Download

1 / 8

80 likes | 98 Views

Comprehensive analysis on product listing, sales, ranging strategy, merchandising, and category management in the retail market. Insights for suppliers to enhance in-store performance.

E N D

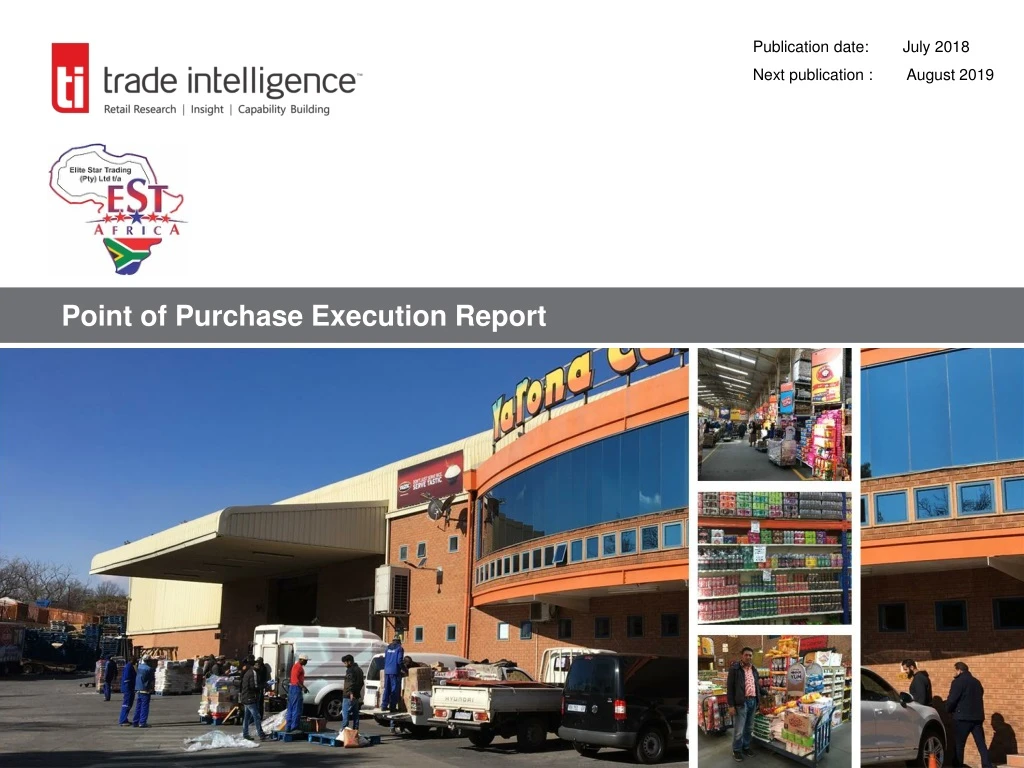

Publication date: July 2018 Next publication : August 2019 Point of Purchase Execution Report

Point of Purchase Execution • Product Listing and Buying • Product listing occurs at both Head Office and store level – national brands tend to be listed at Head Office, while local / regional brands are listed by each member • Listed suppliers : • Head Office: • Approximately 90% of member’s stock is purchased through the Group Head Office, with all promotional stock required to be purchased through Head Office • At Group level, the buying department is structured into Foods (headed by Mohammed Varachia) and Building/Hardware (Rob Suttle) • Member Level • Store-level procurement conducted over and above that at a national level - approximately 10% of member’s stock • Extent of member-level buying dependent on member volume/value (i.e. what the store is able to offer the supplier) • Members hold own accounts with suppliers, the Group does not host centralised supplier accounts • For constructive negotiation at a store level, it is advantageous for suppliers to have a strong understanding of regional/local brands and price points as well as be observant of POP drivers in-store | Elite Star Trading | Point of Purchase Execution

Point of Purchase Execution • Sales • Overall structure (please note that these are averages across the member base): • On average, between 20%-40% of sales-out occur on the shop floor; 80% of sales often take place through an inbound telesales department (note that this varies by member, some members have as much as 90% of sales occurring on the shop floor) • The majority of members incorporate a telephonic ordering department (Telesales) • Every telephonic price confirmed by dedicated, senior person to which telesales staff report – immediate decision-making on price • Telephonic orders pre-picked by the store and collected personally by traders • Horizontal trading is prevalent in the independent market (wholesaler to wholesaler) • Sales Spread • 60% of store turnover achieved within the first 7 days of the month (on average) • Hence need for large warehousing capacity and high % of buffer stock – no supplier able to gear itself adequately • Sharing of sales out data with the Group is at the member’s discretion, rendering data sharing variable | Elite Star Trading | Point of Purchase Execution

