Download

1 / 35

350 likes | 604 Views

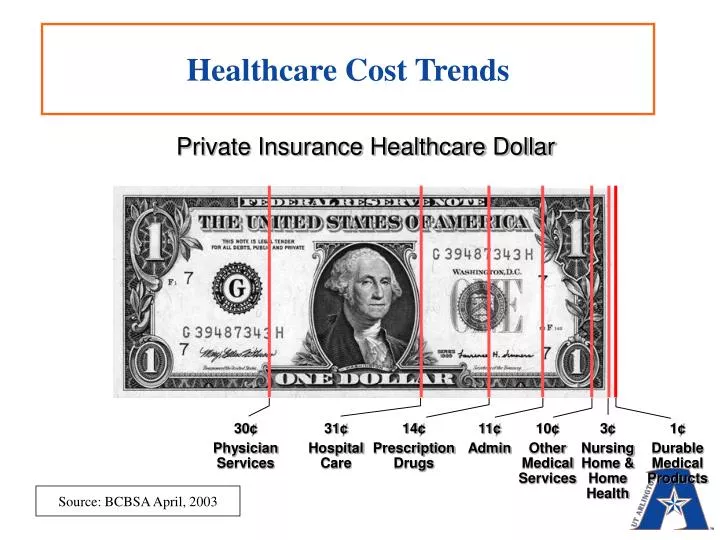

Healthcare Cost Trends. Private Insurance Healthcare Dollar. 30 ¢ Physician Services. 31 ¢ Hospital Care. 14 ¢ Prescription Drugs. 11 ¢ Admin. 10 ¢ Other Medical Services. 3 ¢ Nursing Home & Home Health. 1 ¢ Durable Medical Products. Source: BCBSA April, 2003.

E N D

Healthcare Cost Trends Private Insurance Healthcare Dollar 30¢ Physician Services 31¢ HospitalCare 14¢ PrescriptionDrugs 11¢ Admin 10¢ Other Medical Services 3¢ Nursing Home & Home Health 1¢ Durable Medical Products Source: BCBSA April, 2003

US Attitude Toward Health Care Benefits • Entitlement attitude: Employees feel it is a right due to them by their employer • Similar to pension plans turning to consumer driven 401(k) plans - we have been seeing health care plans taking this path of consumer driven

Definitions - Benefit Plans • Traditional Indemnity Plans • Major medical plan design, usual coinsurance of 20%, with a deductible • Managed Care • Health Maintenance Organizations: HMOs • Preferred-Provider Organizations: PPOs • Point-of-Service Plans: POS

Common Forms of Managed Care Vary in Degree of Integration • HMO: a closed system, providing comprehensive services, assuming full financial risk • POS: combines HMO style controls (e.g. gatekeeper) with PPO freedom to go outside • PPO: allows out-of-plan usage (with higher co-pays) generally fee-for-service Most Degree of Integration Least

Recent Factors Influencing the Growth of Health Benefit Costs Aging Population • U.S. male’s healthcare spending doubles in the 45 to 54 age group; rises 50% in the 55 to 64 group • In the US, One in five people will be 65 or older by 2030.

Key Cost Drivers: Hospital Nursing Shortage Nurse Shortage Growing More Acute Required Shortage of 434,000 Nurses in 2020 Available Source: U.S. Census Bureau data, Internal Release Date: April 2, 2001; and National Sample Survey of Registered Nurses, 2002, HRSA, Bureaus of Health Professions, Division of Nursing

Obesity and Sedentary Lifestyle Factors • Chronic disease • Impaired physical function • Impaired quality of life • At least 300,000 premature deaths • About $90 billion in annual U.S. direct health care costs Archives of Internal Medicine

Annual Change in Average Total Health Benefit Cost, 1996-2005

Total Health Benefit Cost for Active Employees: All Employers 1996-2003

Average Annual Premium Costs for Covered Workers, Single and Family 2005

Percent of Premium Paid by Workers 2000-2005 Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2005

History of Medical Expense Coverage Reaction to Spiraling Costs • HMO Act (1973) introduces federal policy support for managed care provided through organized delivery systems • Self-funding of benefits • Cost-shifting to employees • Managed care

CONSUMERISM • Employees will now need to be aware of the actual costs of their health care and to become savvy health care consumers.

