Download

1 / 10

100 likes | 116 Views

Join Roger Bennett, University Tax Manager, and Anna Gralia-Szucs, Tax Assistant, for a training session on Income/Sales within the UK, VAT codes, and applicable exemptions. Learn about different types of supplies, place of supply rules, and get advice from our tax experts. Don't miss this informative session!

E N D

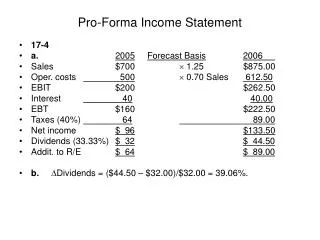

University VAT Training Income/Sales 4 July 2019 Roger Bennett - University Tax Manager Anna Gralia-Szucs - Tax Assistant

Income/Sales within the UK Exempt Supplies (VAT Code X) • Education • Tuition fees/supplies closely related to a supply of education • course materials/field trips • catering to students • student accommodation • Academic Conferences • content and admin must be supplied by the University • includes accommodation and catering • excludes alcohol, laundry and additional nights • a form should be completed to support any invoice if this exemption is used • Examination Services • Lectures and course fees • Student photocopying income • Bench fees from students

Land • Normally includes room hire (where there is no catering) • Sport and Sport Competitions • Gym membership fees • Other Income • Private patients’ income

Outside the Scope of VAT (VAT Code OS) • Pure donations with ‘no strings’ attached • Funding Council grants • Research income – where there is no supply to the funder (no transfer of Intellectual Property) • Library fines and penalties • Reimbursement of travel costs and other academic costs from eligible bodies (where there is no supply)

Standard Rate Supplies (VAT Code S) • Consultancy income • Catering supplies – other than students, within catered outlets • Hire of staff • Research services – sponsor receives a supply (usually measured in terms of a transfer of IP)

Zero and Reduced Rated Supplies (VAT Code Z / R) • Zero Rated • Hard copy books • Sales of qualifying equipment to other charities • Cold takeaway food • Reduced Rate (5%) • Domestic fuel and power • Recharges of utility costs to staff/other for self-catering accommodation • Sanitary products

Sales of Goods/Services outside the UK – within the EU (VAT Code SC) • Provided the customer is based within the EU and is in business (VAT registration is an indicator of ‘in business’), no UK VAT needs to be added • Sales invoices must include the wording ‘this is an intra-community supply and VAT has to be accounted for where the customer is based, under the reverse charge procedure’ • If the sale is a business to a customer (B to C) transaction, then UK VAT has to be added

Sales of Goods/Services outside the UK – rest of the world (VAT Code OS) • Provided the University can demonstrate that the customer is based outside of the EU, no UK VAT needs to be added to the sales invoice and the income is treated as ‘outside the scope’ of VAT

Place of Supply Rules for VAT • The basic place of supply rule for VAT is based on where the customer belongs • Exceptions • Land-related services • Hire of means of transport • Admission to an event • Education • Sporting/artistic and similar activities • Restaurant and catering services • Passenger and freight transport • Use and enjoyment • Telecommunications services • Radio and television broadcasting services

Need Assistance or Advice • Taxation Section – Northcote House • vat@exeter.ac.uk • Roger Bennett (University Tax Manager) ext 5438 r.w.bennett@exeter.ac.uk • Liz Shillingford ext 3098 E.E.Shillingford@exeter.ac.uk • Anna Gralia-Szucs ext 3132 A.Gralia-Szucs@exeter.ac.uk • University Tax Website • http://www.exeter.ac.uk/finance/operations/vat/ • HMRC website helpful for detailed VAT rules - use search or look under ‘charities’ or ‘education’ section • http://www.hmrc.gov.uk/ • Taxation Section – Northcote House • vat@exeter.ac.uk • Roger Bennett (University Tax Manager) ext 5438 r.w.bennett@exeter.ac.uk • Other Finance Services Contacts ext 3076, 5009 or 5058 • University Tax Website • http://www.exeter.ac.uk/finance/operations/vat/ • HMRC website helpful for detailed VAT rules - use search or look under ‘charities’ or ‘education’ section • http://www.hmrc.gov.uk/