Download

1 / 2

20 likes | 134 Views

NI CENTRAL INVESTMENT FUND FOR CHARITIES Investment Factsheet as at 30 September 2012. Background. Fund Information. 3 months to 30 September 2012. Fund Performance. Aim

E N D

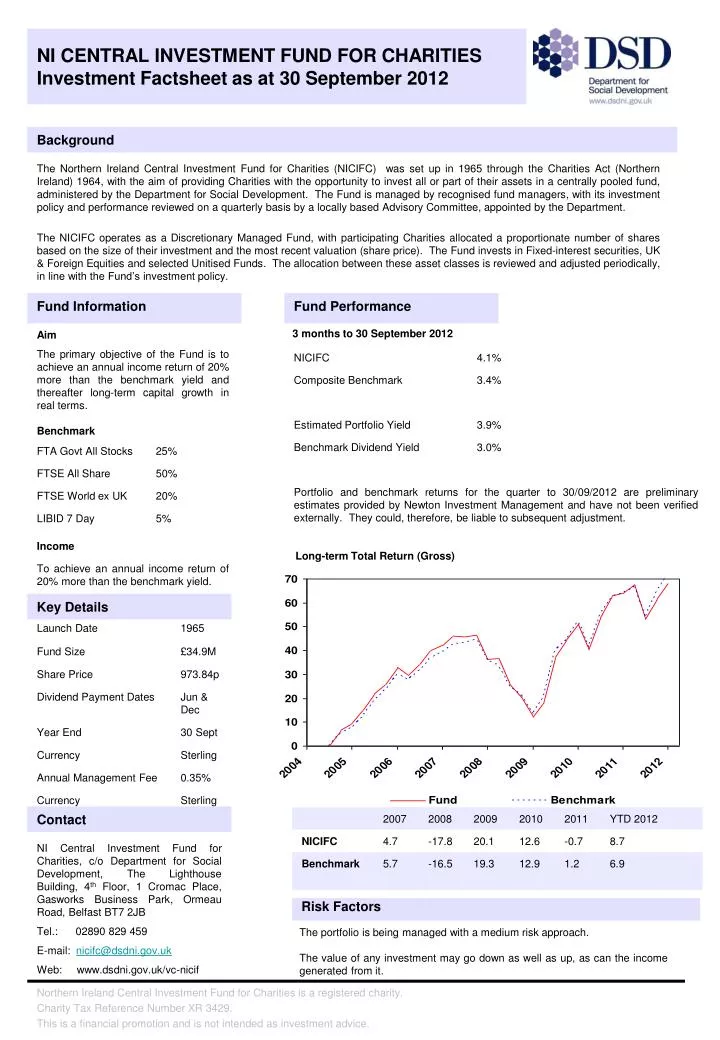

NI CENTRAL INVESTMENT FUND FOR CHARITIES Investment Factsheet as at 30 September 2012 Background Fund Information 3 months to 30 September 2012 Fund Performance Aim The primary objective of the Fund is to achieve an annual income return of 20% more than the benchmark yield and thereafter long-term capital growth in real terms. Benchmark Income To achieve an annual income return of 20% more than the benchmark yield. Long-term Total Return (Gross) Key Details Contact NI Central Investment Fund for Charities, c/o Department for Social Development, The Lighthouse Building, 4th Floor, 1 Cromac Place, Gasworks Business Park, Ormeau Road, Belfast BT7 2JB Tel.: 02890 829 459 E-mail: nicifc@dsdni.gov.uk Web: www.dsdni.gov.uk/vc-nicif Risk Factors The portfolio is being managed with a medium risk approach. The value of any investment may go down as well as up, as can the income generated from it.

NI CENTRAL INVESTMENT FUND FOR CHARITIES Investment Factsheet as at 30 September 2012 Fund Manager Ethical Restriction: No direct investment permitted in tobacco stocks. Sector Allocation as a % of Total Market Value NICIFC Fund Composition Newton Investment Management Limited, Queen Victoria Street, London. Newton is a global thematic stock picking company. This focus on themes helps to identify the catalysts for change and capture opportunities wherever they occur. Newton were first appointed by the Department as managers of the Fund in August 2004 and then reappointed in February 2009, following a successful retendering exercise. Historic Fund Information Source: Newton Investment Management, as at 30th September 2012 Market Commentary Recent European Central Bank and Federal Reserve measures marks a notable shift towards a more inflationary policy stance, being intended explicitly to raise the prices of financial assets. It is doubtful, however that such measures will be effective in bringing about economic enhancements sought by authorities. The true antidote to the ailment of too much debt is, indeed, an improvement in economic activity, but real growth will be hard-won in a world so laden with the burden of past excesses. There is a distinct threat, meanwhile, that the intervention of authorities create new hazards in economies and financial markets. As an authoritative paper by William White of the Organisation for Economic Cooperation and Development highlights, ultra-loose monetary policy risks bad investments (owing to distortions in price signals and the availability of credit), damage to the health of financial institutions, and negative effects on wealth and income distribution. In combination, these dangers, Mr White argues, “support strongly the proposition that aggressive monetary easing in economic downturns is not “ a free lunch” In the months ahead, the friction between policymaking and debt repayment in the major regions is liable to cause further volatility in financial markets, as well as sparks in the economic and political machinery of affected countries. There is a pronounced divisive regional elections, the US presidential election and ensuing efforts to tackle the country’s tax and spending ills, and the change of leadership in China provide ample uncertainty. In managing portfolios, balance appears key. Paying heed to the impact of near-term policy making, but remaining focused on the more enduring forces that will shape the investment landscape is likely to be essential. In a world increasingly preoccupied with the short term, opportunities should continue to arise for those attentive to the long term.