Download

1 / 53

530 likes | 614 Views

The Crisis and the Law. Empirical substantiations. G. Carchedi London, May 12, 2012.

E N D

The Crisis and the Law.Empirical substantiations G. CarchediLondon, May 12, 2012

The present financial crisis has revived the critiques of Marx’s law of the tendential fall of the rate of profit (for short, the Law). In particular, the critique has focused on the thesis that falling profitability is the ultimate cause of crises. My aim today is to assess the latest critiques in the light of empirical material. The focus will be (1) on the sectors producing material goods, a proxy for the productive sectors, because only these sectors produce value and surplus value, the vital lymph of capitalism, and (2) on the US economy because it is by far the most important worldwide.

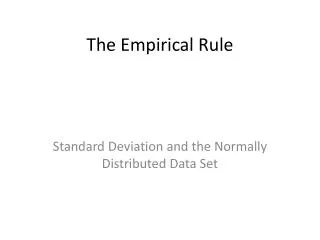

Efficiency • In Marx’s theory technological innovations increase efficiency, i.e. the effect on output of science and technology as incorporated in the means of production. Efficiency is measured by the number of labourers working with a certain quantity of means of production (or assets). This is the Labour/Assets (L/A) curve, the dotted line in chart 1.

Chart 1. Capital efficiency (L/A), labour’s productivity, and rate of exploitation

The labourers working with means of production worth 1 million dollars (deflated figures) dropped from 75 in 1947 to 6 in 2010.

Productivity • Efficiency is the basic determinant of productivity, i.e. output per labourer. This is the broken line in Chart 1. It shows that the output per labourer climbs from $30 million in 1947 to $235 million in 2010.

Chart 1. Capital efficiency (L/A), labour’s productivity, and rate of exploitation

Exploitation • Productivity is affected not only by efficiency but also by the rate of exploitation (a distinction you will not find in conventional economics). This is the continuous line in Chart 1.

Chart 1. Capital efficiency (L/A), labour’s productivity, and rate of exploitation

The implication is that a falling rate of exploitation, as in the period up to the mid 1980’s, depresses the effects of rising efficiency on productivity. Vice versa a rising rate of exploitation amplifies the effect of rising efficiency on productivity, as from the mid 1980’ to date.

The replacement of labour by means of production causes average profitability to fall. In fact, if only labour produces value (a point to be substantiated below), the replacement of labourers by means of production (the increase in the organic composition of capital) implies less value and less surplus value produced per unit of capital invested.

Chart 2. Average rate of profit (ARP) and organic composition of capital (C/V)

Two conclusions follow. First, in the long run, the organic composition rises due to rising efficiency while the trend of the ARP falls. This confirms Marx’s theory of the tendential fall in the ARP: the two trends move in opposite directions, i.e. profitability falls because efficiency rises.

Second, if assets relative to labour rise while the ARP falls, assets cannot produce surplus value. But then, they cannot produce value either. Given that there are only two factors of production, means of production and labour, it is labour and only labour that produces value and surplus value. The law of value is empirically substantiated.

Let us now disaggregate the post-WWII secular period into two medium-terms periods, or phases. Given the cardinal function of value in Marx’s theory, the discriminating factor should not be GDP (as in non-Marxist and many Marxist works) but employment and thus value. In the upwards phase, employment grows from 17.56 million in 1947 to 24.97 million in 1979. In the downwards phase, it falls to 17.79 million in 2010, approximately the 1947 level.

Table 1. The two phases within the secular fall in the ARP • Employment: % growth 1947-1979 +42.17% • 1980-2010 -26.4% • Total value: % growth 1947-1979 855% • 1980-2010 240% • New value: % growth 1947-1979 679% • 1980-2010 136%

Let us consider the two phases in more detail. The period between the end of WWII and the 1970s has been called the Golden Age of capitalism. Usually, the focus is on GDP in the economy as a whole. Here the focus is on the expanded reproduction of labour power in the productive sectors and thus on the (new) value created.

