Download

1 / 30

300 likes | 439 Views

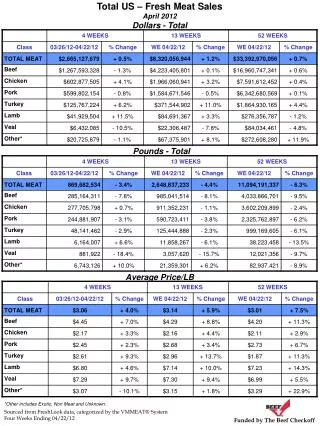

Total Tea Sales Were Relatively Stable. Consumer Sales of Total Tea Total Grocery-Mass-Drug (Millions). Pounds. Dollars. % Chg. % Chg. Total U.S. -*52 Weeks Ending 7/22/00. The Pounds Sale Decline Was Driven By Less Tea Purchasing Per Shopping Trip.

E N D

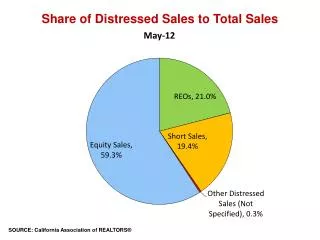

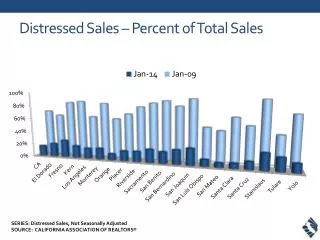

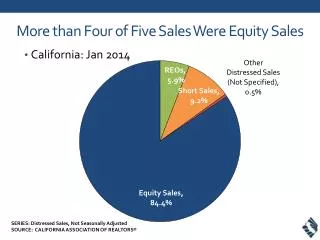

Total Tea Sales Were Relatively Stable • Consumer Sales of Total TeaTotal Grocery-Mass-Drug (Millions) Pounds Dollars % Chg % Chg Total U.S. -*52 Weeks Ending 7/22/00

The Pounds Sale Decline Was Driven By Less Tea Purchasing Per Shopping Trip • Household Purchase Dynamics of Total TeaAll Outlets

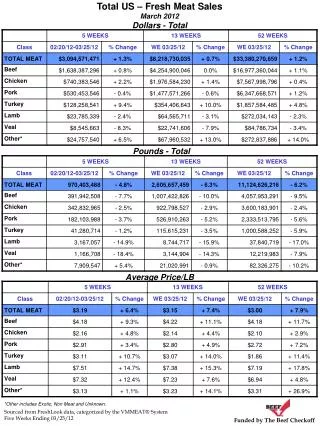

Grocery Remains The Dominant Tea Channel • Consumer Sales Of Total Tea(Millions) Pounds Dollars Note: Mass Merch includes SuperCentersTotal U.S. -*52 Weeks Ending 7/22/00

Grocery Dollar Sales Are Gaining Due To Higher Prices And The Increasing Importance Of R-T-D • Consumer Sales Of Total Tea Dollars Grocery $2MM+ (Millions) Total U.S. - *52 Weeks Ending 7/24/99 or 7/22/00

However, Grocery Tea Dollars AreContinuing Recent Declines • Consumer Sales Of Total Tea Pounds Grocery $2MM+ (Millions) Total U.S. - *52 Weeks Ending 7/24/99 and 7/22/00

The Growth Of Mass And DrugHave Offset Grocery • Consumer Sales Of Total TeaTotal Grocery-Mass-Drug (Millions) Total U.S. -*52 Weeks Ending 7/22/00

Ready-To-Drink Contributes Significantly To Dollars, But Is A Great Deal Less Important To Pound Sales • Share Of Tea Sales By TypeDollars Versus Pounds – Total Grocery-Mass-Drug Pounds Dollars Total U.S. -*52 Weeks Ending 7/22/00** Three Outlets = Grocery $2MM+, Drug, Mass Merch

Tea Bags/Green Tea Has Stabilized, While RTD Continues To Impact Iced And Instant • Share Of Tea Pound Sales By Type — Grocery $2MM+ Note: Tea Bags include Green Tea (4.9 share in 2000*)Total U.S. - *52 Weeks Ending 7/24/99 or 7/22/00

Volume Expansion Was Fueled By Green Tea Gains, While Dollar Growth Was Powered By Ready-To-Drink • Tea Sales Growth 1999-2000 By TypeTotal Grocery-Mass-Drug (‘000) Pounds Dollars Total U.S. -*52 Weeks Ending 7/22/00

Both Buying Households And Increased Tea Purchasing Drove Green And R-T-D Gains • % Change in Penetration — All Outlets Total U.S. -*52 Weeks Ending June 2000

