Download

1 / 28

280 likes | 396 Views

MSP LANDSCAPE OVER THE NEXT 3 YEARS. Presenters. Chris Martin GFI MAX Bob Godgart Co-Founder of ChannelEyes Jay McBain Advisor at ChannelEyes. Myth #1 | It is ALL about the Services. Myth #1 | It is ALL about the Services. BALANCE. Myth #2 | It is ALL about the Cloud.

E N D

Presenters • Chris Martin GFI MAX • Bob Godgart Co-Founder of ChannelEyes • Jay McBain Advisor at ChannelEyes

Myth #2 | It is ALL about the Cloud DELIVERING WHAT IS BEST FOR YOUR CUSTOMER

1 Mobility Almost anything can be IP and Touch Enabled QR • 2012Smart phones Overtake PCs. • Pervasive Computing takes hold • and drives consumerization of IT Mobility In IT…

Cloud – Changing the Business Model in IT 2 Stock Broker… Insurance Broker… Telecom Agent… Cloud Broker? • Cloud. It’s simply a service, one of many.So, control the relationship and take the payment! • Once a commodity, Service is the differentiator! • Margins small. Add services to improve RPC • Maintain long term customer relationshipsContinually evaluate options or your customer will

3 Cloud DrivesNew Vendors - Lots of Them! How Many Vendors Do You Use Today? In 3 Years: How Many WILL You Have? Several product categories have seen explosive growth: - CRM has over 1,000 competitors - EMR has over 300 viable solutions in the US alone - Cloud backup and disaster recovery has grown to hundreds of vendors

Markets Converging on IT 4 Developing Vertical Specialty • Products IP Enabled, Connected • New Products, Revenue Models • They are Coming to your World! New Products New Revenue Models

5 Industry Vertical Specialization • New expertise required in response to expanding Government regulation and legislation around the world • Significant new complexity and confusion requiring industry and technology “micro-segmentation”

6 The World Continues to Flatten • Managed Services and Cloud technologies continue to remove geographic competitive barriers • Industry specialization and deeper solution expertise trumps local presence Competition is based on “what you can deliver” as opposed to where you are located

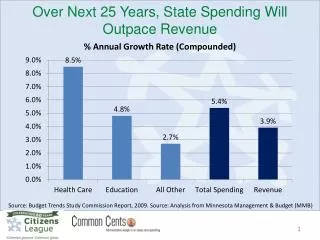

7 Commoditization Drive Margins Even Lower • Credit and financial issues spark innovation around pricing and packaging of traditional Managed Services • Geographic and specialized competition challenge margins Cloud, consumerization and global economic issues weigh on Channel profits

8 Channel Landscape Continues to Change • Number of Partners worldwide will continue to drop by 5% per year. • Consolidation will continue - other major Technology and Retail organizations will announce MSP acquisitions The Managed Services market has matured over the past 10 years both in delivery quality and the technology supporting it.

9 The Customer is Changing As Well • Demographic shift happening in IT departments as well as small business entrepreneurs • Accelerating many of these trends including cloud, mobility and social media Understanding the changing customer is critical in planning for the future.

10 Social Media Changes Marketing • Quantity of noise is growing exponentially • Return on Investment tough to track and measure – can be a resource suck • Business Social fuels momentum into communities

10 Business Social in IT • Social interaction is “now” part of business • It isn’t an application – it’s a conversation. • Business Social will emerge in every app.

Impact on The Channel? Mobility Information Overload + Cloud + It’s a BIG Problem! Convergence + Social + Number of Vendors

The Channel Program Challenge “Tremendous amounts of time and energy go into creating materials stored in web portals, but they receive little traffic.” - EVERY Channel Chief Only 17% open Program email (2% Click-thru) What About You? Few Partners Filter and Distribute Info Less Than 5% Use Vendor Portals …Only Gets to Champion or Gatekeeper EMAIL PORTAL NEWSLETTERS • Partners who leverage Vendor Programs are most successful!

Business Social for the Channel Yesterday: channel broadcasting Today: channel “social graph” buying groups vendors associations industry experts consultants and coaches media community and peer groups distributors • Unsecure, unfiltered • Irrelevant, ignored

The Channel Is Evolving Announcements Sales & Marketing Incentives The first secure, social network for Suppliers and their Channel Partners. It’s kind of like Facebook, but instead of friends – it’s a filtered group of Vendor feeds on a Social Wall. Product Info Tech Bulletins Train/Certification Feeds From: • Vendors • Manufacturers • Distributors • Associations • Master MSPs • Franchises • And More…

The Channel Is Evolving • Aggregate Secure • Program Feeds • Relevant Content • Social Conversations • Partner Program Pages • Any Web Device!

Benefits: ChannelEyes Social Network Cut Through Program Noise and Clutter: • All Channel Program Highlights securely in one place • Leverage web portal and other assets • The right program info gets to the right people • Top of Mind: More participation in Channel Programs • Multiple contacts per Partner. Deeper engagement • Crowdsource feedback on new programs / incentives • Social Conversations around program content • The Result: Better Sell-thru! Bigger Bottom Line.