Download

1 / 47

• 470 likes • 568 Views

15.3 Bearing and Eliminating Risk. Why do people buy insurance? Why do people buy extended warranties? Why are extended warranties so expensive? What is a reasonable extended warranty? These questions are answered by: Actuarially Fair Insurance Risk Premium. 15.3 Actuarially Fair Insurance.

E N D

15.3 Bearing and Eliminating Risk • Why do people buy insurance? • Why do people buy extended warranties? • Why are extended warranties so expensive? • What is a reasonable extended warranty? These questions are answered by: • Actuarially Fair Insurance • Risk Premium

15.3 Actuarially Fair Insurance Actuarially Fair Insurance -insurance where the premium is equal to the expected value of the payout

Actuarially Fair Insurance Example Assume that you could buy fire insurance. You have a $100,000 job, and an 80% chance to lose $75,000 (house fire). Your utility is U=√I. Risky Income: p($100,000 )=0.2, p($25,000)=0.8 1) Calculate Actuarially Fair Insurance Premium

Actuarially Fair Insurance Example If you didn’t get insurance, your utility would be: U=√I Risky Income: p($100,000 )=0.2, p($25,000)=0.8 2) Utility without Insurance

Actuarially Fair Insurance Example With fair insurance, your utility would be: U=√I Risky Income: p($100,000 )=0.2, p($25,000)=0.8 Insurance: $60,000 2) Utility with Insurance

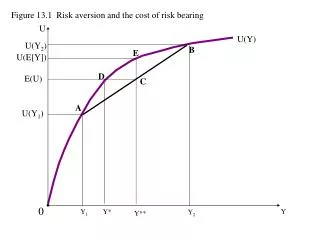

Actuarially Fair Insurance Utility AFI gives you the expected income of a risky situation U Uinsure • Unoinsure D 0 25K $40K=E(I) 100K Income Chapter Fifteen

15.3 Is Insurance ever Fair? Actual insurance premiums are rarely actuarially fair, partially due to a firm making profit, but also due to other factors: • administration • moral hazard • adverse selection (which will be covered later) What is the maximum amount someone will pay above actuarially fair premiums?

15.3 Risk Premium Risk Premium -Maximum amount of money that a risk- averse person will pay to avoid taking a risk -Maximum amount a person will pay in premiums above actuarially fair premiums Note: Even risk loving people consider themselves risk averse for large purchases.

Risk Premium Utility Risk premium = horizontal distance ED U E • • E(U) D 0 Is E(I) Income Chapter Fifteen

Calculating Risk Premium • Calculate E(I) of risky choice. • Calculate E(U) of risky choice • Calculate sure income Is of E(U) • Risk Premium = E(I)- Is • Conclude

Risk Premium Example • U=√I Risky Income: p($100,000 )=0.2, p($25,000)=0.8 • 1) Calculate E(I) of risky choice • 2) Calculate E(U) of risky choice

Risk Premium Example • U=√I Risky Income: p($100,000 )=0.2, p($25,000)=0.8 • E(I) = $40,000 E(U) = 189.7 • 3) Calculate Is of E(U) • 4) Calculate Risk Premium

Risk Premium Example This person would spend a maximum of $4,014 above actuarially fair insurance premiums to avoid the risk in his job. This person would accept a job paying at least $35,986 instead of taking the risky job. • This person is willing to buy additional insurance against his risky job

Risk Premium Utility Risk premium = horizontal distance $4,014 U E • • E(U) 4,014 D 0 25K IS E(I) 100K Income Chapter Fifteen

15.3 Administration and Profit Providing insurance isn’t free, there are administration costs: • Paying employees • Overhead • Legal Costs • Etc Insurance firms also desire profits. Many extended warranties carry 40%-80% profit margins.