Future Outlook • Smaller Employers hit harder ….. • The threshold of pain for employers is 12%--at which point employers take action (Mercer, 2003) • What things look like if employers do nothing? Chart

Responses by Smaller Employers • 19% made changes to health plans • 65% increased deductibles and co-pays • 35% switched insurers • 30% increased employee share of premium • 29% cut back on scope of benefits • 26% increased the scope of benefits EBRI, January 2003 Issue Brief

Prescription Drug Facts • Spending on prescription drugs rose 11.3% last year, rising to $182 billion • Constitute only a relatively small proportion of overall health care spending (about 9.4%), but • Prescription drug costs accounted for 44% of the increase in total health care spending • Controlling prescription drug costs is a primary issue in controlling the rise in health care costs • Fastest-growing component of health care spending

Growth in Prescription Costs • Increased utilization • More drugs being prescribed • Multiple drugs to treat multiple conditions • Physicians greater trend to treat using drugs • Increased drug prices • Lack of true competition in the market • Increased Direct-to-Consumer Marketing

Growth in Prescription Costs • Promotion of drugs to providers • Drug samples • Highest cost drugs are most commonly prescribed • High priced drugs have rapidly rising prices • High priced drugs are most heavily advertised

Employers Pay Biggest Portion of the Cost Percent of US Drug Expenditures by Payer 43.9% 34.3% 21.8% Source: Prescription Drug Trends, Kaiser Family Foundation (November 2002)

Versus Consumers Who • Want access to the “best” drugs • Generally don’t have knowledge of how much the drug actually costs when paying a small co-pay • As a result of direct-to-consumer advertising, the consumer is more aware of the drugs that exist that may improve their health and lifestyle • More likely to try new meds and fill Rx • Process endears providers to patients

Drug Cost Control Strategies • Preferred drug lists & formularies • Use of multi-tiers • Increase co-pays • Percentage co-pays • Expanded use of generics • Require participating doctors to write “brand necessary.”

Drug Cost Control Strategies (cont.) • Drug utilization review (DUR) • To catch overuse, interactions, length of use, etc. • Disease management • Use of managed care • Cover over-the-counter drugs • Pharmacy counseling • Consumer education • Evaluation of pharmacy benefit managers (PBMs)

Retiree Health Care • Stagnant economy + fast-rising health care cost = hastened decline of retiree health benefits

Firms That Offer Retiree Health Coverage, 1993 - 2003 Source: Mercer National Survey of Employer-Sponsored Health Plans, 2003

Retiree Health Benefits Trends Percentage of Firms Offering Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2003

Retiree Health Care • Stagnant economy + fast-rising health care cost = hastened decline of retiree health benefits • Watson Wyatt survey of 56 larger employers (5,000+) • 20% have already eliminated retiree plans for new hires • 17% now require retirees to pay the full premium

Disease Management (DM): Approach • Preventive programs to educate and get the proper services into the hands of patients with chronic illnesses • Chronic illnesses regular hospital utilization • Prescribed routine of wellness, prevention and treatment to avoid or to delay acute episodes.

Disease Management Programs • Purpose: Improve quality of care and health outcomes while decreasing health-care costs • Companies purchase these services through their insurance provider or separately from DM companies such as Health Management Corporation

Disease Management • Focus on conditions including: • high blood pressure, high cholesterol • excess weight; diabetes • Asthma; heart conditions, oncology • In 2002, 11 chronic conditions accounted for 58% of total health-care plan payments Watson Wyatt

Percentage of Firms’ Opinions on the Effectiveness of Cost Containment Strategies Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2003

Eliminate Health Care Insurance • Trend among smaller employers has been to eliminate health care insurance: • 60% of the 41 million that do not have insurance are members of families who own or work for small businesses. • Cash-out option: One alternative to offering benefits • The employer pays workers higher wages in lieu of insurance. The worker can choose to buy health insurance on the individual market. • Shifting employer dollars from benefits to wages.