Download

1 / 32

320 likes | 334 Views

Join us for an informative workshop on pensions for women in business. Learn about different types of pensions, tax relief on personal contributions, and the benefits of company pension schemes, PRSAs, and personal pension plans.

E N D

Women in Business Network “Women & Pensions”Monday 8th May 2006 Mary Hutch Head of Information The Pensions Board

Agenda • The Pensions Board • Why have a pension? • Tax Relief on Personal Contributions • Types of Irish Private Pensions • Company Pension Schemes and Benefits • Personal Retirement Savings Accounts (PRSAs) and Benefits • Personal Pension Plans (RACs) and Benefits • SSIA Incentives • Some Facts • National Pensions Awareness Campaign (NPAC) 2003-2006

The Pensions Board Established by the Pensions Act, 1990 • Main functions are set out in the Act and include • to monitor and supervise the operation of the Act and pension developments generally • Board has 2 statutory roles – regulatory and policy • Promoting pensions development, information and awareness is an associated support function. • Board conducts the National Pensions Awareness Campaign (NPAC) on behalf of Government as recommended in the “Securing Retirement Income” report of the National Pensions Policy Initiative published in 1998

Why have a pension? • The current state social welfare pension is €193.30 per week (or €10,051 per year) • Provision of regular income to replace earnings in retirement, or early retirement due to ill-health • Provision of lump sum benefit income for surviving dependants • Tax Reliefs • Income Tax and PRSI relief on employee contributions • Employer contributions not taxed as BIK (unless paid to PRSA) • Pension schemes do not pay income or capital gains tax on investment returns. • Part of your retirement benefit may be paid as tax-free cash sum

Tax Relief on Personal Contributions The maximum contribution rate as a percentage of total pay/net relevant earnings on which you can receive tax relief is: Highest age at any time during the tax year Limit Under 30 15% 30-39 20% 40-49 25% 50-54 30% 55-59 35% 60 and over 40% Notes: Contributions will also be relieved from the PRSI and the Health Levy, if you pay these charges. For tax purposes these contributions are limited to earnings up to a maximum of €254,000 in any year.

Types of Irish Private Pensions • Company Pension Scheme (88,069 schemes with 726,405 members) (68.9% DB schemes and 31.1% DC schemes) (Fund assets in excess of 70 billion (estimate)) • Personal Retirement Savings Accounts (PRSAs) (68,257 PRSAs with asset value of €451 m - end Dec 05) (76,304 employers had signed up with a PRSA provider ) • Personal Pension Plans and Retirement Annuity Contracts (RACs) (In excess of 200,000 contracts – Irish Insurance Federation) Voluntary regime for supplementary pension provision

Company Pension Schemes • Also known as Occupational Pension Schemes, sponsored by employers on behalf of employees • In private sector, funded arrangement set up under trust so funds held separately from company assets • In public sector usually ‘pay as you go’ unless commercial public sector • Occupational Pension Schemes fall into 2 categories: 1. Defined Benefit 2. Defined Contribution • Operation of schemes is regulated by Pensions Act and monitored by the Pensions Board

Occupational Pension Scheme Benefits • Pension payable on retirement, usually 65, for your lifetime and taxed under PAYE • Once-off tax free cash sum on retirement of up to 1½ final salary • A pension may be payable to your spouse/dependants/children on your death, either before of after pension commences. • A lump sum may be payable on your death either before or after your retirement • A pension and/or lump sum may be payable if you retire in ill-health See PB Information Booklets ‘What are my Pension Options?’ and ‘Women and Pensions’

Personal Retirement Savings Accounts (PRSAs) • For employees, self-employed, homemakers, carers, unemployed or any other category • Contract between individual and PRSA provider – Investment account holding units in investments managed by approved PRSA provider • Two types – PRSA and Standard PRSA • Mandatory employer access • Usual tax reliefs applicable • Transfers to and from other pension arrangements are facilitated as far as possible • Pension Board approves PRSA products and monitors activities of PRSA providers

