Download

1 / 64

640 likes | 655 Views

Review. Principle of separation. Present discounted value the real investment. (equivalence). Decide whether to undertake it (optimization). Select the appropriate financial investment or disinvestment (optimization). Representation. switch and win or stay and lose. guess wrong.

E N D

Principle of separation • Present discounted value the real investment. (equivalence). • Decide whether to undertake it (optimization). • Select the appropriate financial investment or disinvestment (optimization).

Representation switch and win or stay and lose guess wrong Nature’s move, plus the contestant’s guess. pr = 2/3 pr = 1/3 guess right switch and lose or stay and win

No arbitrage condition: • Price of bond = price of zero-coupon bond + price of stripped coupon. • Otherwise, a money machine, one way or the other. • Riskless increase in wealth

Pie theory • The bond is the whole pie. • The strip is one piece, the zero is the other. • Together, you get the whole pie. • No arbitrage pricing requires that the values of the pieces add up to the value of the whole pie.

No arbitrage principle • Market prices must admit no profitable, risk-free arbitrage. • No money pumps. • Otherwise, acquisitive investors would exploit the arbitrage indefinitely.

Definition of a call option • A call option is the right but not the obligation to buy 100 shares of the stock at a stated exercise price on or before a stated expiration date. • The price of the option is not the exercise price.

Example • A share of IBM sells for 74. • The call has an exercise price of 76. • The value of the call seems to be zero. • In fact, it is positive and in one example equal to 2.

S = 80, call = 4 Pr. = .5 S = 70, call = 0 Pr. = .5 t = 1 t = 0 S = 74 Value of call = .5 x 4 = 2

Definition of a put option • A call option is the right but not the obligation to sell 100 shares of the stock at a stated exercise price on or before a stated expiration date. • The price of the option is not the exercise price.

Put call parity at expiration • Equivalence at expiration s + p = X + c • Values at time t in caps: S + P = Xe-r(T-t) + C • Write S - Xe-r(T-t) = C - P

Puts and calls before expiration • S, P, and C are the market values at time t before expiration T. • Xe-r(T-t) is the market value at time t of the exercise money to be paid at T • Traders tend to ignore r(T-t) because it is small relative to the bid-ask spreads.

No arbitrage pricing impliesput call parity • If the relation does not hold, a risk-free arbitrage is available. • If S - Xe-r(T-t) > C – P, then • Sell the stock short, and also sell the put. Use the proceeds to buy the call and a bond paying X at expiration. The position is riskless. It nets the arbitrageur a positive sum. That violates no arbitrage pricing. • Similarly if inequality is in the other direction.

“Real” options • The option to abandon is a put option. • Deciding to delay or not, the firm exercises or not its call on the project.

Review item • What is the interest rate?

Do write: • The interest rate is the premium for current delivery of money. • P0 is the price of current money in current money, namely 1. • P1 is the price of time-one money in terms of current money, something <1. • P

Review item • When a firm creates value through a financial transaction, who gets the increase?

Answer • Old equity means the shareholders at the time the decision is made. • Old equity gets the gains. • Why? Old equity has no competitors. Everyone else is competitive and must accept a market return.

Example • Coupons sell for 450 • Principal sells for 500 • The bond MUST sell for 950. • Otherwise, an arbitrage opportunity exists. • For instance, if the bond sells for 920… • Buy the bond, sell the stripped components. Profit 30 per bond, indefinitely. • Similarly, if the bond sells for 980 …

Incremental cash flows • Cash flows that occur because of undertaking the project • Not sunk barges … oops, I mean costs. • Opportunity cost • Side effects • Working capital

Net working capital • = cash + inventories + receivables - payables • a cost at the start of the project (in dollars of time 0,1,2 …) • a revenue at the end in dollars of time T-2, T-1, T.

Internal rate of return • Definition: IRR is the discount rate that makes NPV = 0 That is, IRR is the r such that

IRR’s at r=1 and r=2. NPV 100% 200% r

Invest Decision Tree for Stewart Pharmaceutical The firm has two decisions to make: Invest To test or not to test. To invest or not to invest. NPV = $3.4 B Success Test Do not invest NPV = $0 Failure Do not test NPV = –$91.46 m

Success: PV = $575 Sit on rig; stare at empty hole: PV = $0. Drill Failure Sell the rig; salvage value = $250 Do not drill The Option to Abandon: Example Traditional NPV analysis overlooks the option to abandon. - $300 The firm has two decisions to make: drill or not, abandon or stay.

