Download

1 / 22

220 likes | 343 Views

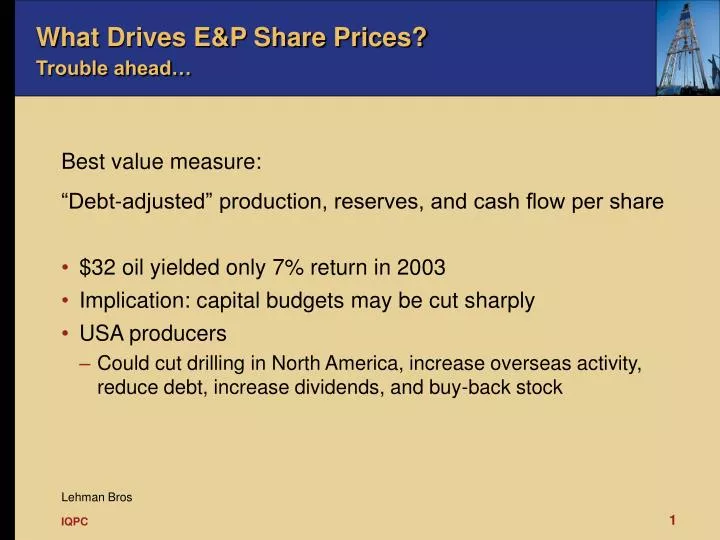

What Drives E&P Share Prices? Trouble ahead…. Best value measure: “Debt-adjusted” production, reserves, and cash flow per share $32 oil yielded only 7% return in 2003 Implication: capital budgets may be cut sharply USA producers

E N D

What Drives E&P Share Prices? Trouble ahead… • Best value measure: • “Debt-adjusted” production, reserves, and cash flow per share • $32 oil yielded only 7% return in 2003 • Implication: capital budgets may be cut sharply • USA producers • Could cut drilling in North America, increase overseas activity, reduce debt, increase dividends, and buy-back stock Lehman Bros

…AND the Next Decade(s)Capital requirements could be exponential… 130 ? World Oil Supply vs. Demand: A.G. Edwards (MMBOPD) ? $4-6 Trillion 86 82 9 30 47 2030 2010 2004 CERA

New World: More Refineries GTL Increased Demand New World: Importance of Gas Old World: Unconventional Resources Decline in Production Capital Planning & Discipline Implications for E&P CompaniesCapital planning will take on new dimensions... 130 ? ? 2030

New World: Traditional Range of Investment OptionsClassic planning and capital allocation approach works… “Conventional” • Oil & gas prospects • Associated gas flaring • Very deep water • Stranded operations • H2S, CO2 mixtures • Severe climates

“Conventional” • Oil & gas prospects • Associated gas flaring • Very deep water • Stranded operations • H2S, CO2 mixtures • Severe climates Old World: Range of Investment Options IncreasingExpanded need for planning and capital allocation discipline… Unconventional Liquids (COP) Unconventional Gas (USGS) • Oil shales • Extra heavy oil • Oil sands • Bitumen • Coal bed methane • Tight gas • Fractured shale gas • Not discreet but continuous • Recovery is the issue not size of resource • Manufacturing style development • Proven, but needs commercial production • Exploration more like development SPE 94667

Old World: Unconventional Gas Of the top 12 U.S. onshore gas giants, 10 are unconventional… USA Onshore Gas Giants of the 1990’s Name EUR Play Type • Newark East – Barnett Shale 26,200 BCF continuous shale gas • Powder River CBM 24,000 BCF coalbed methane • Jonah 3,300 BCF basin centered gas • Pinedale 2,000 BCF tight sands • Madden Deep (Conventional) 2,000 BCF structural • Vernon 1,800 BCF tight sands • Ferron Coal Play Utah 1,500 BCF coalbed methane • Freshwater Bayou (Conventional) 1,500 BCF structural • Dew – Mimms 1,200 BCF tight sands • Bob West 1,100 BCF structured tight sands • Deep Giddings 900 BCF fractured carbonates • Dowdy Ranch – Nan Su Gail 700 BCF tight sands

