Download

1 / 10

130 likes | 583 Views

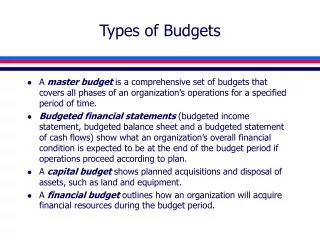

Types of Budgets. Budgeting Basics. Master Budget. Overall financial and operating plan Prepared annually of quarterly A number of sub budgets tied together A Summary. Operating and Financial Budgets. Deals with costs of merchandise or services produced

E N D

Types of Budgets Budgeting Basics

Master Budget • Overall financial and operating plan • Prepared annually of quarterly • A number of sub budgets tied together • A Summary

Operating and Financial Budgets • Deals with costs of merchandise or services produced • Examines expected assets, liabilities, and stockholder’s equity of business • Gives picture of company’s financial health

Cash Budget • For cash planning and control • Expected cash inflow and outflow for designated period • Consists of 4 major sections • Receipts: beginning cash balance, cash collections from customers, and other receipts • Disbursement: comprised of all cash payments • Cash surplus or deficit: difference between cash receipts and cash payments • Financing: detailed account of the borrowings and repayments expected during period

Fixed Budget • Is budgeted figures at the expected capacity level • Used when companies are stable • Lacks flexibility to adjust to unpredictable changes

Expense Budgets • Most commonly used • Very versatile • Four steps in preparing expense budgets • Determine relevant range over which activity is expected • Analyze costs that will be incurred over relevant range to determine cost behavior patterns (variable, fixed, mixed) • Separate costs by behavior • Using formula for variable portion of costs, prepare budget showing what costs will be incurred at various points throughout relevant range

Capital Expenditure Budget • A listing of long term projects to be undertaken • Typically three to ten years • Classified by objective • Expansion/enhancement • Cost reduction/replacement • Development of new product • Health and safety expenditures

Strategic Budgets • Integrates strategic planning and budgeting control • Effective under conditions of uncertainty and instability

Target Budget • Major expenditures are matched to company goals • Strict justification for large dollar and special project requests

Continuous Budget • Revised on regular basis • Also known as rolling budget • Company will extend budget for another month or quarter as new data on current period ends