PRSA Benefits • In general can take retirement benefit anytime from 60-75 • 25% of fund as tax-free lump sum at retirement • Number of options on how to use balance 1. Purchase annuity with life assurance company, or 2. Transfer value of assets to an Approved Retirement Fund (ARF) subject to meeting the qualifying conditions. Withdraw funds as required (taxed as PAYE) , or

PRSA Benefits 3. Retain funds in PRSA and opt to draw income as required (taxed as PAYE). To avail of this option, a minimum of €63,500 must be used to purchase annuity or kept in PRSA until age 75 unless minimum income of €12,700 pa 4. On death before retirement – value of fund available as death benefit payable as lump sum or pension or combination of both 5. On death after retirement benefits payable depend on options chosen at time annuity purchased and if ARF in place.

Personal Pensions and Retirement Annuity Contracts (RACS) • Self-employed or those in non-pensionable employment can take out a Personal Pension Plan aka Retirement Annuity Contract (RAC) • Individual contract between individual and insurance company • Can also effect a life assurance policy at some time to protect dependants • These plans are not covered by Pensions Act but are regulated by Insurance Acts

Personal Pensions/RACs Benefits • Options and benefits on death and on retirement much the same as PRSAs • May not normally retire ‘till age 60 • May retire at any stage in permanent ill-health • See PB Information Booklets ‘What are my pensions options?’ , ‘Women and Pensions’ and ‘PRSAs – a Consumer’s Guide’

SSIAs and Pensions • New SSIA Related Pension Incentive – Finance Act 2006 • Applies to incomes < €50,000 • Tax Credit of €1 for every €3 invested up to a max €2,500 – Invest €7,500 and get €2,500 from State. • Amount transferred from SSIA not subject to 23% exit tax. • Scheme operates from 1 June 2006 • See www.revenue.ie – SSIA Pension Incentive

The Facts • Only 54.2% of men in the Irish workforce • Only 47.5% of women in the Irish workforce • Less than 16% of those working in • the agricultural industries including farming • working seasonal & part-time • working in the catering & tourism industries …have private pensions

Consumer Research and Awareness Audits The key barriers to starting a pension for most people are: • Can’t afford one • house/holiday/car etc are the immediate priority • Too young to start a pension • Too complicated don’t understand pensions

Show Me the Money (Indecon) 1.1 million SSIA account holders € 165 is the average contribution similar to the average PRSA contribution 40% are saving the maximum amount 38% have indicated they would save all or part of their savings 49.8% of accounts will mature in April 2007 Only 9% suggested investing in a pension The Saving Habit is the Key……………….

We are Living Longer More Contract Work More Part Time Working Single Parent Households Smaller Families Separation Divorce Changing World We Live In

Where will your income come from when you retire? The current state social welfare pension is €193.30 per week (or € 10,051 per year) …….will this be enough for you to live on ? 87% of the Pensions Board Consumer Researchsample said that the State old age pension would NOT meet their needs in retirement

Start your pension early • a man retiring at 65 now can expect to live to 81 • a woman retiring at 65 can expect to live to 84 ….that’s nearly 20 years in retirement !

Employers Play your Part Access for all Employees • By law an employer must provide ALL employees with some form of access to a pension, whether they are in full-time, part-time, temporary, contract or casual employment. • All employers regardless of the size of their workforce areobliged to provide access to a Standard PRSA if those employees fall into the category of “excluded employees” (details available on the Board’s website).

A good deal for YOUR Company A good pension scheme has been long recognised as a very valuable asset for both the company and its employees. There is a stronger commitment from employees to participate in pension schemes where the employer makes a contribution. Your company benefits from having: • a reputation and respect as a good employer. • a workforce that feels valued and important • increased loyalty and commitment from staff • an enhanced staff recruitment, reward and retention package

National Pensions Awareness Campaign 2003 - 2006

Highlights from NPAC 2003“Think about tomorrow. Today” • TV Adverts and Radio Adverts • Media print supplements • Posters and Internet Adverts • Shopping Till Receipts and In-Store Plasma Screens • Radio and Press interviews and Community Forums • National Pensions Awareness Week 13 – 19 October 2003 all focused on directing people into action – to either talk to their employer, contact their bank, insurance company, building society or financial advisor to discuss pension options. • Every employer in Ireland (over 173,000) was posted a copy of the Board’s information booklet on “PRSAs and Employers’ Obligations” to help them comply with their obligations under the Pensions Act.

