Download

1 / 11

0 likes | 26 Views

Debt Nirvana empowers individuals with valuable insights on enhancing their credit scores through five strategic approaches. Emphasizing the significance of responsible credit management, the company advises on reducing debt, particularly keeping credit utilization below 30% to maintain a favorable credit profile. Stressing the importance of a meticulous credit history examination, Debt Nirvana encourages individuals to obtain and scrutinize their credit reports for accuracy, suggesting the engagement of a third-party Debt Collection firm if necessary.

E N D

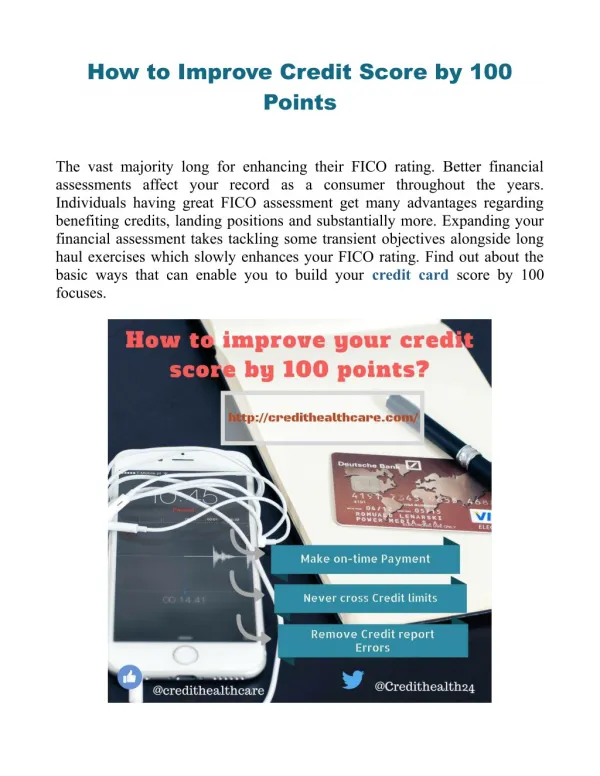

5 ways to improve your credit score In a nutshell, it is a long-term representation of your credit activities. As a result, excellent credit activities result in a better credit profile and a strong CIBIL score. Whereas poor credit activities result in a negative credit profile and a weak CIBIL Score. And that is what will affect your potential credit facilities. Upon approving your loan or credit card request, lenders will look at your CIBIL Score. This is to learn more about your credit record, behavioral patterns, and payback records. • When you begin your credit experience with a card or a loan, you leave a credit impression. This imprint is essential for the growth of your creditworthiness and CIBIL Score.

1. Cut down on your debt • 2. Examine your credit history • 3. Don’t request credit too frequently • 4. Don’t close old accounts instantly • 5. Create an automatic bill payment system • 5 ways to increase your credit score:

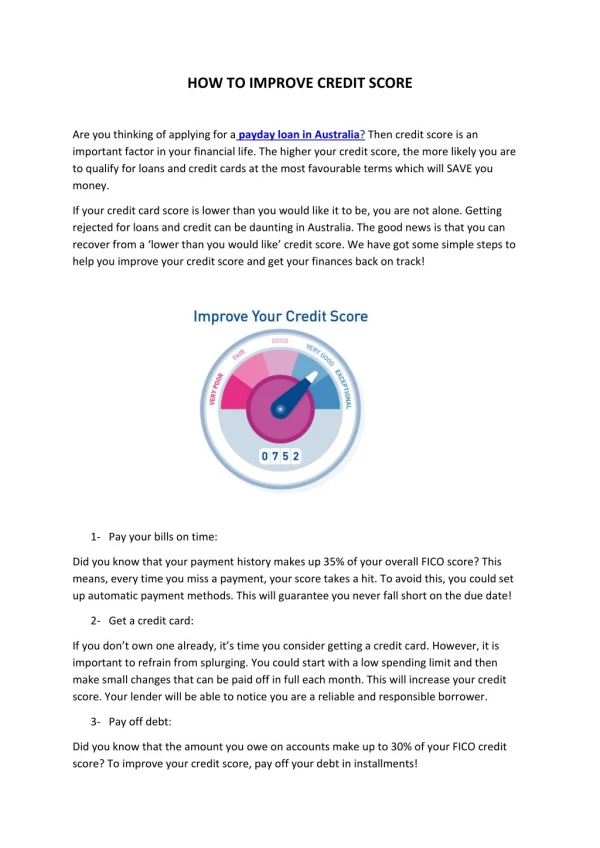

1. Cut down on your debt: Creditors want you to borrow a certain amount of money, but not too much. When you utilise more than 30 percent of your overall credit limit on all of your credit cards, lenders usually roll their eyes. Your credit utilisation score is only up to 30% of your Fair Isaac Corporation (FICO) score. A lack of activity might sometimes be a concern. You can request that electricity bills or any other standard payment services be put to your credit report even if you don’t use a credit card. When it comes to fixed-rate mortgages like property or vehicle loans, lenders will look at your debt-to-income ratio, which shows how much of your annual earnings go toward debt repayment. Your debt-to-income ratio has no bearing on your credit report, but if it’s too high, you might not be able to get a loan. Pay off the debt quickly if your account is about to blow out. You can even try transferring funds from your savings account to pay off your credit card. When all other factors are equal, paying off a credit card with an 18% interest rate is about equivalent to generating 18% on investment.

2. Examine your credit history: Your credit analysis is a comprehensive record of all of your credit transactions, and it’s what’s utilised to calculate your credit score. You can also engage a 3rd party Debt Collection firm to assist you in maintaining your credit records. You must obtain a copy of your credit report because your credit score may struggle if it is inaccurate. You can also double-check that your name hasn’t been hacked. Make sure your biographical details are correct, including your identity, location, mobile number, and Identification Number. Check your credit amounts and limitations, as well as the accuracy of your credit card details.

3. Don’t request credit too frequently: Getting a new credit card periodically, as well as taking out a vehicle home loan, should not harm your credit. Lenders maintain a count of how many times you ask for credit. Since individuals who fail on credit tend to build up a lot of debts before they collapse. New queries 10 % of your total FICO score. When a creditor considers providing you a loan, they will look at your credit record.

4. Don’t close old accounts instantly: 15% of your credit score is based on the period of your previous account, the period of your current account, and the mean lifespan of all your accounts. It’s okay to let an account payable build rust as far as you’re not paying interest charges on it. The more you have credit, the more your score will improve.

5. Create an automatic bill payment system: Using credit report services India, create an automatic bill payment system if you have the funds but tend to forget to provide them. You won’t have to go and withdraw money because your payments would be completed before the deadline.

Conclusion If you’re late for the payment period, a late payment will often appear on your credit report. This will show a negative impact on your CIBIL score. To avoid such circumstances create this payment system. Our Business Information reports are one of the most trusted sources of business data and we provide the best Debt Collection Service India. For any further queries, connect our experts at +91-9810010294 or visit our website.

Hire our expert debt collectors todays! Contact us : USA : 101 California Street Suite 2710 , San Francisco, CA 94111 Phone : 415 6516478 India : Kalkaji , New Delhi PIN – 110019 Phone : +919810010294 0129-4040294 Singapore : 403 Bedok North Avenue 3 11-239, Rainbow Ville 460403 Phone : 6531595194

Please visit our website and social media account: https://www.instagram.com/debtnirvana/ https://debtnirvana.com https://www.facebook.com/DebtNirvana/ https://in.linkedin.com/company/debt-nirvana https://twitter.com/DebtNirvana