Download

1 / 29

350 likes | 728 Views

The Rising Cost of Healthcare. What’s Causing the Growth & How to Reduce the Impact on your Benefits September, 2006. Goals of Presentation. Interpret national premium trends on a local basis Understand factors that drive higher healthcare premiums

E N D

The Rising Cost of Healthcare What’s Causing the Growth & How to Reduce the Impact on your Benefits September, 2006

Goals of Presentation • Interpret national premium trends on a local basis • Understand factors that drive higher healthcare premiums • Examine where healthcare dollars are spent • Discuss tactics to reduce costs • View examples of how RSI clients have offset increases 43%

What did premiums do in 2005? • 9% increase nationally for employer-sponsored plans • Averaged for all plans types, all employer sizes & all regions • Captures premiums paid relative to 2004 (not actual renewal) 43% • Sources: • The Factors Fueling Rising Healthcare Costs 2006, PricewaterhouseCoopers; • Employer Health Benefits 2005 Annual Survey, Kaiser Family Foundation

How did RSI renewals compare in 2005? • Average initial renewal: 19% • Average final renewal: 10% To date for 2006: • Average initial renewal: 17%* • Average final renewal: 7% 43% * Break-out renewal average for NJ SEH groups: 30%

Premium growth: What drives it? 30% Cost Increases Above Inflation 27% General Inflation Increase in Healthcare Premiums 2005 43% Increased Utilization

Increased Utilization-The biggest piece of the pie • Aging- older employees use more services • Lifestyle- continued deterioration of health (obesity, smoking, inactivity) • New technology- treatments once not available, now in demand • Defensive medicine- physicians over utilize services to avoid litigation 43%

Increased Cost-The 2nd driving force • Intensity- higher cost alternatives replace older methods (imaging, labs) • Market consolidation - payers yielding slightly to greater compensation for providers • Cost shifting – uninsured burden weighs on private market 30%

Cost management strategy #1: Manage rates (short-term) • Groups impacted: all sizes/ rating methods • plan design changes (higher copays, deductibles) • shop carriers • plan design changes worth greatest savings can vary over time within same carrier

Cost management strategy #2: Shift cost (short to long term) • Groups impacted: all sizes/rating methods • within plan: shift more significant responsibility to user (hospital copay, coinsurance) • outside of plan: modify contribution schedules • outside of plan: base plans and buy-ups

Cost management strategy #3: Change participant behavior (long term) • Groups impacted: greatest for larger, experience rated/self-funded • wellness programs • risk assessment profiles • disease management • consumer-driven care

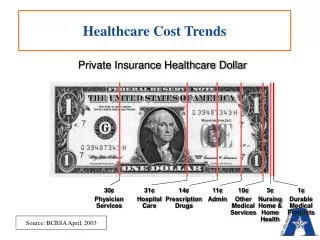

Physician costs (21¢):Encourage prevention, reduce unnecessary utilization • Higher specialist copays • Maintain 100% prevention coverage 21¢

What is the average office visit benefit in today’s group? $20 PCP copay $25 Specialist copay Options: • Increase office visit copays • Increase differential between PCP/Specialist

Client Example #1: Changing the Office Copay Client: Northern NJ client with 170 employees Carrier: Horizon BCBS 2005 Renewal: Change: $10 PCP/ $10 Specialist to $20 PCP/ $20 Specialist Savings: $19,000 (1.4%) 2005 2006 Renewal: Change: $20 PCP/ $40 Specialist- 1% $25 PCP/ $50 Specialist- 2%

Outpatient (18¢) lab/radiology copays surgery copays in-network deductible Inpatient (17¢) hard to reduce inpatient costs by plan designs can shift cost using copays can limit costs using network restrictions Hospital costs (35¢): Keep focus on early intervention & prevention 35¢

What is the average O/P benefit in today’s group? 40% of clients: no cost-share O/P surgery 80% of clients: no in-network coinsurance Options: • Include some lab/radiology cost share • Include O/P surgery cost share • Add in-network coinsurance

Clients Example #2: Adding Outpatient Cost-Sharing Client: NewYork Client with 350 employees Carrier: Cigna Change: $100copay for MRI/PET/CT Scans $200 copay for O/P surgery Savings: $95,530 (5.5%) Note: Savings reduced to $91,532 (5.3%) when employer reimburses 100% of new copays

What is the average I/P benefit in today’s group? 75% of clients: no cost-share I/P hospital 25% of clients: hospital copay (average $350) Options: • Add/increase hospital copay • Self-fund reimbursement to employees • Consider reducing OON benefit- low impact to most employees

Client Example #3: Adding Hospital Copay Client 1: North NJ Client with 100 employees Carrier: Horizon BCBS Change: $500 per admission hospital copay Savings: $7,800 (1.1%) Client 2: North NJ Client with 75 employees Carrier: Oxford Change: $500 per admission hospital copay Savings: $30,500 (5.5%)

Client Example #4: Reducing Out-of-Network Benefit Client 1: SouthNJ Client with 450 employees Carrier: Horizon BCBS Change: Reduction in OON fee schedule from 80% to 70% Savings: .9%

Rx costs (15¢):Encourage use for maintenance & prevention • 3-tiered formularies • significant gap between generic & brand (at least $10) • exclusions (lifestyle drugs) • initial deductible • mail-order benefit 15¢

What is the average Rx plan in today’s group? 77% have 3-tiered: $10/$25/$40 23% have 2-tiered: $10/$20 1 client has initial deductible Options: • Increase copay at brand & non-formulary level • Change non-formulary coverage to coinsurance • Add deductible • Self fund Rx component

Client Example #5: Self-funding Rx Client: Northern NJ Client with 205 employees Carrier: Aetna Change: Self-funded Rx Savings: Reduced overall medical/Rx increase from 28% to 23% for $48,000 savings

Client Example #6: Adding Rx Deductible Client: Northern NJ Client with 90 employees Carrier: Horizon Change: Added $75 Rx deductible to $20/$40/$60 copay Savings: Reduced Rx premium $6500 (7%)

Adding value to benefits without cost • Voluntary benefits • life • disability • long-term care • Cafeteria plans • pre-tax contributions • FSA for unreimbursed medical (copays, deductibles, Rx) • dependent care expenses • Communicate value of benefits • benefit statements • Use benefit committees to empower employees

Wrap-up of Presentation • National trends can provide some local insight into the drivers of cost • No silver bullet for curbing premium growth • Approach to cost containment will vary based on rating of group, carrier and group’s benefit philosophy • Tactics outside of benefit plan can help to create value for employees in face of decreased benefits or increased cost 43%

If you have any questions about the information in this presentation, please contact your RSI Consultant at 800.394.6111. info@rsionline.com www.rsionline.com 43%