Table 1 shows the vigorous growth of both labour and value in the first phase

Employment: % growth 1947-1979 +42.17% • 1980-2010 -26.4% • Total value: % growth 1947-1979 855% • 1980-2010 240% • New value: % growth 1947-1979 679% • 1980-2010 136%

while Chart 2 shows that in the same phase the trend of the ARP falls.

The difficulty is to explain how the ARP could fall in a period of expanded reproduction. • WWII provides the answer. • The war caused an enormous compression of US labour’s purchasing power and a massive conversion of the civilian into the military industry, i.e. a destruction of capital in the civilian sphere.

With the end of the war, the liberation of this purchasing power and the reconversion of the military industry into the civilian one spurred the production first of means of consumption and then of means of production. Greater employment, wages, and profits followed and with them a further surge in purchasing power.

This was the reconstitution of previously destroyed capital. Note that destruction of capital is for some author the destruction of commodities (principally, the means of production). For some other authors it is their depreciation.

But, if capital is essentially production relations and the commodities in which those relations are frozen, the destruction of capital in the US during the war was the annihilation of the means of destruction (weapons and military apparel). But more importantly, it was the destruction of the production relations in the civilian sphere, i.e. the conversion of the civilian economy into a military one. The reconversion after the war meant the reconstitution of those relations on a massive scale and consequently the opportunity for the liberation of labour’s pent-up demand.

This is the reason why, in the first phase, the economy grew is spite of the fall in the ARP. In this phase, the fall of the ARP prepared the conditionsfor the emergence of crises in the second phase. The most efficient capitals could still accumulate and could absorb the technological unemployment they caused. Crises were only potentially present. Difficulties of realization played no relevant role. But the constantly falling profitability undermined economic growth from within because it kept reducing employment and thus the new value produced.

As more firms closed down and unemployment grew, the second phase set in. Difficulties of realization began to emerge because the decreasing labour force could not absorb the greater output any longer. The wage share started to fall in 1973 and the expanded reproduction of the labour force ended in 1979.

Realization difficulties became a feature of the second phase. In this phase, the liberation of the pent up purchasing power and the reconversion of military into civilian economy, the two powerful counteracting factors that had held back the crises in the first phase, could no longer neutralize the constant fall in the ARP and avoid crises. When crises finally emerged, they had been preceded by a quarter of a century of falling profitability. Falling profitability continues also in the second phase. After each crisis, there is a recovery. But after each recovery, there is a crisis because the ARP keeps falling, because the fall of the ARP has not been halted and reversed.

Difficulties of realization multiplied starting in the mid-1980s, when wages came under a savage assault by capital as a measure against decreasing profitability. The result was a boost of profits, but not of profit rates, with the exception of the 2003-2006 period, to be considered shortly. However, the productive sectors could not accumulate these higher profits because the vigorous expanded reproduction had ended and because of the greater difficulties of realization due to wage cuts.

At this point, capital started to migrate to the financial and speculative sphere that offered higher profit rates. These higher rates attracted further capital. The speculative bubble (basically, the explosions of derivatives) inflated. When the size of the unproductive sectors became too large for the productive ones to provide the flow of surplus value needed for the continuous growth of unproductive profits, the financial crisis erupted.

It is common opinion that financial crises are the cause of the crises in the ‘real’ economy simply because the former seem to precede the latter. However, while the ARP in the productive sectors began its long descent right after WWII, the first financial (stock market) crisis erupted only in 1973-74. If falling profitability in the productive sectors preceded the emergence of the first financial crash by a quarter of a century, the former must have been the breeding ground of the latter. From that point on, financial crises have become a recurrent feature of the economic landscape. In spite of the different triggers, their recurrence shows that there must be a common cause. This is the constantly deteriorating profitability in the productive sectors.

It follows that financial crises are the catalyst rather than the cause of the crises in the productive sectors and that the cause of the present crisis has not been ‘financialization’, the decoupling of the financial sphere from the productive one. The same causal nexus that existed in the past exists still nowadays.

Recently, some critics have remarked that the 2007 financial crisis has emerged after a rise in the ARP. Therefore, they argue, the fall in the ARP cannot be the (ultimate) cause of all crises. • Three perspectives are possible.

