Download

1 / 6

60 likes | 71 Views

This study examines the proposals and actions taken by major pension funds from 1987-1993 and their impact on target firms' policies, organization, governance, and long-term performance. The findings suggest that while pension fund activism leads to changes in management and board turnover, shareholder lawsuits, and other events, it does not result in significant long-term improvements in performance. The study also discusses the limitations of measurement techniques in detecting small improvements in performance.

E N D

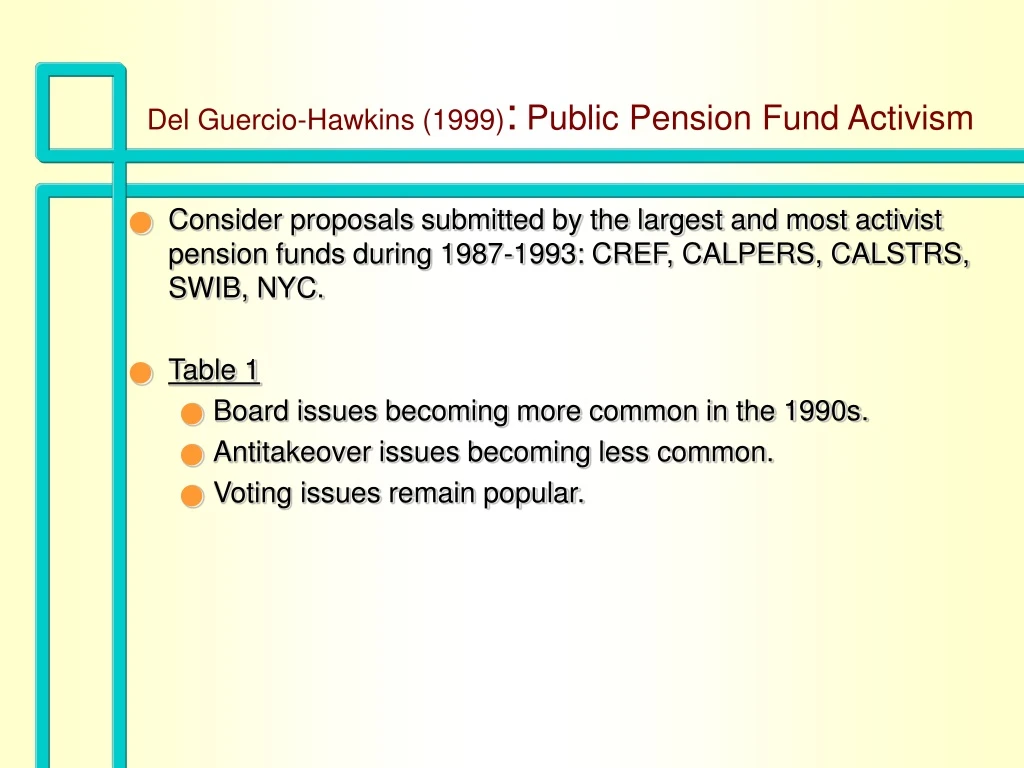

Del Guercio-Hawkins (1999): Public Pension Fund Activism • Consider proposals submitted by the largest and most activist pension funds during 1987-1993: CREF, CALPERS, CALSTRS, SWIB, NYC. • Table 1 • Board issues becoming more common in the 1990s. • Antitakeover issues becoming less common. • Voting issues remain popular.

Del Guercio-Hawkins (1999): Public Pension Fund Activism • Table 2 • Total domestic equity portfolio value • CREF: $31.8 billion • CALPERS: $19 billion • Average dollar holding in target firms • CREF: $67 million • CALPERS: $34 million • Total dollar holding in target firms • CREF: $2.1 billion • CALPERS: $1.1 billion • Average % ownership in target firms • CREF: 1% • CALPERS: 1%

Del Guercio-Hawkins (1999): Public Pension Fund Activism • Table 4: Frequency of announced events in the target firm in the four years after the firm is targeted. • Does pension fund activism have a significant impact on target company business policies, organization, and governance? • Management and board turnover is significantly higher for targeted firms. • Shareholder lawsuits and public “no” votes for directors are significantly higher for targeted firms. • Asset sales/spin-offs/restructuring/layoffs are significantly higher for targeted firms. • Table 6: Do pension funds choose targets that are (even without being targeted) likely to engage in above policy/organizational changes? No.

Del Guercio-Hawkins (1999): Public Pension Fund Activism • Impact of pension fund activism on long-term performance • Pages 326-327: No long-term improvement in performance. • Implication of above • Pension fund activism has no long-term improvement in performance. • Measurement techniques are not powerful enough to pick up “small” improvements in performance.

Measurement techniques are not powerful enough to pick up “small” improvements in performance. • Barber and Lyon (Journal of Financial Economics, July 1996) • Accounting operating performance: Return on assets (ROA) after controlling for industry performance: • Superior ROA performance of 1% : Detected 2 times out of 10. • Superior ROA performance of 2% : Detected 7 times out of 10. • Superior ROA performance of 3% : Detected almost every time.

Measurement techniques are not powerful enough to pick up “small” improvements in performance. • Kothari and Warner (Journal of Finance, 2001) • Using state-of-the-art techniques, can we detect superior mutual fund performance? • 100 basis points annual superior performance: Undetected. • 500 basis points: Detected once every three times. • 1500 basis points: Detected (almost) every time. • Ability to detect superior performance improves if one tracks a mutual fund’s stock trades.