Download

1 / 35

2.19k likes | 4.99k Views

The Accounting Equation. Chapter 1.1. What is Accounting?. Accounting- planning, recording, analyzing, and interpreting financial information Accounting System- planned process for providing financial information useful to management

E N D

The Accounting Equation Chapter 1.1

What is Accounting? • Accounting- planning, recording, analyzing, and interpreting financial information • Accounting System- planned process for providing financial information useful to management • Accounting records- organized summaries of a business’s financial activities

Who Uses Accounting Info? • Owners, managers, accounting personnel use accounting to understand what is happening within accounts • Suppliers use accounting to interpret financial activities represented by financial statements • Financial Statements- reports that summarize financial condition and operations of a company • Government- uses accounting records to assess taxes

What If Accounting Goes Wrong? • Inaccurate accounting records often lead to business failure or bankruptcy. • Failure to understand accounting can lead to poor decision making.

What is a Business Entity? • BUSINESS ENTITY is the accounting concept applied when a business’s financial information is recorded and reported separately from the owner’s personal financial information.

Proprietorships • Proprietorship (sole proprietorship)- business owned by one person • Can include service businesses- provide services for a fee • Can include retail businesses- provide goods/products

Sole Proprietorship • Advantages • Ease of formation • Total control by owner • Profits are not shared • Disadvantages • Limited resources • Unlimited liability • Limited expertise • Limited life • Obligations to follow both the laws of the federal government and the state in which it is formed

Discussion • Why do you think more businesses organize as proprietorships than any other form of business organization? • What kinds of people do you think would be most successful as owners of a proprietorship?

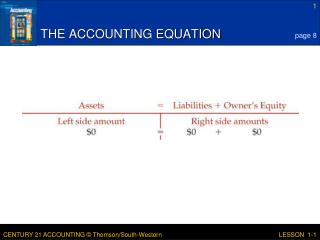

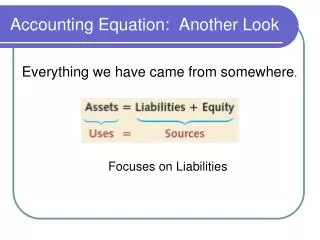

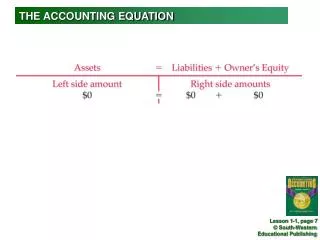

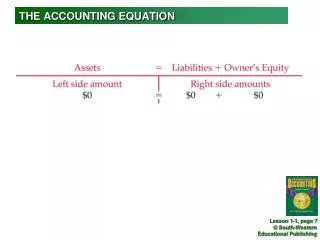

The Accounting Equation ASSETS = LIABILITIES + OWNER’S EQUITY • Shows the relationship between assets, liabilities, and owner’s equity • MUST BALANCE!

THE ACCOUNTING EQUATION page 8 LESSON 1-1

The Accounting Equation • Asset- anything of value that is owned; have value because they can be used to acquire other assets or operate a business • Equities (financial rights to assets): • Liability- any amount owed by a business to another entity (supplier, bank, etc) • Owner’s Equity- amount remaining of assets after all liabilities have been paid

problems Practice: Complete On Your Own 1-1 on page 9 and turn it in.

How Business Activities Change the Accounting Equation Chapter 1.2

Business Transactions • Transaction- a business activity that changes assets, liabilities, or owner’s equity • Every transaction changes the amounts in the accounting equation

What is a Unit of Measurement? • The accounting concept of UNIT OF MEASUREMENT is applied when business transactions are stated in numbers with common values (common units) • This concept is followed so financial reports are clearly stated and understood and can be compared

Recording Activity • A record summarizing all the information pertaining to a single item in the accounting equation is called an ACCOUNT • Account Title-name given to the account (simple info, but very important) • Account Balance- amount in the account (again, simple, but very important)

Capital Account • Capital- account summarizing the owner’s equity of a company

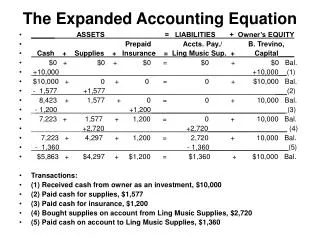

Transactions and the accounting equation • One single item impacts BOTH sides of the accounting equation • However, the accounting equation is still BALANCED

Transaction 1August 1. Received cash from owner as an investment, $5,000.00. RECEIVING CASH page 10 LESSON 1-2

Transaction 2August 3. Paid cash for supplies, $275.00. PAYING CASH page 11 Transaction 3August 4. Paid cash for insurance, $1,200.00. LESSON 1-2

Transaction 4 August 7. Bought supplies on account from Supply Depot, $500.00. TRANSACTIONS ON ACCOUNT page 12 Transaction 5 August 11. Paid cash on account to Supply Depot, $300.00. LESSON 1-2

Practice • Work Together 1-2, page 13 • On Your Own 1-2, page 13

How Transactions Change Owner’s equity Chapter 1.3

Received Cash from Sales • Revenue- an increase in owner’s equity due to operations of business • When cash is received, the total amount of both assets and owner’s equity is increased • Transactions for sales of goods or services result in an INCREASE in owner’s equity

Sold Services on Account • Sale on Account- sale for which cash will received at a later date • aka “Charge Sale” • Regardless of when payment is actually made, revenue should be recorded at the time of sale

REALIZATION OF REVENUE • Accounting Concept: Regardless of when payment is actually made, revenue should be recorded at the time of sale

Transaction 6 August 12. Received cash from sales, $295.00. REVENUE TRANSACTIONS page 14 Transaction 7 August 12. Sold services on account to Oakdale School, $350.00. LESSON 1-3

Expense Transactions • Expense- decrease in owner’s equity resulting from the operation of business • Transactions to pay for goods or services needed to pay for operations of business

Paid Cash for expenses • When paying cash for expenses: • Cash is decreased • Owner’s equity is decreased • Expenses could be: • Rent, supplies, advertising, equipment rental or repair, charitable contributions, misc.

Transaction 8 August 12. Paid cash for rent, $300.00. EXPENSE TRANSACTIONS page 15 Transaction 9 August 12. Paid cash for telephone bill, $40.00. LESSON 1-3

Other Transactions • Receive cash on account: • Increase Cash, decrease Accounts Receivable • Paid cash to owner for personal use: • Withdrawal- assets taken out for owner’s personal use • Decrease asset (Cash), decrease Owner’s Equity

Transaction 10 August 12. Received cash on account from Oakdale School, $200.00. OTHER CASH TRANSACTIONS page 16 Transaction 11 August 12. Paid cash to owner for personal use, $125.00. LESSON 1-3

Practice • Work together 1-3 on page 17 • On Your Own 1-3 on page 17

GAAP • Generally Accepted Accounting Principles designed to guide all financial business practices • Provides conformity and financial information is consistent across companies