Download

1 / 42

430 likes | 621 Views

United States Tax Court. U.S. Tax Court. Established by §7441 Nineteen Judges – 19 of them Judges are specialists Fifteen year term Circuit ride Usually only one judge hears a case. But may be En Banc, depending on significance/impact of the issue. U.S. Tax Court (cont’d).

E N D

U.S. Tax Court • Established by §7441 • Nineteen Judges – 19 of them • Judges are specialists • Fifteen year term • Circuit ride • Usually only one judge hears a case. But may be En Banc, depending on significance/impact of the issue

U.S. Tax Court(cont’d) • The Tax Court has the right to go beyond the issues brought before it and examine the petitioner’s entire return if it so desires. Extremely rare.

U.S. Tax Court(cont’d) • No jury option • Deficiency only – don’t have to pay first • How to get to Tax Court: • File Tax Court petition after receiving the IRS Statutory Notice of Deficiency (“90 day letter”) (ticket to Tax Court).

U.S. Tax Court(cont’d) • TC decisions • Regular • Memorandum – only application (in Judge’s view) of existing law or interpretation of fact • May rely on both

U.S. Tax Court(cont’d) “The Golsen Rule” Jack E. Golsen, 54 TC 742 (1970) The Tax Court will follow the Circuit Court in taxpayer’s circuit (Golsen Rule) • Based on identical facts • Court may reach opposite decisions for taxpayers in different geographical areas

U.S. Tax Court(cont’d) • Golson reasoned that where a reversal would appear inevitable, due to the clearly established position of the Court of Appeals to which an appeal would lie, the Tax Court’s obligation as a national court did not require a futile and wasteful insistence on its view.

U.S. Tax Court(cont’d) • The logic behind the Golsen doctrine is not that the Tax Court (a national court) lacks the authority to render a decision inconsistent with any Court of Appeals (including the one to which an appeal would lie), but rather that it would be futile and wasteful to do so where the Tax Court would surely be reversed on appeal.

U.S. Tax Court(cont’d) Does not hear • Claims for refund (although may find an overassessment) • Employment tax – With certain exceptions • Excise tax • Etc., - non-deficiency procedure taxes – With certain exceptions

U.S. Tax Court(cont’d) Small Case Division - §7463 • Special Trial Judges - §7743A • Not over $50k per year at issue • Petitioner may be pro se or represented • Petitioner’s option • Decision is final – may not be appealed • Decision is not published, not a precedent

Citations • Whatever the court, • Whatever the case, • Be sure to give a complete/accurate citation for any authority you rely on • See Appendix B

U.S. Tax Court(cont’d) Regular decisions are published by the GPO Citation: Fausner, Donald W., 55 TC 620 • 55 = TC Volume # • 620 = volume page #

U. S. Tax Court(cont’d) • Memorandum decisions cite depends upon the publisher; published only by the tax services • CCH: Fausner, Donald W., 30 T.C.M. 1187 (1971) • 30 = CCH TCM volume # • T.C.M. = CCH TC memorandum decisions • 1187 = page # • (1971) = year of decision • General (unpublished): Fausner, T.C. Memo 1971- (#)

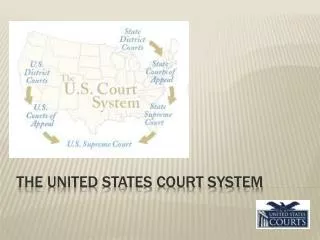

U.S. District Court • Judges • Generalists • One judge • Jury upon request • Emotional / equity issues • Jury can only decide facts. Judge deals with legal matters.

U.S. District Court(cont’d) • How to get a case in U.S. District Court • Must have paid the tax, filed claim for refund • Tax paid with return • Pay tax deficiency following an audit. • File Form 1040X and request a refund • If refund is denied appeal administratively • If appeal is denied file suit in U.S. District Court

U.S. District Court(cont’d) Bankers & Farmers Life Insurance Company and Southern Medical Life Insurance Company, PLAINTIFF v. U.S., DEFENDANT, Civil Action No. W-76-CA-62, 1979-1 USTC ¶9333 (WD TX, 1979). (CCH cite)

U.S. District Court(cont’d) Bankers & Farmers, supra.: • “One of the two special verdict questions submitted to the jury at the close of the evidence presented this fact issue for their consideration, as follows”: • ‘Did Jesse Derrick, president of Bankers and Farmers Life Insurance Company, have the authority to sign the election to transfer the policyholders surplus account?’ • “Thus, it appears to the Court that it was the proper function of the jury in this case to decide that the §815(d)(1) election was in fact the result of a good faith reliance by Bankers & Farmers on a material mistake of fact.”

U.S. District Court Bankers (cont’d) • “It is also clear that the withdrawal of the election in this case leads to the more equitable result.” (emphasis added)

U.S. District Court(cont’d) Citation CCH: > Bankers & Farmers Life Insurance Company and Southern Medical Life Insurance Company v. U.S.A, (DC-Tex) 79-1 USTC ¶9333 > 79-1 = volume # > USTC = CCH’s United States Tax Cases > ¶9333 = Paragraph #

U.S. District Court(cont’d) • Reliability? • Varies • Chance of overturn on appeal

United States Court Of Federal Claims

U.S. Court of Federal Claims • National jurisdiction • Sixteen judges • Judges may travel to your location • All monetary claims against the U.S. • Judges are generalists • No jury option • Again, as the name implies, tax must have first been paid

U.S. Court of Federal Claims(cont’d) • Citation - West: • 30 Fed. C1. 396 (1994). • 30 = volume # • Fed. C1. = West’s U.S. Court of Federal Claims • 396 = page # • 1994 = decision year

U.S. Court of Federal Claims (cont’d) • CCH cite • 94-1 USTC ¶50,044 (Fed. C1., 1994)

United States Courts of Appeals

U.S. Courts of Appeals • Eleven geographic circuits • One D.C. – D.C. District Court • Federal Circuit – appeals from U.S. Court of Federal Claims • Thirteen Total • Under which jurisdiction are you?