15.3 Loading Fees Loading Fee = Actual Premium – Actuarially Fair Premium -Average loading ratio (actual premium/fair premium) for private US insurance companies is 1.2 (Phelps 2003) -(typical laptop service plan is $200 for 3 years, working out to a Loading Ratio of 4.0 – 10% failure rate in year 2 and 3 for $500 laptop) -keep in mind administration costs

15.3 Asymmetric Information Part of the additional costs of insurance, as well as items such as deductibles and mandatory insurance, arises from: ASYMMETRIC INFORMATION – when one party has information not available to another party • Typically, the person being insured has information the insurance company doesn’t: • Hidden actions – Moral Hazard • Hidden information – Adverse Selection

15.3 Moral Hazard • If people have insurance, their actions may change in two ways: • They are riskier (take laptop to beach, eat unhealthy – health insurance) • They over consume insurance since it’s free (Send laptop to be fixed, ask for unneeded tests based on “House” – health insurance) This second effect can be shown through supply and demand:

Moral Hazard P Without insurance, repairs cost P0 and Q0 repairs are made (where S=D). This causes repair expenditures of area A. S=MC (constant) P0 A B P1 Q Q0 Q1 D=MB With insurance, repairs cost P1 and Q1 are made (where new S=D). This causes repair expenditures of Area A +B (expenditures increase).

Moral Hazard P This overcomsumption causes deadweight loss where MC>MB: S=MC (constant) P0 DWL P1 Q Q0 Q1 D=MB The insurers are forced to cover waste, therefore insurance premiums increase.

15.3 Fighting Moral Hazard • Moral Hazard can be decreased by: A) Including “reckless” situations that invalidate warranty ie: Casio Calculator Warranty: “The customer shall NOT have any claim under this warranty for repair or adjustment expenses if:” • The problem is caused by improper, rough or careless treatment; • The problem is caused by a fire or other natural calamity;

15.3 Fighting Moral Hazard 3) The problem is caused by improper repair or adjustment made by anyone other than a CASIO Service Center; 4) The problem is caused by battery leakage, bending of the unit, broken display or key; 5) The battery is damaged or worn… 7) The proof of purchase is not presented when requesting service -although it can be hard to prove that a customer has been “reckless”: “Of course I didn’t drop my ipad!”

15.3 Fighting Moral Hazard B) Introducing a cost to claim the warranty/insurance. ie: • Deductible • Shipping Costs • Cost of time • Long repair time • Hard-to-get-to repair location

15.3 Adverse Selection • Insurance can break down due to Adverse Selection – an increase in insurance premium increases the average risk of the insured • Assume there are 3 laptop purchasers: • Bill has a laptop failure rate of 10% (he’s a computer technician) • Charles has a laptop failure rate of 20% (he’s average) • Denis has a laptop failure rate of 30% (he clicks on all the “you won” pop-ups)

15.3 Adverse Selection • Recall that actuarially fair insurance just charges enough to over expected repairs • AFI = ($500xP(failure)): • Bill: $50 • Charles $100 • Denis $150 • If you charge: • $50 – Charles and Denis cause a loss • $100 – Bill doesn’t want insurance and Denis causes a loss • $150 – Charles and Bill don’t want insurance

15.3 Adverse Selection • If insurance is optional, those with higher risk would buy • This leads to more expensive claims • This leads to higher premiums • This leads to more people not buying insurance • The end result would be UNDERPROVISION of insurance

15.3 Adverse Selection • 5 Issues can keep Adverse Selection from killing a private insurance market: • Risk Aversion • Group Insurance • Insurance Choice • Risk Categories/Risk Profiling • Mandatory Insurance

i) Risk Aversion • Because people are risk averse, they are willing to pay a RISK PREMIUM above the actuarially fair premium. • This may keep more people in the market ii) Group Insurance • Larger companies can offer group insurance plans that automatically cover everyone (high and low risk) • This doesn’t help small firms or the self-employed

iii) Insurance Choice • If different levels of insurance at different costs are offered, people will self-sort themselves into different categories: • Denis will pay $150+ for the full insurance (ie: Product Replacement Plan) • Charles will pay $100+ for partial insurance (ie: Product Service Plan) • Bill will pay $50+ for limited insurance (ie: manufacturer warranty included in price)

iv) Risk Categories • Adverse selection occurs due to asymmetric info – inability to know a person’s risk • HOWEVER, a company can charge premiums based on OBSERVABLE characteristics statistically linked to UNOBSERVABLE risk • ie: Male 20-year olds pay more for auto insurance because they are STATISTICALLY more likely to have an accident than Female 20-year Olds

iv) Risk Profiling? • The Supreme Court of Canada ruled this does not violate the Canadian Charter of Rights and Freedoms because there is statistical evidence that 20-year-old males do have higher loss probabilities • Some ask how long until we are charged based on: • Ethnicity • Religion • Sexual Orientation (marital status already applies) • If there is statistical evidence?

