Download

1 / 27

290 likes | 423 Views

Conditions for bubble formation. Michael Joffe Imperial College London. The importance of bubbles. increasing study of bubbles in recent years – not least because of the perception that the financial crash of 2007-2009 involved one or more of them

E N D

Conditions for bubble formation Michael Joffe Imperial College London

The importance of bubbles • increasing study of bubbles in recent years – not least because of the perception that the financial crash of 2007-2009 involved one or more of them • several bubbles in recent decades; some observers believe that their frequency and/or severity may be increasing • they tend to occur in stock markets (e.g. dot-com), or in real estate; in the latter case a major role is played by the financial sector (Shiller “Irrational exuberance”, 2nd edition)

Bubbles: symmetric or asymmetric? • typical definition: “trade in high volume at prices that are considerably at variance from intrinsic value” [King RR et al. 1993] • a question of how prices are set: how do the seller and the potential buyer come to form a compatible perception of “the going price”? • the metaphor of a “bubble” suggests something that grows steadily and then bursts suddenly • the first is symmetric – can be up or down – but the second is asymmetric: only up; which is correct? – an empirical question • in addition, one needs to ask, is there always an “intrinsic” value?

Aim of the paper • to present a model of bubble formation that predicts asymmetry • my reading of the literature is that the focus has predominantly been on symmetric behaviour, in line with the definition rather than the metaphor • the assumed context: • the market is of a type where the price is not set in direct relation to costs, as is the case e.g. for an established product => a need for information on what is “the going price” • market participants may perceive a trend in prices, upwards or downwards, and extrapolate from that to predict that the trend will continue into the future: “trend extrapolation”

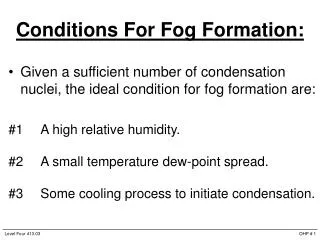

The model I starting from a standard market equilibrium model: D(P) = a – bP (1) S(P) = c + dP (2) where P is the price; D(P) and S(P) respectively represent the willingness to buy and to sell the asset now at the existing price; assuming for simplicity that the demand and the supply curves are both linear and given by the parameters a,b,c,d, with b,d > 0

The standard market equilibrium model S price D P1 Q1 quantity

The model I starting from a standard market equilibrium model: D(P) = a – bP (1) S(P) = c + dP (2) where P is the price; D(P) and S(P) respectively represent the willingness to buy and to sell the asset now at the existing price; assuming for simplicity that the demand and the supply curves are both linear and given by the parameters a,b,c,d, with b,d > 0

The model II trend extrapolation condition: perception of a price trend expected to continue into the future this brings about a price increment ΔP “now” to take into account the cost or benefit of waiting: the price modified by trend extrapolation is (P + ΔP); ΔP is negative with a falling trend ΔP can be represented by: ΔP = θP (3) where θ is the proportional expected future price increment

The model III for simplicity the perceived trend P’ is regarded as linear θ is given by θ = f(P’) (4) with f(.) an increasing function: θ<0 for P’<0, and θ>0 for P’>0 for a representation of how θ may relate to P’ in terms of ζ, “investor sentiment” or tendency to buy, see Caginalp and Ermentrout 1990

The model IV The original equations now become: D(P) = a – bP + mθP (1’) S(P) = c + dP – nθP (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation

The model IV The original equations now become: D(P) = a – bP + mθP (1’) S(P) = c + dP – nθP (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation m,n > 0 because if the trend is rising (θ>0), then mθP>0 and nθP>0, and vice versa for a falling trend (θ<0)

The model IV The original equations now become: D(P) = a – bP + mθP (1’) S(P) = c + dP – nθP (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation

The model IV The original equations now become: D(P) = a – bP + mθP = a – P(b – mθ) (1’) S(P) = c + dP – nθP = c + P(d – nθ) (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation

