Download

1 / 11

110 likes | 166 Views

Learn about the key responsibilities and activities of the IFTA Audit Committee in 2015, including workshop updates, ballot reviews, and proposed audit requirements.

E N D

IFTA AUDIT COMMITTEE 2015 Annual IFTA Business Meeting Audit Committee Report Presented by David Nicholson (OK), Chair

Audit Committee Beth Duda AZ* Bob Gattinella RI Diana Kay FL Jimmy Tompkins AL Joel Foreman NE* Kristie Zanis NH Lynden Landholm KS* Maxime Dubuc QC Stacey Hammock WY Jeff Hood IN Ex-Officio Helen Varcoe MT Vice-Chair David Nicholson OK Chair Board Liaisons Joy Prenger MO IFTA Board Steve Nutter VA IFTA Board IFTA, Inc. Advisors Debbie Meise IFTA, Inc. Tammy Trinker IFTA, Inc.

AC CharterAuthority And Purpose The AC is established by the IFTA Articles of Agreement pursuant to Article R1810.200.020. The purpose of the AC is to review and maintain the IFTA Audit Manual, and to complete other responsibilities assigned to it by the International Fuel Tax Association, Inc. (IFTA, Inc.) Board of Trustees (Board). R1350 REVIEW/REVISION OF AUDIT REQUIREMENTS .100 The Audit Committee shall review the audit requirements of this Agreement at least once every three years.

AC Charter Committee Responsibilities A. advising the IFTA membership regarding audit matters; B. planning and conducting an annual audit workshop; C. reviewing and commenting on ballot proposals, D. reviewing and preparing responses for consensus board interpretation drafts referred to it by the Board,

AC Charter Committee Responsibilities E. developing ballot proposals and Board interpretation requests, F. maintaining a committee member rotation chart, G. recruiting members and maintaining a list of potential committee members, H. making recommendations to the Board to fill committee vacancies; and I. maintaining the IFTA Best Practices Audit Guide.

AC At Work 2015 IFTA/IRP Workshop Held February 2015 San Antonio 206 attendees from jurisdictions and industry Continued work on Ballot #3 2014 Ballot #3 is currently out for a 4th comment period.

AC At Work Currently working on the 2016 Audit Workshop Recently filled 3 vacancies Working on updating the Best Practices Guide Responded to several inquiries from the membership 2015 Ballots are being reviewed in relation to audit

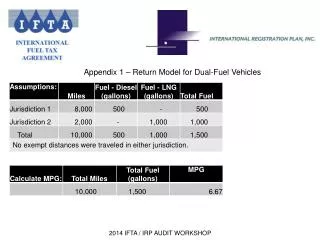

Ballot #4 2014 Currently reviewing Ballot #4 2014 – What constitutes an audit for count? This ballot failed – Why? Current language indicates an audit of a license year. The proposed language would have been 4 consecutive quarters in lieu of licensing year.

Ballot #4 2014 At last years ABM, there was discussion of being able to include “short period audits”. Current language requires all four (4) quarters in the license year. The AC would like your input – Any 4 consecutive quarters 4 consecutive quarters tied to the IRP (registration year) Short period audits - An audit of a company with less than 4 quarters of operations - When a licensee closes an account prior to four (4) consecutive quarters, an audit will qualify as long as all auditable quarters are included.

Changes to Ballot 3-2014 After the first 3 Comment Periods Requirements moved back to the Procedures Manual Removed the term “Evidence” Removed the Proposed Sampling Language Inadequate Records Assessment – The audited or reported MPG/KPL can adjusted. The Ballot has been vetted by the ASSC. With the changes identified, the proposed language does not affect the defensibility or three core provisions of the Agreement.

Comments/Questions? Thank You!