Download

1 / 37

370 likes | 626 Views

Merger & Acquisition in U.S. Taewon Yang California State University at San Bernardino. 1.Definition. Merger/Acquisition: combination of two firms or more than two firms. Recent merger waves resulted from deregulations, technology and relevant consolidations. Example 1.

E N D

Merger & Acquisition in U.S. Taewon Yang California State University at San Bernardino

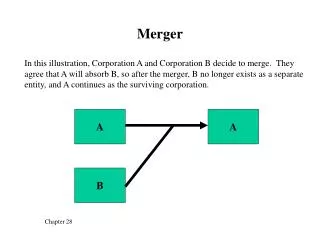

1.Definition • Merger/Acquisition: combination of two firms or more than two firms. • Recent merger waves resulted from deregulations, technology and relevant consolidations.

Example 1 • 2/11/2003. Johnson & Johnson (NYSE: JNJ) Agrees to Pay $ 2.4 Billion ($45 per share) for Scios Inc. (Nasdaq: SCIO), a California pharmaceutical company known for Natrecor, a heart-failure drug. • Christine Poon, worldwide chairwoman of J&J's pharmaceuticals group, said "This transaction is a merger of strength." "It's all about accelerating growth in our pharmaceutical businesses." In addition to the new drugs and technology provided by Scios, another asset of the deal is the experience of the management team for the company.

2) 2/12/2003. Moody's Investors Service affirmed the long and short term debt ratings of Johnson & Johnson with a stable rating outlook, following the merger attempt news. 3) 4/3/2003. Johnson & Johnson and Scios Inc.announced that the U.S. Federal Trade Commission has granted early termination of the waiting period under Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended. 4) 4/28/2003. Scios Inc said its shareholders have approved the 2.4 bln usd takeover offer from Johnson & Johnson.

2. Motives • News commonly quoted improved profitability through the economy of scale/scope and synergy from proposed M&As and diversifications. (e.g.) • Banks: to increase market shares in wealthy or economically growing areas, to have assets (e.g. deposits) in targets, or to provide new services. • High Tech: to obtain advanced or supporting technology or to get into new markets. • Utility: to increase market shares in new areas or to obtain natural resource (e.g. petroleum or gas storage) in targets. • Health Cares: to increase market shares (hospitals) in new areas, to obtain advanced medical technologies, or to provide other services. • Airlines: to obtain the lines (new markets), or to improve sales through vertical mergers.

3. Merger procedure 1) Pre-merger contact with one potential bidder or more: not public, due diligence and Intent of merger agreement. 2) Merger agreement: public announcement of merger terms (e.g. offer price or payment method) and due diligence. 3) Approvals of regulatory bodies (e.g. FTC, DOJ or local regulatory committees). 4) Approvals of target and bidder shareholders.

4. Merger/Takeover types 1) Takeover Procedure: • Mergers and Tender offers 2) Attitude of target/bidder: Friendly mergers and hostile takeovers. 3) Payment Methods -Financing: • Stock mergers, cash mergers and stock/cash mergers. • Stock swap mergers and collar mergers.

4) Terms of a Collar merger Source: “Merger Deal Structure and Investment Strategies” by Ben Branch and Taewon Yang, Journal of Alternative Investments, 2006. • Fixed payment collar: consider the Provident Financial Group (NASDAQ: PFGI) offer to acquire Fidelity Financial of Ohio (NASDAQ: FFOH). In 1999, FFOH shareholders were to receive $21.00 worth of Provident common stock if Provident’s 10-day average daily closing price ending on the date of the last regulatory approval is between $40.00 and $44.50. If the average closing price was less than $40.00, FFOH shareholders would receive a fixed exchange ratio of 0.525. If the average closing price was more than $44.50, FFOH shareholder would receive 0.4719 shares of Provident common stock for each FFOH share. Actually, the average price during the pricing period ended on 17th of November in 1999 was $42.51875. At merger consummation, each outstanding common share of FFOH was converted into 0.4939 shares of Provident common stock. Thus one share of FFOH was worthy of $21.00 ($42.51875 × 0.4939 = $21.00)

