & dominated by agents or middlemen; Can work both direct or indirect with suppliers or retailers; Food retail Food retail sector is booming currently because of rapidly growing purchasing power of high income- consumers; Modern retail outlets are increasing fast in number; Half of 90 million population is below 30 years old; New emerging class of higher income, younger and more westernized consumers is readily apparent; Food distribution patterns are changing with the expanding into urban areas Challenges - Some non- tariff barriers are used with the food and foodstuff products imported; Vietnam has emerged as a strong importer of food products only over the last 10 years so retailers, importers and distributors still lack of skills in working with partners and improve the distribution; A fragmented and non- transparent supply chain with significant risk to exporters from outside; Food sector is dominated by a large number of small family business so it is hard to establish reputable contacts; Currently the unrestrained growth with inflation has become a significant problem for the exporters in short term at least due to the import un-encourage policy of the government. Suggested solutions for foreign exporters Focusing on the processed food & foodstuff; Capturing new opportunities with new products appearing from the market; Continue the development of relationships with the big food retailers who are interested in direct shipments of products from exporters. Coordinate inward buyer missions of key importers from Vietnam. Food & Foodstuff

Consumer Trends: + The majority are spending less while a few are spending more + The Young generation are the most powerful consumers + Promotion of products made in Vietnam + Hi-tech consumers Distribution channels: + Retailers (traditional channel) & distributors: + Supermarket chains & convenience shops: Modern supermarket and convenience stores include many foreign stores: Family Mart, Malaysia – The garden; Big C group, Metro hypermarket. Local supermarket are regional and popular in HCMC & Hanoi but their operations are instance such as Fivimart, Intimex, Saigon co-op supermarket, etc.. There are only few major distributors of FMCG products in Vietnam such as Unilever and Colgate – Palmolive. Most of distributors are small and only strong in the regions that they are based in and concentrate more on the channels of wholesaling of media or above – the –line promotions. Distribution margins Foreign distribution companies entering Vietnam need to be aware that the profit margins differ according to your company’s relationship with the supermarkets. Product margins for supermarkets range between 15- 25% across the board. Lifestyle Products & Fast moving consumer goods (FMCG)

Regulations: all health & beauty products imported must be registered with the Ministry of Health (MOH) for quality insurance and identification purposes; The foreign company should contract with a local company that can help the foreign company to change the registration status of imported goods and deal with different local distributors if any problem occur. The process of product registration is quite complex and confused with foreigners so the local company will help to make it easier and more efficiently. Very potential market Vietnam shares 5% of the beauty product market in ASEAN currently Vietnam is expected to be big as Singapore (9%) in 2015 The growth is fast recently with the continuing growth of economy and people ‘s income Sales mostly in big cities especially in Hanoi & HCMC with 5 times bigger from HCMC Demand for imported goods is increasing fastly. Most favourable ones from Korea, EU, Japan, Thailand, US, and some others. Problems & regulations There are too many fake products Have to find out the suitable way of distribution practices for products (Exclusive national distribution; non- competing regional distribution; nationally tiered distribution). Health & Beauty Products

Situation 2011 Turnover was $14.5 billion accounted for 3% of world’s garment & textile turnover ($480 billion); Included in the list of the top five leading exporters globally; In most big markets such as the US, EU, Japan, retailers accounted for 70%-90% of the market share; only 10-30% belonged to commercial businesses and producers; Problems & Challenges for 2012 The industry is facing with problems of its structure and production method; The industry needs around 400,000 tones of cotton yearly but domestic production could meet a tiny of 0.75% of the demand. The industry continues to import 100% of its spare parts and 70% of the materials; Low production capacity of enterprises leading to less competitive and other countries; The industry do not have direct access to markets but have to operate through middlemen; Lacking of capital and mainly dependent on bank loans. Slow in production expansion and technology upgrade due to the high interest rates; Solutions Should be restructured as soon as possible; Focusing on building and expanding the distribution system; Focus on building Vietnamese trademarks especially in neighboring countries such as Laos, Cambodia, Myanma and increasing co-operation with foreigners. Call for more investment to improve the facilities and enrich the capital for production toward exporting. Turnover for the first 4 months of 2012 reached $4.4 billion, up 14.7% despite the shrinking demand in the US, Japan and Europe; Target of 2012 is $18.5 billion for exporting garment and textile; Focusing on boosting exports to countries which signed bilateral or multirateral free trade agreements with Vietnam already such as Republic of Korea; The government is now actively negotiation bilateral free trade agreements with Japan, EU and on way to join the Trans – Pacific Partnership (TTP) agreement Textile & Garments