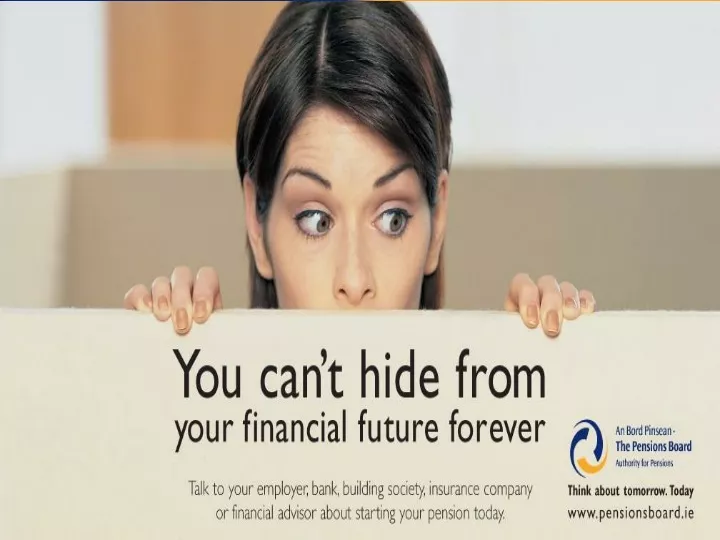

Highlights from NPAC 2004“You can’t hide from your financial future forever” Held National Pensions Awareness Week in September. Integrated TV, Radio, Press and ambient advertising campaign. Launched the “on-line calculator” on our website Handed out 100,000 sample calculators Distributed 50,000 copies of the Women & Pensions booklet

Highlights from NPAC 2005“Action & Responsibility” • Pensions Action Week in May. • Focused on young people and women • Targeted the print, radio and TV shows that young engage with most. • Literature handed to people on the street when they came off public transport and in their cars at traffic junctions. • Sent out a “call to action” message in newspapers, especially regional ones where coverage rates are low. • Used an array of ambient media, including posters on buses, 48 sheet admobiles and on-line banner links to our website.

National Pensions Awareness Campaign 2006 Proposed Strategy & Implementation Plan

National Pensions Awareness Campaign 2006 Background and Objectives Background • Allocation of €1,000,000 is available for NPAC 2006. • The maturity of SSIAs represents an opportunity to encourage greater take-up of pensions and an increase of pension adequacy. • Research shows that awareness about pensions is very high but that action following awareness is low, while adequacy levels among those with pensions are not sufficient. • CSO figures identify specific sectors and age groups with particularly low levels of pension penetration, especially amongst 25 – 39 year olds. • Low levels of pensions awareness and understanding among under 25 year olds NPAC Objectives 2006 • The primary objective of the NPAC 2006 is to push action by those with no pension and to ensure those with pension provision address the adequacy of that provision. • A related objective is to encourage SSIA holders to think about pension planning when their SSIA funds are released.

National Pensions Awareness Campaign 2006 Proposed Strategy • NPAC 2006 will focus on ‘Action and Adequacy’. • Intensified advertising and promotion focus on the key targets (25 – 39 year olds). • Tap into the SSIA windfalls and encourage SSIA holders to invest some of their capital into a pension and keep the savings habit. • Directing consumers to be personally responsible for their future retirement planning as well as promoting employers responsibility. • Guiding consumers to the Pensions Board website particularly the pensions calculator. • Educating young people with the “Pensions Checklist” as the first step to starting a pension. “Starting a new job – ask about your pension” • More intensive in 2006 ‘on the street’ activity at key events relevant to NPAC target groups – Women’s mini marathon, ladies GAA final, Women’s Camogie finals, National Ploughing Championships – promote to young people around music events like the Electric Picnic and Oxygen.

Women & Pensions Diamonds are forever……...... ......but a good pension is a girl’s best friend !