Fixed Exchange Collar: consider the 1999 merger attempt between Medco Research (NYSE: MRE) and King Pharmaceutical (NASDAQ: KING). The terms of the agreement set the exchange ratio at 0.6818 shares of King Pharmaceutical common stock for each share of Medco common stock, if the average closing price of King common stock during the twenty (20) consecutive trading days ending on the third day preceding Medco's shareholder’s meeting was between $33.00 and $49.87 per share. If the average closing price of King Pharmaceutical common stock was above $49.87 per share, King would pay $34.00 per share (using its own shares to make the payment) for Medco common stock. If the average closing price of King Pharmaceutical common stock was below $33.00 per share, King Pharmaceutical would provide a purchase price of $22.50 per share of Medco common stock, using its own shares for the payment. King Pharmaceutical could elect not to proceed with the transaction if the average closing price of King’s common stock fell below $30.00 per share. As of the pricing date ended on the 22nd of February in 2000, the average price of King Pharmaceutical was $50.31563. At merger consummation, each outstanding common share of Medco Research was converted into 0.6757 shares of King’s common stock. Thus one share of Medco Research was exchanged for King Pharmaceutical stock worth approximately $34.00 ($50.31563 × 0.6757 = $33.99).

5. Valuing the Target Firm Sources: (1) “Intermediate Financial Management,” Ch. 26. by Brigham and Daves, 8eth. 1) Market Multiple Analysis: To apply Industry average ratios to the targets • (e.g.) Industry average PE * Expected EPS of the target

2) Corporate Valuation Model • Free cash flow = (Net operating profit after tax +depreciation) – new gross investment in operating capitals. Here Net operating profit after tax = EBIT*(1-t). Gross investment = net investment + depreciation. Non-operating asset: marketable securities and investment on others. TV is a terminal value. WACC is a weighted average cost of capitals

3) Discounted cash flow (equity residual model) • Net cash flow to equity holders: NI + depreciation – retention reduced for growth • TV: Terminal value • r: Cost of equity

4) Adjusted present value (APV) • V operation = V unlevered + V tax shield • (here, until t= N, target’s capital structure is supposed to change due to the merger. After t=N, the target’s capital structure is stable. Unlevered is an unlevered cost of equity, TS is tax shield.)

6. Regulations: SEC (securities and exchange commissions) filings in mergers. Source: “Takeover, Restructuring and Corporate Governance” by Weston, Mitchell and Mulherin,4th edition. 1) Filings are required under Securities Act of 1939 and Securities Exchange Act of 1934. • 8-K: to report any material events or changes in companies. Disseminating information. • 425: to provide information regarding communications in connection with mergers. Disseminating information. • S-4: to be used in the registration of securities associated with stock payments in mergers. • 14A: definitive merger proxy statement. • 15-12B: termination of registration of securities and suspension of the filing of periodic reports.

2) Federal Securities Laws: full disclosure of relevant information to achieve fairness in the market. • Security Act of 1933: Regulating the sale of securities. Legal liabilities for any mis-statements or omissions of material information. • Securities Exchange Act of 1934 established SEC to supervise and regulate securities transactions in the market. SEC could stop transaction and request information from firms. • Public Utility Holding Company Act of 1935: to stop abuse of the financing and operation of gas and electric utility firms. • Trust Indenture Act of 1939: To set forth responsibilities of indenture (debt contract) trustee (commercial banks) and requirements that should be included for the protection of the credit holders. Debt amount > $5 million • Investment Company Act of 1940: To regulate the firms involving in security trading and investments. • Investment Advisers Act of 1950: registration and regulation of investment advisers. • Security Investor Protection Act of 1970 established Security Investor Protection Corporation that supervises liquidation of bankrupt securities firms and arrange the payments

Securities Act Amendments of 1975: Recommend the abolition of fixed minimum brokerage commissions. • In 1978, the SEC began to streamline the securities registration process. • Rule 415 in 1982: self registration. Large corporations can register debts and equity that they will sell in 2 years. They can pick up times of selling. • Private Securities Litigation Reform Act (PSLRA) in 1995: To place restrictions on filing of securities fraud class action suits – frivolous claims. • Sarbanes-Oxley Act of 2002: To enforce the auditor’s independence, to strengthen the responsibility of corporations, greater financial disclosure, to separate the interest of analysts from the corporations and to impose the stringent penalties for corporate and financial fraud.

