Download

1 / 20

200 likes | 297 Views

Equilibrium Price. When the Laws of Supply and Demand Collide. Diminishing Marginal Utility .

E N D

Equilibrium Price When the Laws of Supply and Demand Collide

Diminishing Marginal Utility • As a person increases consumption of a product - while keeping consumption of other products constant - there is a decline in the marginal utility that person derives from consuming each additional unit of that product.

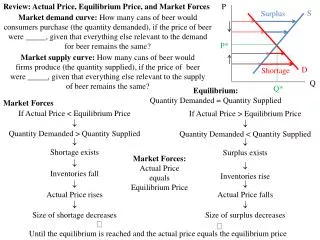

Equilibrium • Def. The point at which quantity demanded and quantity supplied come together.

Disequilibrium • If the market price or quantity supplied is anywhere but a equilibrium price, the market is in a state called disequilibrium. • Interactions between buyers and sellers will always push the market back towards equilibrium…. • Unless the government interferes

Government Interference • In some cases, the government steps in to control prices. • Exs: Price ceilings and price floors.

Price Ceiling • Def: A maximum price that can be legally charged for a good • Ex: Rent Control: A situation where the government sets a maximum amount that can be charged for rent in an area. Usually in large cities- NYC or LA

Price Floor • Def: A minimum price, set by the government, that must be paid for a good or service. • Ex: Minimum Wage- sets a minimum price that an employer can pay a worker for an hour of labor • Ex: Luxury or “Sin” Taxes- items like alcohol, cigarettes and gas have extra taxes

Problems with Price Floor and Ceilings • Both prevent markets from reaching equilibrium. They prevent suppliers from producing as much as price dictates or prevents consumers from buying as much as they wish. • Ex- Rent control; prevents landlords from getting full value. • Ex: Cigarette taxes-prevent people from buying them=reduce the # of smokers

Equilibrium • The point where supply and demand meet can change for 3 reasons:

1. Change in Supply • Excess supply leads to a surplus (when supply is greater than demand). This leads to a decrease in price and in increase in demand. - Ex: After Christmas sales • A decrease in supply leads to an increase in price. This leads to a decrease in demand.

Do Now- Review! • Answer the following questions: • 1) What is the Law of Demand • 2) What is the Law of Supply • 3) What is Profit? • 4) What is Elasticity of Demand • 5) What is Elasticity of Supply

2. Change in Demand • If there is a shortage, when demand is greater than supply, price rises, which increases supply and decreases demand • Ex: Tickle Me Elmo • When demand falls, suppliers cut prices and find a new equilibrium

3. Change in Price • As prices change, supply and demand will both change.

So why are prices important? • Prices are vital in a free market economy • They help move land, labor and capital into the hands of producers and finished goods to buyers. • Price is a language both consumers and producers can use to determine value.

Advantages of Price • 1. Price as an Incentive Price shows to buyers and sellers whether a good or service is scarce or easily available. Encourage or Discourage production. 2. Price as Signals (Traffic Light) - A high price (green light) tells produce to make more. Low Price (red) tells producers to make less

Advantages cont. • 3. Flexibility of Prices • Prices are generally more flexible than production levels, can be easily increased or decreased 4. Price System is “Free” A distribution system based on price costs nothing to administer, unlike in command economies

How does scarcity of an item affect its price? • If there is a scarcity on an item, then the price will be high. • Ex: Gasoline

How does a boycott affect the price • If an item is being boycotted, then the price often will go down. • Ex: If everyone stopped buying gas, the price would drop

How does the war in Iraq affect the price of certain items? • Price of many items have increased (ex: gas and security)