Old World: Unconventional OilWestern Hemisphere reserve base is enormous… Billion Barrels Extra-Heavy Unconventional Potential Conventional Proved Sources: Venezuela Potential from PDVSA Statements Reported OGJ Dec 2003 Canada Potential from NEB Energy Market Assessment May 2004

Old World: Unconventional Oil TypesInitially in place… Type Location Canada 36% United States 32% Oil sands and bitumen 39% Oil Shales 38% Other 13% Venezuela 19% Extra heavy oil 23% 7 trillion barrels Source: International Energy Agency based on Cupcic, Dyni & IHS Energy

Model the System Identify “Pinch Points” Define Variability Holistic Project Description – Proposed Decision ChainA system thinking perspective is important… Integrated Planning: End-to-End Line of Sight The Reservoir The Well Bore The Facilities The Market SPE 49092

Plateau Life Applied Facility Constraint Initial Production Area = Volume Decline Curve Cumulative Production Classic: Reservoir & Well BoreBreaking down the production profile… Reservoir Well Bore Facilities Market SPE 90440

Initial Production Area = Volume Cumulative Production Improved: Review Production ProfileFocusing on the other key factors… Reservoir Well Bore Facilities Market ProductionProfile • Plateau rate • Decline rate • Ramp up • Drilling constraint • Well bore constraint • Production efficiency • Facility constraint • Market constraint SPE 90440

Well Bore & FacilitiesBenefits for intelligent completions… Reservoir Well Bore Facilities Market 5% Reduced Well Intervention Costs Operator targets: $300-500M of added value per year 25-35% improved well lifecycle value 7% Accelerated Production 13% Reduced Well Costs 22% Reduced Surface Facilities Costs 53% Increased Ultimate Recovery Relative Business Impact SPE 94672

San Diego De Cabrutica Old World: Facilities and MarketExtra heavy oil example… Reservoir Well Bore Facilities Market ConocoPhillipsLake Charles Refinery Loading Monobuoyand Solids Marine Terminal PDVSA Paraguana Refining Complex VENEZUELA CARIBBEAN SEA Upgrading Complex Jose BARCELONA AnzoáteguiState 200 KmPipelines 20” Diluent 36” Diluted Crude Orinoco river Production Field Development

Old World: Facilities and MarketTar sands example… Reservoir Well Bore Facilities Market A Mechanical Engineers Dream • Large reserves • Mining with shovels & trucks • Separation with steam & water • 80% in situ • Horizontal parallel wells .. steam from gas fueled generators • Upgrading & refining

New World: Facilities and MarketLNG example… Reservoir Well Bore Facilities Market

A Word About Price – Drives New InvestmentsOil supply infinite; depending on price… • At: • $15/bbl, some light oil profitable • $20/bbl, heavy oil attractive • $30-40/bbl, oil from coal (SASOL) • $50+/bbl, renewable energy • At some price, gas from chemistry (C+H) • Heavy oil, tar sands, shale oil, coal liquids, unconventional gas – all depend on $$, facilities & technology Geo. Stosur SPE Distinguished Lecturer

Making the Best Investment DecisionEntering phase of “Super-Investment”…

Model the System Identify “Pinch Points” ROV Real Option Valuation Making the Best Investment Decision Get the math right… Disciplined planning needed for $ multi billions investments The Reservoir The Well Bore The Facilities The Market Stochastic L/P Deterministic Tools

Production Facility Midstream Storage Transportation Downstream Refining Suggested insights and techniques have been applied Commercial Marketing Holistic Project Description – Help is AvailableWhere should we look for lessons learned? Exploration Classic approach may be less valuable over time E&P Production Upstream Petroleum Industry

Restating the Problem…The business case for better forecasting… • In the next decade • Projects will become more complex • Global efforts are the norm, not the exception • JVs are the standard operating model • Competition for capital exists across the integrated asset chain The planner’s ability to routinely anticipate and model the key business drivers, especially those external to your company, will determine your effectiveness.

Future Production Forecasting Much more than a sum of decline curve forecasts… • Define the problem we are trying to solve • Set a business model to frame analysis • Ensure line-of-site across entire decision chain • “Get the math right” - use the most appropriate method • Define the best tool(s) to run the analysis • Test, test, test for reasonableness … in business to make money, not just find oil & gas