3) Tender offer regulations – Williams Act of 1968. • Goal: to protect target shareholders from swift and secret takeover attempts. • Section 13(d): any person who had acquired 10% or more of stocks of public firms must file a Schedule 13(d) with SEC within 10 days of crossing the 10%. It was amended to 5% in 1970. It was not applied to persons who purchased less than 2% of the stock within the previous 12 months. • Section 14: It is only applied to a public tender offer. Any group (making solicitations or recommendations to target groups) resulting in obtaining more than 5% should file the schedule 14(d) and 14(d)-(1) (Tender Offer Statement). It reveals intents and plans for the target as well as any relationship. 14(d) (4)-(7) regulate terms of a tender offer including the length of time the offer must be left open (20 trading days) and the right of target shareholders to withdraw their tendering. 14(e) prohibits misrepresentation; nondisclosure; any fraudulent actions.

Inside trading: Rule 10B-5 and 14e-3 prohibits trading in nonpublic information in connection with tender offers. Section 16(a) requires any person owning more than 10% of stocks report any transaction to SEC on a monthly basis. Section 16(b) allows any person or firm to suit against inside traders to get the profit back. Sarbanes-Oxley Act amended Section 16(a) requires insiders to report the change of ownership in two days. • Inside Trading Sanctions Act of 1984 provides for triple damages in insider trading case. • Racketeer Influenced and Corrupt Organizations Act of 1970 provides for seizure of assets and triple damages.

4) Regulation of takeover activity by the state. • States are not permitted to pass laws that impose restrictions on interstate commerce. • Indiana Act in1987: when an acquiring entity or bidder obtains shares that would cause its voting power to reach specified threshold levels, the bidder does not obtain the voting rights from those shares. The transfer of voting right should get approvals of a majority of shareholders, not bidder and inside managers. • New York – New Jersey Act provides for 5-year moratorium preventing hostile takeover attempts to newly acquired target. • Delaware Law prevents hostile takeover attempts to newly acquired target for 3 years unless there are approvals of the board of target and 2/3 votes.

5) Antitrust policy • Department of Justice (DOJ) and Federal Trade Commission (FTC) handle the antitrust policy. They could challenge and stop merger attempts, basing on following antitrust laws. 5-1) Sherman Act of 1890 • Section 1 prohibits mergers that would increase monopoly or undue market control. (e.g. Staple and Office Depot in 1997) • Section 2 is directed against firms that already had dominant power in the markets in the view of the government. (e.g. Microsoft – 10 year litigations. Agreed on restrictions on how it develops and licenses software) 5-2) Clayton Act of 1914 created FTC • Section 5 empowered FTC to prevent companies from doing harmful business. • Section 7 and amendment empowered FTC to block stock purchase and asset purchase. FTC also can block a merger attempt that it perceive the tendency of increasing concentration in the market.

5-3) Hart-Scott-Rodino Act of 1976 empowered FTC and DOJ to investigate antitrust issues and to approve a merger attempt before the merger take place. • Under Title 1, DOJ has the power to civil investigate demands. If DOJ suspects antitrust violation, it can request internal files for review. • Title 2 is a pre-merger notification provision. • - If an acquiring firm has sales or assets of $100 million and a target firm has sales or assets of $15 million, merger information should be submitted for review. • - 30 days waiting period (15 days for tender offer) for agency review. An agency may request a 20-days extension (10 days for a tender offer).

Under Title 3, state attorney generals can initiate triple-damage suits relevant to anti-trust violations. 6) Antitrust Guidelines and other market characteristics • Herfindahl-Hirschman Index (HHI): Sum of the squares of market shares.

Whether entry is easy or not • Whether collusion is easy and very profitable. 7) Regulated industry • Railroads – Surface Transportation Board (STB) • Banking – Comptroller of the Currency, FED and Federal Deposit Insurance Corporation (FDIC). • Telecommunications – Federal Communication Commission (FCC).