The model IV The original equations now become: D(P) = a – bP + mθP = a – P(b – mθ) (1’) S(P) = c + dP – nθP = c + P(d – nθ) (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation Compare (1’) and (2’) with (1) and (2): D(P) = a – bP (1) S(P) = c + dP (2)

The model IV The original equations now become: D(P) = a – bP + mθP = a – P(b – mθ) (1’) S(P) = c + dP – nθP = c + P(d – nθ) (2’) where m,n are parameters (>0) that determine the extent to which the price is affected by trend extrapolation Compare (1’) and (2’) with (1) and (2): D(P) = a – bP = a – P(b) (1) S(P) = c + dP = c + P(d) (2)

The model V bubble occurrence depends on reversal of the sign of the coefficient of P we now have two conditions for this: if mθ > b, a rise in P will lead to a rise in D(P) (5) if nθ > d, a rise in P will lead to a fall in S(P) (6) under these conditions, therefore, instead of the usual decreasing function in P for D(P) and increasing function for S(P), as represented by equations (1) and (2), the situation is reversed (5) and (6) can be written as θ>b/m and θ>d/n

The model VI recall that b,d,m,n > 0 therefore θ>b/m => θ>0 and θ>d/n => θ>0 the property of reversing the overall direction of equations (1) and (2) only occurs when θ>0, and thus also P’>0 this model therefore predicts asymmetry

The model VII D(P) = a – bP + mθP (1’) S(P) = c + dP – nθP (2’) in the case where θ<0, the terms mθP and nθP would have the same signs as bP and dP respectively they would merely accentuate the normal decreasing and increasing functions represented respectively by equations (1) and (2)

The model VIII To summarize: • the model predicts that if prices start at or near their intrinsic level, a self-fulfilling and thus self-perpetuating tendency will tend to occur in markets with an upward – but not a downward – price trend • the conditions specified by the model bring about a bubble equilibrium: a rising price reinforces the perception that prices are destined to rise, and in turn this perpetuates the rising trend – for as long as the trend extrapolation perception lasts • bubble equilibria are inherently unstable

The model IX • the bursting of a bubble is not directly covered by the model – the only prediction is that the price deviation cannot continue indefinitely; not the timing and subsequent time course • depends on functional form, and other factors • the return towards the intrinsic value then proceeds according to the standard equations (1) and (2) • not necessarily sudden “bursting” • where there is no clear intrinsic value, the equivalent role would be played by a realisation that prices are no longer affordable

Situational rationality I • a rational calculation in the context of imperfect information • can be seen as a form of bounded rationality, but limited calculating ability is not a feature here • the extrapolated trend is external to each market participant => they have to join in, even with misgivings • it is difficult to distinguish between “behavioral theories built on investor irrationality and rational structural uncertainty theories built on incomplete information about the structure of the economic environment” (Brav & Heaton)

Situational rationality II • Caginalp & Ermentrout: “emotional”; also “group-think”, “optimism” or “panic” • e.g. Akerlof & Shiller: “Animal spirits”

Situational rationality II • Caginalp & Ermentrout: “emotional”; also “group-think”, “optimism” or “panic” • e.g. Akerlof & Shiller: “Animal spirits”

Situational rationality II • Caginalp & Ermentrout: “emotional”; also “group-think”, “optimism” or “panic” • e.g. Akerlof & Shiller: “Animal spirits” • these emotions may occur – but are they causal? – hard to answer • are they invariably present? consider someone buying a property to live in, when property is seen as likely to increase in price – it’s a calculation • emotion is likely to be added to this, with a small group of operators + face-to-face contact: e.g. financial market traders; ? the real estate context

Conclusion • the model predicts asymmetry: the process of progressive deviation from intrinsic value (or from affordability) will occur in a rising but not a falling market, and actual prices will be higher than intrinsic value (or affordability) in such circumstances; until the bubble bursts • there are four conditions for this to occur: • price setting is not based on established cost, so that additional information is required • “the going price” is based on trend extrapolation • (θ > b/m) and (θ > d/n) • a fortiori, P’ > 0, i.e. bubbles form when prices are rising