Download

1 / 13

130 likes | 157 Views

Explore the impact of biases on judgments in accounting, ranging from self-serving biases to attachment biases influencing auditors' decisions. Discover how familiarity, discounting, and escalation play a role in biased judgments and their implications.

E N D

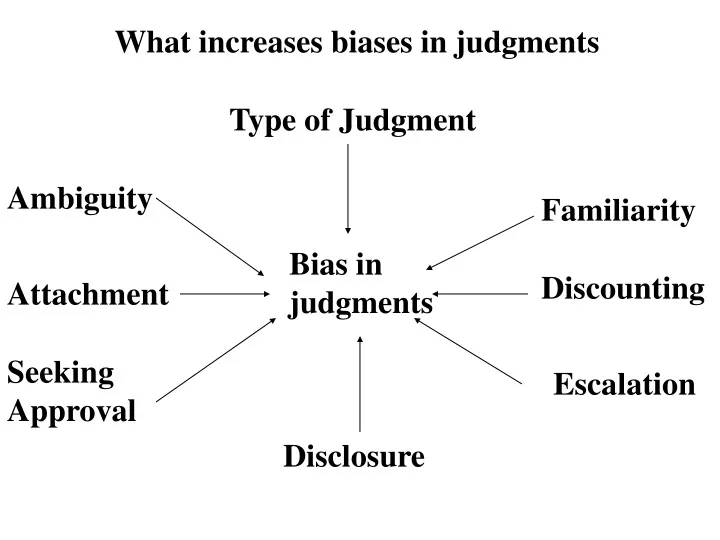

What increases biases in judgments Type of Judgment Ambiguity Familiarity Bias in judgments Discounting Attachment Seeking Approval Escalation Disclosure

Ambiguity in accounting • Study of approx 50 tax preparers shows 83%-976% difference in how much a family owes in yearly taxes • Ambiguity in Income, deductibles, depreciation schedule • Declaring items as revenue vs. expenses (early vs. later) has implications on how stockholders react • Firms hire based on how auditors interpret accounting problems

Self-serving Bias Attachment Students role playing as plaintiffs (in an accident) predicted that they would receive larger awards from the judge than did those role-playing the defendants Bias in Judgment

Types of training that does/does not decrease self-serving bias Learning about self-serving biases Writing essays arguing for other side Reading case first before being assigned a role as plaintiff/ defendant 0 0 - Bias in judgments

Seeking approval • You are even more biased toward yourself when someone else is biased toward your opinion when you come to that opinion yourself • Implications for overly biased judgments • E.g., when auditors make judgments by themselves first vs. merely “endorsing” judgments that clients already made (they are even more biased toward their self-serving biases)

Familiarity, discounting, escalation • On-going relationships Familiarity • Decide between negatively affecting clients (who are company executives) vs. company investors (who are not clients) • Discounting • Favour immediate consequences vs. delayed uncertain consequences (movie) • E.g., damage to relationship, loss of contract, unemployment • Escalation • Sum of small judgments large biases (corruption)-- movie

Auditor Attachment affects Bias in Judgment • Study of buyer, seller, buyer auditor and seller auditor • Seller valued firm more than buyer • Auditors were more biased toward client interests • Sellers auditors valued firm more than buyer auditor • Reward for accuracy for auditors did not eliminate the bias they already had

Auditor Attachment affects Bias in Judgment • Auditors who were hired by the company were more likely to conclude that the company complied with the GAAP rules rather than those auditors who were hired by the company’s business collaborator • Experience of auditor did not decrease the bias

How evidence supports the link Type of Judgment Those who generated own audits first and then judged company reports were less biased than those who judged company’s reports first and then generated their own audits Bias in Judgment

Advisors vs. estimators of how much $$ in jar • Estimator got paid for accurate judgments • Advisor got paid for how high estimator’s estimate was (i.e., advisor had a incentive to make higher judgments) Disclosure of conflict of interest Bias in Judgment

Disclosure of advisor’s motive to estimator did not lead estimators to discount advisor’s advice and make lower judgments so advisors made more than estimators Disclosure of conflict of interest Bias in Judgment

Advisors who were given incentives to mislead estimators to make high judgments and whose motives were disclosed to estimators were more biased than those whose motives were not disclosed. • Because advisors seemed to adjust for estimator’s discounting and so made even higher judgments Disclosure of conflict of interest Bias in Judgment

Legal reform in accounting should remove the incentive for being attached and should take into account the negative effects of disclosure to the organization Legal Reform + ? Increase Disclosure Reduce Attachment Reduce Bias in Judgment