Example 2 4/11/2003. After its friendly takeover attempt was rejected, Axcan Pharma (Nasdaq: AXCA) launched an unsolicited $203 million tender offer ($8.75 cash per share) for Salix Pharmaceuticals (Nasdaq: SLXP). • Salix adopted a poison pill and recommended shareholders to reject the unsolicited tender offer due to an inadequate offer price. • Axcan did a lawsuit against the target to drop the poison pill and suggested new board members to replace the existing board of directors.

5/2/2003. Axcan Pharma Inc. today announced the expiration of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, with respect to Axcan's tender offer for all outstanding shares of Salix Pharmaceuticals, Ltd. • 5/20/2003. Axcan increased an offer price to $10.50 and extended the expiration date of the offer until 5:00 p.m., New York City time on June 27, 2003. • 5/27/2003. Salix’s managers recommended to reject the revised offer.

6/9/2003.Axcan contends that Salix violated the tender offer and proxy rules under the U.S. securities laws when Salix stated that an analyst was "independent" without disclosing that the analyst's firm has a long-standing relationship with Salix. • 6/19/2003. Salix Pharmaceuticals, Ltd. (Nasdaq:SLXP) announced at its 2003 Annual Meeting of Stockholders, held earlier today, that based on preliminary reports from the Company's proxy solicitor, in excess of 92% of the votes cast were "FOR" the five Salix director nominees, and less than 6% of the votes cast were for the Axcan Pharma slate. • 6/27/2003. Axcan Pharma Inc. (NASDAQ: AXCA) announced that its $10.50 per share offer for all outstanding shares of Salix Pharmaceuticals, Ltd. (NASDAQ: SLXP) expired today at 5:00 p.m. New York City time, without the acceptance of the tendered shares.

6. Governance and Anti-takeover measures Source: “Case Studies in Finance” by Robert F. Bruner and “Corporate Governance and Equity Price” by Gomper, Ishii and Metrick, Quarterly Journal of Economics, 2003 Issue: Entrenchment and Discipline. • Poison Pill (Shareholder right plan)– right to obtain the stocks at a cheaper cost. • Greenmail – buyback target shares from the bidder. • Restricted voting right – deprives a shareholder of voting rights. • Classified (Staggered) Boards with more voting power delay the attainment of control by the bidder. • Supermajority Amendment requiring an approval from a large percentage of the shareholders. • Fair Price Amendment preventing two-tier or freeze-out. • Golden Parachute – compensation to managers/directors after taken over. • Silver Parachute – compensation to general employees.

Leveraged recapitalization with or without poison put making the debts immediately payable upon a change of control of the target. • Pac-man. • White Knights / Squires • Lock-up: To give an option to buy stocks or assets to a friendly buyer. • Stock repurchase. • Corporate charter amendments or Shark Repellent. • Blank check preferred stocks. • Law suits or report to regulatory bodies. • State laws and antitrust regulations.

7. Risk/Merger Arbitrage • An investment strategy, taking a long position in target stocks and short position in acquirer stocks. • Short term investment strategy driven only by economic motives. • To evaluate likelihood of the deal being consummated.

Ex) Return calculation for a long position in target stocks • Example 1) Between 2/11/2003 and 4/28/2003 Target stock: +2.3% and Bidder: +9.6% • Example 2) Between 4/10/2003 and 6/27/2003. Target stock: +7% and Bidder: +14%.

Source: “A Test of Risk Arbitrage Profitability,” by Ben Branch and Taewon Yang, International Review of Financial Analysis, 2006

8. Are Mergers always successful? – empirical findings Source: “Takeover, Restructuring and Corporate Governance” by Weston, Mitchell and Mulherin,4th edition and other article. • Several scholars (Healy, Palepu and Ruback, 1992 and Andrade, Mitchell and Stafford, 2001) found that operating cash flows/performance tend to improve, compared to industry peers. They attributed to improved asset management. Shahrur (2005) argued that improved buying power in horizontal mergers has a positive impact. • Loughran and Vijh (1997), Rau and Vermaelen (1998) and Mitchell and Stafford (2000) found insignificantly negative post-merger stock returns for 5 and 3 years.

Cash mergers tend to generate positive post-merger returns whereas stock mergers generate negative post-merger returns. Value firms with a high book-to-market tend to generate positive post-merger returns whereas growth firms with a low book-to-market generates negative post-merger returns.