Beta measures risk • How much risk is added depends on the relation of sAM and s2M • Define beta

Covariance • It measures the tendency of two assets to move together. • Variance is a special case -- the two assets are the same. • Variance = expectation of the square of the deviation of one asset. • Covariance = expectation of the product of the deviations of two assets.

Rate of return expected by the market Security market line E[Rj] E[RM] Rf 1 b

Example of beta and NPV • Wingmar Inc. has a beta of 2. • The Market risk premium is 8.5% • The risk-free rate is 4%. • Wingmar has a project with cash flows -100, 60, 80. • The project is typical of Wingmar’s core business. • Should the project be undertaken?

Uses of Cash Flow (100%) Sources of Cash Flow (100%) Capital spending 98% Internal cash flow (retained earnings plus depreciation) 97% Internal cash flow Financial deficit Net working capital plus other uses 2% Long-term debt and equity 3% External cash flow The Long-Term Financial Deficit (2002)

Event Studies: Dividend Omissions Efficient market response to “bad news” S.H. Szewczyk, G.P. Tsetsekos, and Z. Santout “Do Dividend Omissions Signal Future Earnings or Past Earnings?” Journal of Investing (Spring 1997)

All informationrelevant to a stock publicly availableinformation past prices Relationship among Three Different Information Sets

EPS and ROE under Proposed Capital Structure Shares Outstanding = 240 Bust Normal Boom EBIT $1,000 $2,000 $3,000 Interest 640 640 640 Net income $360 $1,360 $2,360 EPS $1.50 $5.67 $9.83 ROA 5% 10% 15% ROE 3% 11% 20%

Cost of capital: r(%) rS . r0 rWACC rB Debt-to-equityratio (B/S) MM Proposition II no tax

Cost of capital: r(%) . rS . r0 . . rWACC rB Debt-to-equityratio (B/S) MM II and WACC

Debt channel Equity channel Corporate taxes TC Personal taxes TS TB 1-TB (1-TC)(1-TS) Channels $ of operating cash flows

tax cut increased equity Operating C.F.’s of the whole economy Value as debt Value as equity ...

Summary: APV, FTE, and WACC APV WACC FTE Initial Investment All All Equity Portion Cash Flows UCF UCF LCF Discount Rates r0 rWACC rS PV of financing Yes No No Which is best? • Use WACC and FTE when the debt ratio is constant • Use APV when the level of debt is known.

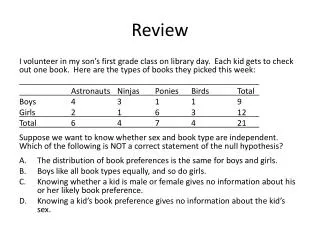

Review item • Two assets have the same expected return. • Each has a standard deviation of 2%. • The correlation coefficient is .5. • What is the standard deviation of an equally weighted portfolio?

Review item • A firm has a project with positive NPV. • The project costs 100M to start. • The firm has only 50M. • What should it do?

Answer • Raise the money in the capital market. • It can because NPV is market valuation.

Capital asset pricing model T-bill rate is known. Market premium is known, approximately 8.5%. Estimate beta as in the project

. T . S 0.8 Security Market Line T is undervalued. Its price rises Expected returnon security (%) Security market line (SML) . . . . Rm M Rf S is overvalued. Its price falls Beta ofsecurity 1

EPS and ROE under Proposed Capital Structure Shares Outstanding = 240 Recession Expected Expansion EBIT $1,000 $2,000 $3,000 Interest 640 640 640 Net income $360 $1,360 $2,360 EPS $1.50 $5.67 $9.83 ROA 5% 10% 15% ROE 3% 11% 20%

Proposition II of M-M • rB is the interest rate • rs is the return on (levered) equity r0 is the return on unlevered equity • B is value of debt • SL is value of levered equity • rs = r0 + (B / SL) (r0 - rB)

rWACC MM Proposition II no tax Cost of capital: r(%) rS . r0 rB Debt-to-equityratio (B/S)

MM II (with taxes) • Corporate taxes, not personal • rB = interest rate • rS = return on equity • r0 = return on unlevered equity • B = value of debt • SL = value of levered equity • Previously, without taxes rS = r0 + (B/SL)(r0 - rB)

Effect of tax shield • Increase of equity risk is partly offset by the tax shield • rS = r0 + (1-TC)(r0 - rB)(B/SL) • Leverage raises the required return less because of the tax shield.