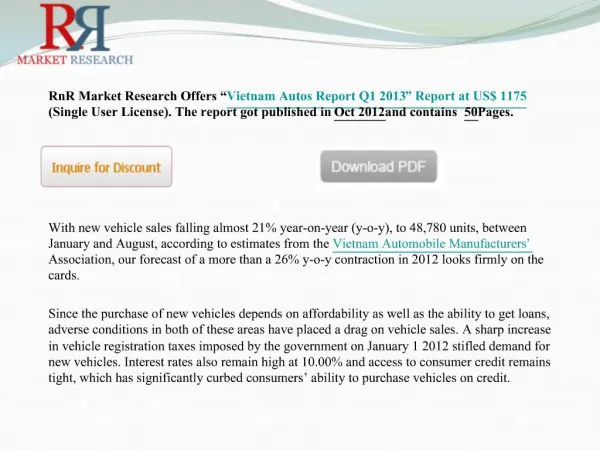

Automobiles Cars sales in march 2012 2011 Situation • New vehicle sales in Vietnam fell by 2% year on year over 2011 to reach 110,020 completely built units; • December 2011, vehicle sales reached only 10,937 units, down 12% in the same period of 2010; • In term of manufacturers, the local manufacturer Truong Hai Auto Joint Stock Co (thaco) has displaced long time market leader Toyota Motor Vietnam in term of new vehicle sales in 2011; • Current outlook is mixed due to some factors: high inflation with 18.3% 2011; weak currency, heavily taxed accounting for 60% of the value of a new car. 2012 situation • Increase the car ownership registration tax rates with fewer 10 seats from 12%- 20% in Hanoi and 10%-15% in HCMC; • Vehicle sales in beginning of 2012 decreased a lot with all VAMA members; • Estimated sales may fall 20% this year; • The industry is forecasted to be in a very difficult situation this year. • VAMA has asked for supports from multi – functioned local authorities to loosen the policies with automobiles instate of seeing them to withdraw from Vietnam market.

Members of Vietnamese Automobile Manufacturers Association (VAMA) There are 17 members of VAMA chaired by Toyota Motor Vietnam • Ford Vietnam Ltd. • GM Vietnam Company Ltd • Hino Motors Vietnam Ltd • Honda Vietnam Ltd • Isuzu Vietnam Ltd • Mekong Auto • Mercedes – Benz Vietnam Ltd • Saigon Transportation Mechanical Corp (SAMCO) • Sanyang Industry (SMV) • Toyota Motor Vietnam • Truong Hai Auto • Vietnam Motors • Vietnam Suzuki Corp. • Vina Star Motors Corp. (Mishubishi Motors) • VN Engine & Agricultural Machinery Corp (VEAM) • VN National Coal& Mineral Industries Group (VINACOMIN) • Xuan Kien Private Enterprise (VINAXUKI)

VIETNAM LEATHER & FOOTWEAR INDUSTRY 2011 STATISTIC 1. Export Value 2011: Shoes and footwear products: 6.549 billions USD Bags & leather handbags: 1.289 billions USD 2. Production Capability Shoes and footwear products: 850 millions pairs Finishing leather products:350 millions sqft Bags & leather handbags: 200 millions units ENTEPRISES STATISTICS By Enterprise Models: State Owner2 Private & Company Ltd.195 Joint Veture54 100% Foreign Capital38 Joint Stock Company56 Limited6 By Industries: Shoes231 Tanning 29 Material56 Suitcases, handbages, bages32 Repairing equipment3 By Locations: Ho Chi Minh207 Binh Duong39 Dong Nai30 Ha noi26 Hai Phong18 Hai Duong5 Thua Thien Hue4 Da Nang4 Can Tho3 Vinh Phuc3 Leather Products

Achievements Has achieved outstanding results in terms of exports considering it is still in its infancy in Vietnam; Tourism remains the main export item in service industry with a large and increasing number of tourist year by year; Export of transport services, represented mainly by shipping; Telecom services are the third major export with the going up revenues for the last ten years; Promising market for foreigners Demand for service industry especially in tourism such as hotels, resorts, as well as transport and telecom are increasing; Service industry is seen as one of the targeted industry of Vietnam for economic development so receiving a number of promoted policies form the government and; Private sector is put consideration to invest in this industry Challenges Limitations in term of policy/regulations Service providers lacked size and inexperienced; Lack of facilities and public infrastructure; Has not been focusing on exporting services. Service Industry

Thank you ! Office of Commercial Affairs, Royal Thai Embassy Hanoi Suite 801, floor 8th HCO Building 44 B Ly Thuong Kiet- Hanoi, Vietnam Tel: 84-4 3 9365226-7 Fax: 84-4- 39365228 Email: thaitchanoi@depthai.go.th