Download

1 / 39

390 likes | 490 Views

Va Loans for Vets provides and assists all veterans and active duty military with ALL of their VA Home Loan Financing Needs. Be a proud homeowner today. For more details call us at 480-351-5904 or visit our site http://www.valoansforvets.com/<br>

E N D

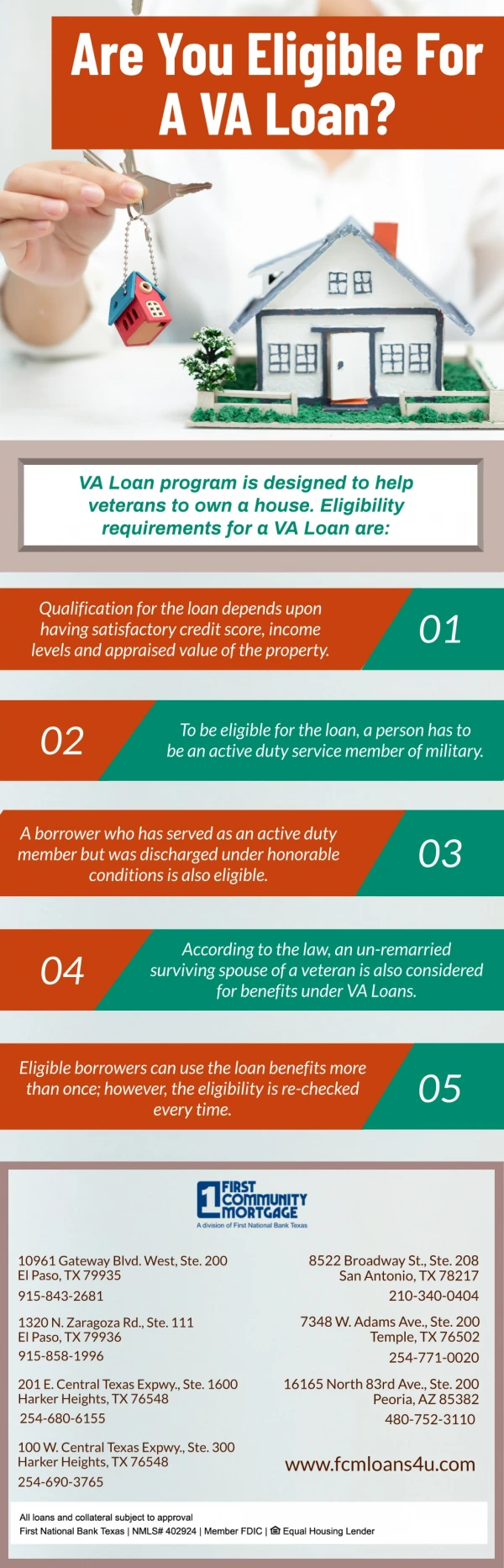

How to Determine if You are Eligible FOR A VA LOAN

Veteran’s benefits are one of the ways in which we are able to show veterans our appreciation of their service to the country.

One key benefit is the VA-guaranteed home loan. If you’ve wondered how to get a VA loan, here are a few basics you need to know.

If qualified, loans can be used to purchase a condominium or house, improve a home, build a house, or buy a manufactured home and/or lot.

To proceed with the process you must obtain a Certificate of Eligibility (COE) that verifies to the lender that your discharge conditions and service requirements authorize you for VA backing.

A mortgage broker or lender that specializes in this type of mortgage lending can help you verify personal eligibility and apply for the COE.

Generally a VA-guaranteed mortgage is a real plus because: It guarantees repayment to the lender of at least a portion of the loan Thereby allowing the lender to be a bit more relaxed about credit and credit score criteria.

It is a good idea to familiarize yourself with your FICO score and credit report prior to approaching a lender.

If your score is negatively impacted by issues such as unpaid collection items, past dues and so forth, you may want to pay off or pay current so that your score will improve.

It is important to demonstrate to potential lenders that you are reliable about paying debt obligations.

To get a free copy of your credit report, once each year go to www.annualcreditreport.com.

Lenders also want to know if you have the cash flow availability to pay the mortgage note.

This is known as debt-to-income ratio. Review your debt structure and determine what percentage of the household income is committed to set monthly bills…

… and how much is discretionary income. The more discretionary income you have, the better.

Generally if the appraisal value of the home is the same as or more than the sales price …

… you may not be required to make a down payment, or can pay less than the lenders normal requirement.

You do not have to be a first-time buyer, and the benefit can be reused.

Other qualified veterans may be able to assume your loan in the future.

A potential lender wants to know that you have an adequate and reliable income flow to be able to make house payments for the life of the loan.

It is safe to assume that your employment, including length of employment, will be verified.

Two years of steady employment is desirable, and if it is with the same employer, even better.

There are always exceptions to the rule so don’t despair if you cannot meet this burden.

Be prepared to explain why the exception, and to offer some type of evidence as to the dependability of future cash flow streams.

FINISHING Touches

Once you have worked with your real estate professional to find a home, negotiated an acceptable price…

… signed a purchase agreement, and applied for the VA Loan, the lender will begin the approval process.

Once these processes are completed a closing date will be set so the property can be transferred to you.

Jimmy Vercellino, VA Loan Specialist helps veterans obtain the loans they are entitled to.

He served in the United States Marine Corps, and now devotes himself to the Veteran home buyer in the Phoenix area, fulfilling a passion of his while at the same time helping others achieve home ownership.

Be a proud homeowner today. For more details call 480-351-5904 or visit the site www.valoansforvets.com

VA Loans for Vets 7702 E. Doubletree Ranch Road, Suite 220 Scottsdale, AZ 85258 Phone: (480) 351-5904 Email: jimmyv@fcbmtg.com