Download

1 / 41

430 likes | 642 Views

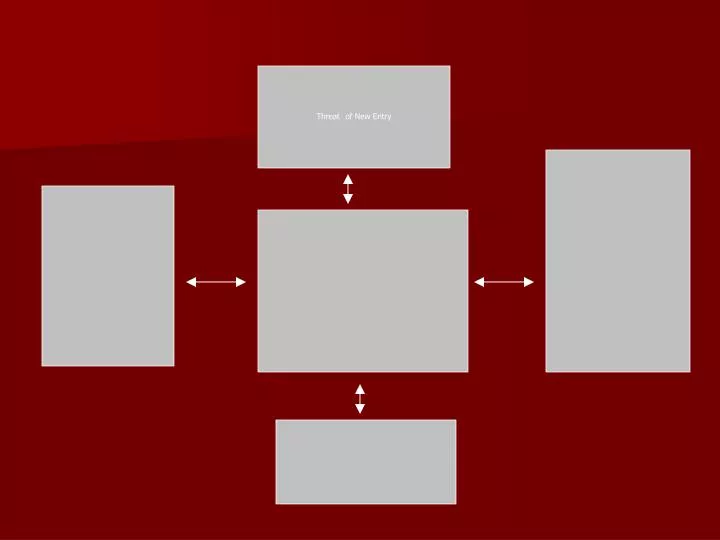

Threat of New Entry. Economies of Scale Proprietary product differences Brand Identity Switching costs. Capital requirements Access to distribution Absolute cost advantages Government Policy Expected retaliation. Threat of New Entry. Economies of Scale.

E N D

Economies of Scale Proprietary product differences Brand Identity Switching costs Capital requirements Access to distribution Absolute cost advantages Government Policy Expected retaliation Threat of New Entry

Economies of Scale • Fortune brands and Masco consolidate resources and sharing plants. Changes the structure of competition. Changes Economies of Scale. • Threat comes from acquisitions of smaller cabinet companies to gain size. • Aristo bought Capital Kitchens • Legacy Cabinets and Sunshine Kitchens became a member of Republic National Cabinet Corp • Aristo is in markets now which they were not before because of Capital Kitchens.

Proprietary Product Differences • Customer Loyalty • May lose sales if a customer is acquired and parent company has loyalty to another cabinet company.

Switching Costs • Customers have costs associated with replacing showroom displays, IT change over, CAD Program, inventory, backlog, and training.

Capital Requirements • Capital requirements are high. • American Woodmark is spending $12 million to build a new plant. • Advertising, R&D costs, and training are high expenses.

Access to Distribution • Huge barrier • Distributors - MCS

Absolute Cost Advantages • Large companies leverage buying. • Ability to outsource • Managing the supply chain • Chinese connections

Government Policy • Restrictions from the EPA

Bargaining Power of Suppliers • Information from Gary Bateman • Differentiation of inputs • Switching costs • Presence of substitute inputs • Supplier concentration • Importance of volume to supplier • Cost relative to total purchases • Impact of inputs on cost or differentiation

Threat of Substitutes • Relative price performance of substitutes • Switching costs • Buyer propensity to substitutes

Buyer Concentration Buyer Volume Buyer Switching Costs Buyer Information Ability to Integrate Backward Substitute Products Price/Total Purchases Product Differences Brand Identity Impact of Quality/Performance Buyer Profits Bargaining Power of Customers

Buyer Concentration/Volume • Higher volume of purchases the better price the buyer gets. E.g. Factors, rebates • Selling to Home Depot and Lowes. • Tougher to raise prices. • Customer demands price decreases and sensitive to price increases. • Builder Consortium (Toll House and K Hov) • Home Centers going out of Business. • Big Builders getting bigger with acquisitions.

Focused Builder Assessment Top 100 Builders - Share of Market 1990 vs. 2005 est. Acquisitions are driving top 100 Builder market share gains Source: Professional Builder Magazine, April 2003

Top 10 Builders Share of Top 100 Source: Builder Magazine, July 2003

Buyer Switching Cost • K Hov push on manufacturers to consume costs of switching. • Switching costs are high, issue who pays • Process and systems, raw materials

Buyer Information • Low information for the end-user. Consumers do not know what to look for in products. • Results of Cherry Audit

Ability to Integrate Backward • Pulte has Divosta in FL. Has reached capacity so Pulte is outsourcing. • John Wieland builds own cabinets. • Pulte and supply chain with China.

Substitute Products • Ready-To-Assemble Cabinets • Ikia • Millspride

Price/Total Purchases • Breakdown of cost of home • Total cost of building a home at $124,276 only 5% of cost is cabinets and countertop.

Product Differences • Demands for a variety of products. Finished, door style, accessories • Turn-key solution • There are process differences

Brand Identity • Lennar-US Home no longer keep brand name separate • Influence of Brand Names on Purchase Decision PPT slide from NAHB Consumer Preference Survey 2003.

Impact of Quality/Performance • Service key • Alliant Survey • Replacement parts lead-time • Operations side

Buyer Profits • List top 10 last 5 years of Profitability, price of homes, stock price • Article from NAHB Housing Economics

Industry growth Fixed Costs/Value added Overcapacity Product differences Brand Identity Switching costs Concentration and balance Informational complexity Diversity of competitors Corporate Stakes Exit Barriers Rivalry Among Existing Competitors

Industry Review Industry Size and Growth 2003 $9.5 Billion 102.0 Million Units Source: Dollars--F.W. Dodge, June 2003 SBI, June 2001

Industry Review Merillat Unit Volume and Opportunity Gap by Industry Segment Source: Units--F.W. Dodge, June 2003 CONTINUED OPPORTUNITY

Channel Review 1992 - 2002 CAGR by Channel Segment ($s) Source: KB&B Industry Report, 1993 - 2003 * - Other includes consumers, architects, and interior designers

Fixed Costs/Value Added • Information from Doug Benette

Overcapacity • Competitors expansion and acquisitions • American Woodmark • Bertch • Ultracraft • Cabinetry by Karman • Spreadsheet with additions and deletions of competitors 200-2002

Product Differences • List of Competitors and product offerings

Brand Identity • Hanley wood study

Concentration and Balance • Spreadsheet with Top 40 • Consolidation is not going as fast as builders

Informational Complexity • Increasing need to be more solutions oriented. • Understanding of new products coming out

Diversity of Competitors • List of Competitors and list other ventures the company has ex. Kitchen sink, hinges, faucets, countertops.

Corporate Stakes • Investments – publicly held companies have a lot higher stakes. • Reputation

Exit Barriers • Low