Download

1 / 31

310 likes | 330 Views

Your monthly payments. No arbitrage pricing. Key concepts. Real investment Financial investment. Interest rate defined. Premium for current delivery. Basic principle. Firms maximize value Owners maximize utility Separately. Justification.

E N D

Your monthly payments No arbitrage pricing.

Key concepts • Real investment • Financial investment

Interest rate defined • Premium for current delivery

Basic principle • Firms maximize value • Owners maximize utility • Separately

Justification • Real investment with positive NPV shifts consumption opportunities outward. • Financial investment satisfies the owner’s time preferences.

A typical bond Note: Always start with the time line.

Definitions • Coupon -- the amount paid periodically • Coupon rate -- the coupon times annual payments divided by 1000

Two parts of a bond • Principal paid at maturity. • A repeated constant flow -- an annuity

Strips • U.S. Treasury bonds • Stripped coupon is an annuity • Stripped principal is a payment of 1000 at maturity and nothing until then. • Stripped principal is also called a pure discount bond, a zero-coupon bond, or a zero, for short.

No arbitrage condition: • Price of bond = price of zero-coupon bond + price of stripped coupon. • Otherwise, a money machine, one way or the other. • Riskless increase in wealth

Pie theory • The bond is the whole pie. • The strip is one piece, the zero is the other. • Together, you get the whole pie. • No arbitrage pricing requires that the values of the pieces add up to the value of the whole pie.

Yogi Berra on finance • Cut my pizza in four slices, please. I’m not hungry enough for six.

Why use interest rates? • In addition to prices? • Answer: Coherence

Example: discount bonds • A zero pays 1000 at maturity. • Price (value) is the PV of that 1000 cash flow, using the market rate specific to the asset and maturity.

Example continued • Ten-year maturity: price is 426.30576 • Five-year maturity: price is 652.92095 • Similar or different? • They have the SAME discount rate (interest rate) r = .089 (i.e. 8.9%)

Calculations • 652.92095 = 1000 / (1+.089)5 • Note: ^ is spreadsheet notation for raising to a power • 426.30576 = 1000 / (1+.089)10

More realistically • For the ten-year discount bond, the price is 422.41081 (not 426.30576). • The ten-year rate is (1000/422.41081)1/10 - 1 = .09. • The 1/10 power is the tenth root. • It solves the equation 422.41081 = 1000/(1+r)10

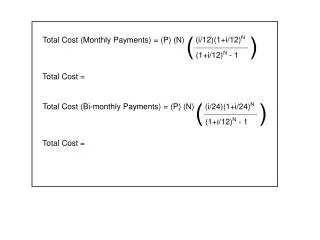

Annuity • Interest rate per period, r. • Size of cash flows, C. • Maturity T. • If T=infinity, it’s called a perpetuity.

Value of a perpetuity is C*(1/r) • In spreadsheet notation, * is the sign for multiplication. • Present Value of Perpetuity Factor, PVPF(r) = 1/r • It assumes that C = 1. • For any other C, multiply PVPF(r) by C.

Value of an annuity • C (1/r)[1-1/(1+r)T] • Present value of annuity factor • PVAF(r,T) = (1/r)[1-1/(1+r)T] • or ATr

Explanation • Annuity = • difference in perpetuities. • One starts at time 1, • the other starts at time T + 1. • Value = difference in values (no arbitrage).

Values • Value of the perpetuity starting at 1 is = 1/r … • in time zero dollars • Value of the perpetuity starting at T + 1 is = 1/r … • in time T dollars, • or (1/r)[1/(1+r)T] in time zero dollars. • Difference is PVAF(r,T)= (1/r)[1-1/(1+r)T]

Compounding • 12% is not 12% … ? • … when it is compounded.

Example: which is better? • Wells Fargo: 8.3% compounded daily • World Savings: 8.65% uncompounded

Solution • Compare the equivalent annual rates • World Savings: EAR = .0865 • Wells Fargo: (1+.083/365)365 -1 = .0865314

Exam (sub) question • The interest rate is 6%, compounded monthly. • You set aside $100 at the end of each month for 10 years. • How much money do you have at the end?

Answer Interest per period is .5% or .005. Present value is PVAF(120,.005)*100 = 9007.3451 Future value is 9007.3451*(1.005)120 = 16387.934