Point of Purchase Execution • Ranging Strategy • Regional/store based – brand loyalty of the South African consumer particularly evident on a geographic / regionallevel • Regional/local brand strengths have an impact on forward share and ranging decision-making • Category ranging decisions based on the ability of any one store to trade in meaningful quantities – competitive pricing hinges on bulk buying • Members manage their own range decision-making • Supplier opportunity: • To better understand brand regionality and implement more specific/localised brand strategies in conjunction with wholesalers/retailers | Elite Star Trading | Point of Purchase Execution

Point of Purchase Execution • Ranging Strategy cont. • Elite Star member stores (particularly wholesale/hybrid outlets) offer a wide (‘’Big Box’) range of categories in-store • The depth of range within each category is generally narrow, but this is dependent on the member store and shopper profile specifics, e.g. a wider distribution area requires greater brand depth, as regionality will differ • The majority of members are strongly focused on commodities • Whilst fresh fruit & veg does play a role in within some stores, for most members it is not a priority • Within the retail component, service departments are playing a substantial role, with wider ranges available across several food categories | Elite Star Trading | Point of Purchase Execution

Point of Purchase Execution • Merchandising • The majority of in-store merchandising is conducted by internal member staff. However, over the past year there has been a shift towards outside merchandising, with an increasing number of dedicated supplier merchandisers operating within larger members • Products merchandised in cases, shrinks and units on a single shelf • Pallet-based merchandising, based on broad principals of forward share, applies across the majority of members. Smaller pack sizes are merchandised at eye level, while larger packaging and shrinks are merchandised above • Sales volumes determine forward share – allows for powerful displays for individual brands • Catering sized packs also available, predominantly merchandised at floor level • Single pack size merchandising less predominant due to high shrinkage levels, however with the shift towards hybrid trading, single units are finding their space on shelf • High value items often merchandised behind the counter | Elite Star Trading | Point of Purchase Execution

Point of Purchase Execution • Category Management • Category Management approach • Category management is conducted through supplier agreement and is driven by regional brand strengths, as well as on-shelf availability • EST members tend not to utilise formal category management principles frequently in-store, although there is movement towards supplier-driven space planning initiatives with certain suppliers • Recent Category Shifts • Within commodities (maize, flour, sugar and rice) growth evident in : • Private label • Secondary and tertiary (economy) brands • Overall decline in flour sales, coupled with a shift to cheaper brands • Growth in smaller pack sizes across the range (e.g. 250g and 500g soap powder, 225g tinned foods) • Driven by economic restraints on the end consumer • Hardware continues to show growth driven by EST strategic objective of establishing a firm foothold and growing share in this category • Hamper sales a primary offering in North West and Northern Cape, particularly for commodities (both in wholesaler and informal trader) • Growth in decanting: • Spaza owners decanting a wide range of product – from Sunlight Liquid to Cremora, to eggs; “sell in scoops” • Portion packs - supplier opportunity to achieve correct, market-related pricing | Elite Star Trading | Point of Purchase Execution

tel +27 [0] 31 303 2803 fax +27 [0] 31 303 4560 info@tradeintelligence.co.za Kate Shirley | Retail Analyst New Channels Maryla Masojada | Lead Analyst Disclaimer These materials and the information contained herein are collated by TI* referencing a wide range of public domain data sources, face-to-face interviews, retailer presentations and financial reports, and are intended to provide general information about the South African consumer goods trading environment and selected retailers, and are not intended as an exhaustive treatment of such subjects. Whilst every effort has been made to ensure that the information published in this work is accurate, your use of these and the information contained herein is at your own risk. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your business, and TI makes no express or implied representations or warranties regarding the accuracy of the information herein. TI will not be liable for any special, indirect, incidental, consequential, or punitive damages or any other damages whatsoever, whether in an action of contract, statute, tort (including, without limitation, negligence), or otherwise, relating to the use of these materials and the information contained herein. TI expressly disclaims all implied warranties, including, without limitation, warranties of merchantability, title, fitness for a particular purpose, non-infringement, compatibility, security, and accuracy. * TI refers to The Retail Workshop (Pty) Ltd trading as Trade Intelligence Disclaimer These materials and the information contained herein are collated by TI* referencing a wide range of public domain data sources, face-to-face interviews, retailer presentations and financial reports, and are intended to provide general information about the South African consumer goods trading environment and selected retailers, and are not intended as an exhaustive treatment of such subjects. Whilst every effort has been made to ensure that the information published in this work is accurate, your use of these and the information contained herein is at your own risk. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your business, and TI makes no express or implied representations or warranties regarding the accuracy of the information herein. TI will not be liable for any special, indirect, incidental, consequential, or punitive damages or any other damages whatsoever, whether in an action of contract, statute, tort (including, without limitation, negligence), or otherwise, relating to the use of these materials and the information contained herein. TI expressly disclaims all implied warranties, including, without limitation, warranties of merchantability, title, fitness for a particular purpose, non-infringement, compatibility, security, and accuracy. * TI refers to The Retail Workshop (Pty) Ltd trading as Trade Intelligence www.tradeintelligence.co.za