Download

1 / 22

220 likes | 357 Views

Default Management in the US Student Loan Program. Tony Glad, Executive Vice President ANZFAA – Sydney 2010. Default Consequences For Schools. A high Cohort Default Rate can: Result in a loss of eligibility for Title IV loans Possibly reduce school eligibility for other sources of funding

E N D

Default Management in the US Student Loan Program Tony Glad, Executive Vice President ANZFAA – Sydney 2010

Default ConsequencesFor Schools A high Cohort Default Rate can: • Result in a loss of eligibility for Title IV loans • Possibly reduce school eligibility for other sources of funding • Affect disbursement policies • Cause extra work to reduce default rate • Cause students to reconsider attending an institution

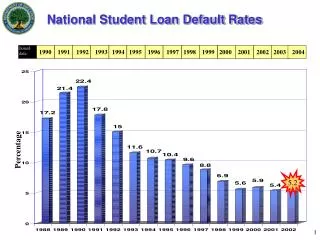

The Challenges Ahead • Loan default rates are on the rise • Educational costs/student debt are rising • The economy • “New” three-year Cohort Default Rate (CDR) calculations and sanctions • “New servicers” - Guarantors and FFELP lenders are no longer strong players

But Remember…That Economy Thing • Cohort Default Rate data is retrospective, and latest published figures are from 2007 • US economy started to decline in 2008 • Unemployment began to increase • Interest rates on Stafford and PLUS locked in at 6.8% and 8.5% (July 1,2006)mean higher monthly payments than early 2000’s

CDR Window Expanding • The Higher Education Opportunity Act of 2008 expands the cohort default rate window from 2 years to 3 years. • Essentially, borrowers have a longer period in which their defaulting can affect their school’s default rate. • Would take foreign schools from 2007 CDR 2.12% to 3.61%. • Curious about you? www.finaid.org/loans/cohortdefaultrates.phtml

CDR Window Expanding – ctd. • Three year rates won’t go into full effect until FY2011’s data is available, so sanctions based on this won’t go into effect until FY2014 • New sanction levels- 3 years at 30% (up from 25%) lead to ineligibility 15% (up from 10%) for 30 day delay for 1st yr and multiple disbursement rules

Three Year Sanctions First year>30% • School must develop a default prevention plan and task force • Submit plan to ED Second consecutive year> 30% • School must review/revise plan • Submit revised plan to ED • ED may require additional efforts Third consecutive year> 30% • Loss of eligibility

Increased School Responsibility • Guarantee agencies and FFELP lenders now out of the picture • Reporting of student loan amounts, revisions, refunds and cancellations must be done by school via NSLDS • A return of funds to G5 is not automatically reported; school must do so via COD and NSLDS

DL Servicers • Multiple servicers used to create an environment of competition to ensure student borrowers receive the best in business service • All of a borrower’s loans should be at one servicer • School may not designate a servicer • Loan volume will be allocated based on default management performance and customer • Satisfaction surveys (borrower, school, ED)

Key Steps to Effective Default Prevention • Counseling strategy • Data collection • Data reporting • Contact with student

Entrance Counseling • Solid counseling program using Entrance Counseling • Required for all first time borrowers in the Federal programs • Can be an institutional requirement for all borrowers • Should be done before student arrives and funds disbursed

Entrance Counseling • Studentloans.gov • Links in with Direct Loan system • Mapping your future • Same process many have been using • Verifying if still allowed for foreign schools • In person presentation • Stronger impact and more dynamic interaction

Exit Counseling • Must be made available to all students when they graduate or cease to be enrolled at least half-time • Harder to enforce than Entrance Counseling • What things have you done? • If student doesn’t attend need to follow up

Exit Counseling Option • Studentloans.gov • Links in with Direct Loan system • Mapping Your Future • Same process many have been using • Still exists – for now • In person presentation • Stronger impact and more dynamic interaction

Missed Exit Counseling? What must you do if a student doesn’t do Exit Counseling before leaving your university? Either: • Ensure that borrower completes interactive electronic counseling, • Mail written materials to the borrower at their last known address within 30 days after learning they withdrew or failed to complete exit counseling.

Data Collection • It is important to maintain current records showing the students • Mailing Address • Phone Numbers • Other contact information • Will be used by servicers chasing the student during delinquency (before a student defaults)

Data Reporting • Keep NSLDS up-to-date with all enrollment data • Easier now there is only one lender, but university now bears full responsibility for reporting – no lender or guarantor will do it on your behalf • Keeping servicer informed when student withdraws • Let them know within 30 days if student leaves before expected completion date

Contact with students • Students are always more likely to want to stay in touch with the university rather than a lender • Maintaining an alumni connection is often best way to make sure you have contact details