v) Manditory Insurance • Public Health Insurance, Car insurance, etc is MANDATORY, and therefore Adverse selection is avoided since the low risk individuals can’t drop out PRO’s: • Mid and High-risk individuals are covered at a reasonable rate ($100 in our example) Con’s: • Low risk individuals would rather not be covered at a high rate (for them)

15.3 Diversification – Insurance Alternative • Risk can also be managed through: Diversification – Reducing risk by allocating resources to a variety of activities whose outcomes are not closely related ie: • Stock Market – buying a variety of stocks • Sales – selling a variety of products • Insurance – buying a variety of good without the warranty.

15.3 Law of Large Numbers • Diversification works because of: Law of Large Numbers – as the number of samples increases, the average of these samples is likely to reach the mean of the whole population (investopedia) ie: Stock has 50% fail rate Full fail chance of 1 stock = 50% Full fail chance of 2 stocks* = 25% Full fail chance of 8 stocks* = 0.39%*stocks must be unrelated -extreme outcomes reduce, expected outcome increases

15.3 Diversification – Extended Warranties • Assume: You spend $5000 on electronics over 10 years, with an average FULL failure rate of 10% • No Extended Warranty: You spend $500 on repairs and replacement E(repair)=cost * f(cost)E(repair)=$5000 * 0.10 = $500 • Extended Warranty: You spend $1000 on extended warranties (assume 50% profit margin)

15.4 Risk and Game Trees • Probabilities can be combined with Game trees from chapter 14 • A player who MAKES decision is replaced by an outcome that is chosen by chance • These game trees or decision trees can be FOLDED BACK in a method similar to backward induction to reduce the tree to the simple trees seen in chapter 14:

15.4 Risk and Game Trees Example 1 • Circles represent CHANCE NODES (choices made by chance), while squares represent DECISION NODES (choices made by players).

15.4 Risk and Game Trees Example 1 • Chance Nodes are FOLDED BACK by replacing them with the expected payoff: E(B)= Σ$f($)=0.5($50)+0.5($10)=$30

15.4 Risk and Game Trees Example 1 • Now new best responses lead to an overall Equilibrium

15.4 Risk and Game Trees Example 2 • Sometimes the process takes multiple steps

15.4 Risk and Game Trees Example 2 1) Backward induction of E and F 2) Expected return of B and C

15.4 Risk and Game Trees Example 2 3) Expected Return of D

15.4 Risk and Game Trees Example 2 4) Final Backward Induction

15.4 Value of Information • This previous example highlights the VALUE OF INFORMATION • The firm expected return increases by $5 (million) if it is able to do a free test • The firm will pay up to $5 million for the test Value of Perfect Information – increase in a decision maker’s expected payoff when they can conduct a costless test to determine the outcome of a risky event VPI = E($)with test- E($)without test

15.4 Value of Information Examples • People pay money for information in a variety of ways: • New house inspections • Car inspections • Consumer Report subscriptions • Online dating sites • Etc.

Chapter 15 Conclusions • P(a) = Prob(a) = probability that event a will occur • E($) = Σ$f($) • E(U) = ΣUf(U) • People can be risk averse, risk neutral, or risk loving depending upon their preferences between certain and uncertain incomes. • Actuarially Fair Insurance=E(loss) • Most people are willing to pay a RISK PREMIUM above Actuarially Fair Insurance

Chapter 15 Conclusions 7) Insurance Premiums are increased by Asymmetric Information (Moral Hazard and Adverse Selection), which can be reduced but never eliminated. 8) Diversification is an alternative to insurance 9) Game trees including risky outcomes can be “Folded Back” using expected values and analyzed normally 10) Information is valuable 11) Unless you can’t sleep at night without one, say “no” to the extended warranty.