Download

1 / 23

240 likes | 475 Views

Equilibrium Price. The magical price where the quantity demanded is equal to the quantity supplied. Price. $3.00. 27. Quantity. $0.50. 30. $1.00. 25. $1.50. 19. $2.00. 15. $2.50. $3.00. 10. $1.50. 30. Demand and Supply. Quantity. $0.50. 4. $1.00. 12. 5. 19. $2.00. 25.

E N D

Equilibrium Price The magical price where the quantity demanded is equal to the quantity supplied.

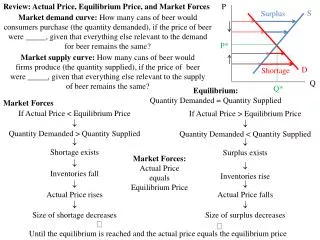

Price $3.00 27 Quantity $0.50 30 $1.00 25 $1.50 19 $2.00 15 $2.50 $3.00 10 $1.50 30 Demand and Supply Quantity $0.50 4 $1.00 12 5 19 $2.00 25 $2.50 Price • Price effect of demand • As price increases the quantity demanded increases • Price effect of Supply • As price increases the quantity offered for supply decreases. Demand for Milk ( millions of gallon per week) Supply for Milk ( millions of gallons per week)

The Magical Price Everyone Wins <Suppliers sell all they want to sell <Demanders buy all they want to buy.

What if the price is lower than the equilibrium? • Shortage • Buyers want to buy more than sellers want to sell.

A Market Left Alone Seeks Equilibrium What? • In a shortage: • Buyers will compete for the scarce items, driving the price up. • If I can’t get a gallon of milk for $0.50 I'll pay $1.00 to get the amount I want. • Sellers offer more as the price moves upward. • I can sell more gallons of milk at $1.00 than I can at $0.50

Why Would We Have Shortages? Rent control & price ceilings • Government control of housing prices. • Student housing in the Boston area • Housing in NY City • The market seeks equilibrium in other ways ( other ways to compete for scarce resources) • NY City Key deposits • Quality of housing - lack of incentive to build and improve.

WWII Food Price Ceiling Gov’t set price for food - demand greater than supply • Non market competition (the way around it) • Buy direct from farmer at legal set price. Buy farmers dog for extra price. • Let dog go because of no dog food. • Dog returns to farmer.

1970's Gas Shortages • 1972 oil embargo drove world gas prices up • The U.S. government keeps prices below the Market Clearing Price in form of price ceilings • Buyers want more than seller want to sell. • Non market competition develops in the form of lines ( opportunity cost)

What if the price is above equilibrium? Surplus The demander buys less then the supplier wants to sell.

A Market Left Alone will Seek Equilibrium In a Surplus A. The sellers compete for the scarce sells driving the price down. B. As the price decreases the # of buyers increases. C. the process continues until equilibrium is reached

Why would we have a surplus? Government subsides & price floors • US Minimum Wage • Require employers to pay workers over the market clearing price • More supply of worker than demand = poor quality • Less jobs • Less training • competition for the job in non market ways

Changes in Supply and demand An Increase in the Demand & other things ( supply) being equal An increase in price & an increase in quantity demanded

Changes in Supply and demand An increase in Supply & other things ( demand) being equal <A decrease in price and An increase in quantity

Changes in Supply and Demand PA decrease in Demand & other things ( supply) being equal <A decrease in price & a decrease in quantity demanded PAn Decrease in Supply <An increase in price a decrease in quantity

Changes in Supply and demand Other possibilities PDecrease in supply increase in demand PIncrease in Supply decrease in demand PDecrease in supply decrease in demand PIncrease in supply increase in demand

Supply and demand in the US agriculture market What is the problem? PUS farm policy <Policy to control the supply BLand bank programs <Tax incentives to help farmers <Why not market price?

The functions of markets and prices in the free enterprise system. PInform <Do they value what I have? PIncentive <Produce low & sell high <Buy low PRationing Function <Who gets what stuff? <What will be produced? <How will it be produced?

The price system and the five fundamental questions How does the price system: <1. Determine what is to be produced <2. Organize Production <3. Distribute total output <4. Accommodate change <5. Communicate and coordinate individuals free choices

What to produce Profits, profits, profits PEconomic Profit -businesses must secure all four type of economic resources <Land, labor, capital, entrepreneurial ability <Payments must be made to secure the resources. Receipt of sales is greater then the costs for resources = Economic Profit PDollar Votes - consumers vote for type and quantities of produced by demand.

Organizing Production PHow should resources be allocated among specific industries? PWhat specific firms do the producing in each industry? PWhat combination of resource- what technology- should each firm employ. <Consumer demand, low production costs = profits

Accommodate Change The price system communicates changes to firms: PChange in consumer demands PChange in availability of resources PChanges in technology or production methods <The firm must adapt to changes to remain competitive.

A The Invisible Hand@ The organizing mechanism of competition. PProduce what is in demand and get it to the consumer at the lowest possible price PNew firms push better quality and production methods PNew products developed to satisfy consumer demands PNew entrepreneurs compete for the consumer dollar and a profit.

Questions to discuss P1. What is equilibrium? P2. What is a shortage? P3. What is a surplus? P4. What is a price ceiling? Give an example. P5. What is a price floor? Give an example P6. Do you support price floors and ceilings? Explain P7. Should we do about the US agriculture problem? P8. What are the functions of markets and prices in the free enterprise system?