U.S. Courts of Appeals(cont’d) • First level of judicial appeal • Judges typically a panel of three • Each Circuit CA is independent of all others. Obligated to follow only decisions of the U.S. Supreme Court.

U.S. Court of Appeals(cont’d) • Generally will hear only questions of law. • Usually will not disturb the trial court’s findings of fact. • Why? The trial court, having heard witnesses first hand, etc., is in the best position to determine the facts. • Will overturn a fact determination only if the trial court was clearly in error.

U.S. Courts of Appeals(cont’d) • Usually the final authority in tax matters. • Why? The Supreme Court usually will hear only three or four tax cases per year. • Because we are in the Ninth Circuit, what is the weight of a Ninth Circuit decision? • The Tax Court here will follow that decision on identical facts. • Can get out of the Ninth Circuit by paying the tax, filing a claim for refund and filing suit in the U.S. Court of Federal Claims (Federal Circuit).

U.S. Courts of Appeal(cont’d) • Citation - CCH: • Bankers & Farmers Life Insurance Company v. U.S., (CA-5, rev’g DC) 1981-1 USTC ¶9369 • 81-1 = CCH Volume • #9369 = page #

U.S. Courts of Appeal(cont’d) • Fifth Circuit in Bankers and Farmers: • “We conclude that the district court's reliance upon the jury's response that the election was based upon a mistake of fact and upon Meyer's Estate was incorrect. The jury's determinations that Bankers & Farmers relied on a mistake and that the reliance was in good faith are factual findings entitled to the normal deference which courts must give a jury's findings of fact. But the jury's determination that the mistakes themselves were factual bound the trial court not one whit. The trial court's characterization of the mistakes upon which Bankers & Farmers relied as factual is itself a question of law freely reviewable on appeal.”

U.S. Courts of Appeal(cont’d) • “In our view, neither the literal language of the statute nor the indicated Congressional purpose supports Banker & Farmers' position. No funds were distributed from the policyholders' account and none were returned by Bankers & Farmers' shareholders. The timing of events specified in §815(d)(6) is absent. Most important, Bankers & Farmers' election was patently intentional, not inadvertent. Therefore, the scope of relief envisioned in subsection (d)(6) does not reach Bankers & Farmers' ill-timed election to recognize the Phase III gain.”

U.S. Courts of AppealCitations (cont’d) • Citation - West: • 643 F.2d 234 • 643 = volume # • F.2d = West’s Federal Reporter, second series • 234 = page #

U.S. Supreme Court • No automatic right of appeal to the Supreme Court • Petition by Writ of Certiorari – certiorari will be “granted” or “denied.”

U.S. Supreme Court • Certiorari granted in very few tax cases; only when • Significant and widespread issue, and • Split among the Circuits.

U.S. Supreme Court(cont’d) Denial of certiorari • Is not an “upholding” or approval of the lower court decision, (and cannot be relied upon as such) although the lower court’s decision will stand.

U.S. Supreme Court(cont’d) • Citations - Corn Products Refining Co. • West: 76 SCt 20 (aff’g CA-2) • Cumulative Bulletins: SCt (aff’g CA-2) 1955-2 CB 51 • CCH: (aff’g CA-2), 55-2 USTC ¶9746 (USSC, 1955) • GPO Reporter: (aff’g CA-2), 350 US 46

Substantial Understatement Penalty Authority Reg. 1.6662-4 • Notwithstanding the preceding list of authorities, an authority does not continue to be an authority to the extent it is overruled or modified, implicitly or explicitly, by a body with the power to overrule or modify the earlier authority. • In the case of court decisions, for example, a district court opinion on an issue is not an authority if overruled or reversed by the United States Court of Appeals for such district. • However, a Tax Court opinion is not considered to be overruled or modified by a court of appeals to which a taxpayer does not have a right of appeal, unless the Tax Court adopts the holding of the court of appeals. • Similarly, a private letter ruling is not authority if revoked or if inconsistent with a subsequent proposed regulation, revenue ruling or other administrative pronouncement published in the Internal Revenue Bulletin.

Substantial Understatement Penalty Authority • Reg. 1.6662-4(d): Effect of having substantial authority. • If there is substantial authority for the tax treatment of an item, the item is treated as if it were shown properly on the return for the taxable year in computing the amount of the tax shown on the return. • Thus, for purposes of section 6662(d), the tax attributable to the item is not included in the understatement for that year.

Substantial Understatement Penalty Authority Reg. 1.6662-4 • Taxpayer's jurisdiction. • “The applicability of court cases to the taxpayer by reason of the taxpayer's residence in a particular jurisdiction is not taken into account in determining whether there is substantial authority for the tax treatment of an item. • Notwithstanding the preceding sentence, there is substantial authority for the tax treatment of an item if the treatment is supported by controlling precedent of a United States Court of Appeals to which the taxpayer has a right of appeal with respect to the item.”