Dollar Sales Growth Was Fueled By Increased Pricing Across All Tea Types … • Tea Price Per Pound ChangesTotal Grocery-Mass-Drug Price Per Pound % Chg vs Year Ago Total U.S. -*52 Weeks Ending 7/22/00

Green & Herbal Achieve Significantly Higher Premium Pricing To Mainstream Tea • Tea Dollar Sales by Price PointTotal Grocery-Mass-Drug RegularTea Bags IcedTea Opportunity? $ Herbal Dollars (Millions) Decaf Tea Bags Green LooseTea Instant Tea Price per Pound Total U.S. -*52 Weeks Ending 7/22/00

Ready-To-Drink Is Especially Important In Drug, However Tea Bags Dominate Across All Outlets • Division of Tea Pound Sales within Channels By Type – Grocery $2MM+ Grocery$2MM+ Drug Stores Mass Merchant Total U.S. -*52 Weeks Ending 7/22/00

Grocery Is Still The Key OutletFor Regular Tea Bag Sales • Consumer Sales Of Regular Tea Bags Pounds Dollars Total U.S. -*52 Weeks Ending 7/22/00

Regular Tea Bag Volumes Declined Slightly, But Dollars Sales Gained • Consumer Sales Of Regular Tea Bags(Millions) Total U.S. -*52 Weeks Ending 7/22/00

RTD Tea Continues Strong Dollar Growth, Capturing 37% Of Tea Grocery Dollars • Ready-To-Drink Tea — Grocery $2MM+ Dollar Sales (Millions) Dollar Share of Tea Total U.S. -*52 Weeks Ending 7/24/99 or 7/22/00

Ready-To-Drink Provided The Sole Tea Gains Within The Supermarket ($2MM+) Channel • Volume Gains 1999-2000 — Tea Pounds (000s) Regular Tea Bags Herbal Tea Instant Tea Iced Tea Mix Loose Tea Green Tea Ready-To-Drink Tea Drug Stores Regular Tea Bags Herbal Tea Instant Tea Iced Tea Mix Loose Tea Green Tea Ready-To-Drink Tea Mass Merchandisers Regular Tea Bags Herbal Tea Instant Tea Iced Tea Mix Loose Tea Green Tea Ready-To-Drink Tea Grocery $2MM+

Finally, There Are Distinct Differences In The Demographics For The Growth Segments • Demographic Insights • Tea Bags • Large Families, Older Children, South, Rural, Less Affluent • Green Tea • Small Households, No Kids, 55+, East/West, Urban • Ready-To-Drink • Large Families, Middle-Aged (35-54), East, Urban • Kids 6-17 Ethnic Households, Affluent • Demographic profiles are largely unchanged since 1996 Total U.S. -*52 Weeks Ending June 2000

Decaf Tea Growth Is Outpacing Regular, Accounting About 13% Of Sales • Total Grocery-Mass-Drug Total U.S. -*52 Weeks Ending 7/22/00

In Fact, Decaf Tea Bag Sales Helped Offset Regular (Caffeinated) Tea Bag Losses • Tea Bags Gains By CaffeinationTotal Grocery-Mass-Drug (‘000s) Pounds Dollars Total U.S. -*52 Weeks Ending 7/22/00

Decaf’s Presence Is Strongest In Tea Bags • Volume Share Of Decaf Tea By TypeTotal Grocery-Mass-Drug Note: Dollar Mix is similar to Volume MixTotal U.S. -*52 Weeks Ending 7/24/99 and 7/22/00** Three Outlets = Grocery $2MM+, Drug, Mass Merch

Decaffeinated Growth Was Sourced Almost Entirely From Tea Bags And Ready-To-Drink • Decaffeinated Tea Sales Growth 1999-2000 By Type • Total Grocery-Mass-Drug (‘000s) Pounds Dollars Total U.S. -*52 Weeks Ending 7/22/00

Bottled Water Market Has Grown10 Fold Since 1976 • U.S. Bottled Water Market1976-1997, Gallonage Thousands of Gallons Year Source: Beverage Marketing Corporation, New York

Water Is A $2.6 Billion Dollar Market, Growing Over 20% • U.S. Bottled Water Market — 1976-1997, Gallonage * Food, Drug, Mass, Convenience, Petro

We Must Continue To Find New Ways To Leverage The Benefits Of Tea • Tea Based Beverages • i.e. Minute Maid and Snapple Iced Tea, Lemonade/Lemonade Iced Tea • Tea Based Frozen Specialties • i.e. Tea Flavored Ice Pops (recruit young consumers early) • Dietary Supplements • i.e. Anti-Oxidant Tea Pills • Tea Based __________________