Notice that the trend in the ARP keeps falling no matter which distribution policies are applied (rising wages relative to profits from the end of WWII to 1986 and the reverse in the 1986-2010 period). • Let me dwell on this point by briefly touching upon a critique of underconsumptionism and of the profit squeeze theory.

A critiqueofunderconsumptonism. • Underconsumptionism holds that crises are due to falling wages and thus to labour’s reduced purchasing power. Due to unsold commodities, firms’ profitability falls and investments fall too. The slump is ushered in. • But it is possible to show algebraically that, if wages fall, profits rise always, even in case of maximum loss, i.e. even if all commodities whose price corresponds to the wage cuts remain unsold.

Then, if profits rates fall in spite of lower wages, the reason is that the rise in the organic composition overweighs the fall in wages or that a nation’s capital has become less relative to that of other nations. • Falling wages cannot explain neither the origin of crises nor their continuation.

If falling wages cannot explain the origin of the slump, higher wages cannot lift the economy out of it. Higher wages do increase labour’s purchasing power. Underconsumptionism holds that output (first of the means of consumption and then of the means of production) would be spurred and with it the recovery. • But capital does not expands production if profitability falls due to increasing wages, in spite of a greater purchasing power. The following chart shows empirically the fallacy of underconsumptionism

The incompatibilitybetween Marx and Keynes • This chart shows that, when wages (relative to profits) rise, the ARP falls instead of rising, contrary to underconsumptionism. When wages fall, the ARP rises instead of falling, again contrary to underconsumptionism. • Underconsumptionsim is empirically disproved and Marx is empirically substantiated.

Critiqueof the profit squeeze • Chart 4 would seem to substantiate the profit squeeze theory. This theory identifies the cause of crises in rising wages and concomitant fall in profits and profit rates. It would deem to conform to Marx. However, the inverse relation between profits and wages presupposes a fixed (or decreasing) quantity of new value. But in a phase of expansion, both wages and profits grow.

Then, if we assume that profit falls because wages rise, we assume that economic growth has ended and that the crisis has already begun, i.e. we assume what is to be explained. It is only after economic growth has come to an end that higher wages reduce profits, thus worsening the crisis, rather than causing it. • Rising wages cannot explain the crisis.

In sum, redistribution policies cannot cause the cycle. Only the generation of value and surplus value, as indicated by the falling trend in the ARP, can cause it.

This implies by no means that it is useless to demand pro-labour policies. But they should not be framed within a Keynesian view, i.e. as if these policies were favourable both to capital (because capital would exits the crisis) and to labour. • The perspective should be the Marxian one: higher wages are favourable to labour and not to capital. They weaken capital and thus are a condition for its supersession.

The secondperspective • The critics’ second perspective is the 1986-2006 period removed from its historical context. Given that what determines the cycle is the production of surplus value rather than its redistribution, the question is whether in this period this production relative to the capital invested falls or rises. To answer this question, I have computed the ARP by holding the rate of exploitation constant throughout the secular period. Then, this ARP reflects only the variations in the value produced.

Production and overall ARP • Let us call this rate the production ARP, to be distinguished from the overall ARP, the result of both the tendency and the countertendencies, in this case the variations in the rates of exploitation. • Chart 5 below shows that while the overall ARP has been rising since 1986, the production ARP has been falling

The rise in the overall ARP is due to greatly increased rates of exploitation, a long-term, sustained countertendency, the manifestation of the historic defeat of the world working class, a defeat from which labour has yet to recover. This critique too is invalid.

The thirdperspective • The critics’ third perspective focuses on the 4 years immediately preceding the 2007 crisis. In this period, the production ARP rises. This would seem to confirm the critics’ argument. However, table 3 below shows that the production ARP grows minimally, from 7.1% in 2003 to 7.5% in 2006, hardly an indication of a reversal of the tendency, of economic recovery. Moreover, 7.5% is lower than any single rate since 1947. In reality, the production ARP has stagnated at around 7% after a 56-year fall and has started to fall again after that short pause. What has really happened is a tremendous increase in the rate of exploitation. Table 3 compares the relevant data.