Download

1 / 19

• 190 likes • 215 Views

Explore the Capital Asset Pricing Model (CAPM) theory, its application in investment analysis, efficient frontier concepts, risk-free assets, and the Capital Market Line (CML). Learn about market portfolios, risk pricing, separation theorem, and more.

E N D

Capital Market Line Dr. Lokanandha Reddy Irala www.irala.org Lokanandha Reddy Irala 1 Capital Asset Pricing Model

James Tobin (1958) expanded on Markowitz's work by adding a risk-free asset to the analysis. This made it possible to leverage or deleverage portfolios on the efficient frontier. This lead to the notions of a super-efficient portfolio and the capital market line. Through leverage, portfolios on the capital market line are able to outperform portfolio on the efficient frontier. Lokanandha Reddy Irala 2 Capital Asset Pricing Model

Efficient Frontier with short sales • In the presence of short sales, but without risk less lending and borrowing, each investor faced an efficient frontier such as that shown here Rp C B Rp A Lokanandha Reddy Irala 3 Capital Asset Pricing Model

E(rP) T C Y X rf p

Borrowing Portfolios E(rP) C T C Lending Portfolios rf p

E(rP) T rf B rf p

EF-With Risk free lending & borrowing Rp C Ti Rf B Rp A • In the presence of short sales, with risk less lending and borrowing, each investor faced an efficient frontier such as that shown here Lokanandha Reddy Irala 7 Capital Asset Pricing Model

EF-With Risk free lending & borrowing Rp C Ti Rf B Rp A • The tangency portfolio is denoted with Ti • Tidenotes investor i's portfolio of risky assets • The investors satisfy their risk preferences by combining portfolio Tiwith lending or borrowing • In general the efficient frontier will differ among investors because of differences in expectations. Lokanandha Reddy Irala 8 Capital Asset Pricing Model

EF & Homogeneity of Expectations • If all investors have homogeneous expectations and they all face the same lending and borrowing rate, then they will each face an identical frontier • The portfolio of risky assets Tiheld by any investor will be identical to the portfolio of risky assets held by any other investor • If all investors hold the same risky portfolio, then, in equilibrium, it must he the Market Portfolio. Lokanandha Reddy Irala 9 Capital Asset Pricing Model

The Market Portfolio (M) • Is constituted with all assets like bonds, stocks, options, real estate, rare coins, stamps, antiques etc. • Each one of these assets is included in M in proportion to market value of the asset, relative to total market value of all assets • M is a fully diversified portfolio with no unsystematic risk. What remains in the market portfolio is only systematic risk • M is an efficient portfolio. • Market Portfolio in this sense does not exist in reality • A substitute is a market index as Sensex Lokanandha Reddy Irala 10 Capital Asset Pricing Model

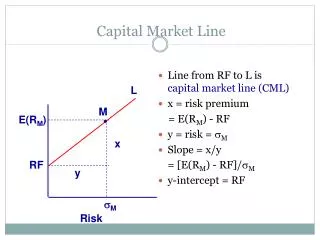

Capital Market Line Rp C (σm, Rm) M Rp B (0, Rf) σp A • The line of tangency with Ti replaced with the Market Portfolio (M) is usually referred to as the Capital Market Line. Lokanandha Reddy Irala 11 Capital Asset Pricing Model

Deriving the Equation of CML • The equation of the straight line in x-y space with (x1, y1) and (x2, y2) as two points in it is given by • The equation of the straight line in Rf-M space with F (0, Rf) and M (σm, Rm) as two points on it is given by Lokanandha Reddy Irala 12 Capital Asset Pricing Model

Deriving the Equation of CML • The term [(Rm - Rf)/σm] can be thought of as the market price of risk for all efficient portfolios. • It is the extra return that can be gained by increasing the level of risk (standard deviation) on an efficient portfolio by one unit. Lokanandha Reddy Irala 13 Capital Asset Pricing Model

Deriving the Equation of CML • The term [(Rm - Rf)/σm] σp is the market price of risk times the amount of risk in a portfolio. • It is that element of required return that is due to risk. Lokanandha Reddy Irala 14 Capital Asset Pricing Model

Price of Time & Risk • The first term is simply the price of time • The return that is required for delaying potential consumption for one period given perfect certainty about the future cash flow. • Thus, the expected return on an efficient portfolio is • (Expected return) • = (Price of time) + (Price of risk) X (Amt. of risk) Lokanandha Reddy Irala 15 Capital Asset Pricing Model

Separation Theorem • All investors will end up with portfolios somewhere along the CML depending on the risk-return preferences. • However, it should be distinctly noted that the Market Portfolio (and hence the CML) is constructed without any reference to the risk-return trade-off curves of the investors • This result is popularly known as the Tobin’s Separation Theorem Lokanandha Reddy Irala 16 Capital Asset Pricing Model

Separation Theorem • The separation theorem states that • the optimal combination of risky assets in the market portfolio is determined without consideration of the risk-return preferences of the investors. • Risk-return trade-off of investors is separate from the constitution of the market portfolio. • The indifference curve is relevant only in the selection of the optimum portfolio Lokanandha Reddy Irala 17 Capital Asset Pricing Model

Limitations of CML • The CML is the locus of only efficient portfolios. The individual assets and inefficient portfolios don’t lie on the CML. • So the CML does not describe equilibrium returns on non efficient portfolios or on individual securities. • We now turn to the development of a relationship that does so • The Security Market Line Lokanandha Reddy Irala 18 Capital Asset Pricing Model

Efficient Frontier with risk free asset Thank You Questions? Lokanandha Reddy Irala 19 Capital Asset Pricing Model