Download

1 / 22

220 likes | 229 Views

This course explores the theory of optimal currency areas and analyses the costs and benefits of joining a monetary union. It focuses on the European Central Bank and the functioning of the eurozone, including monetary and fiscal policies. The course also examines the impact of asymmetric shocks and different adjustment mechanisms in a monetary union.

E N D

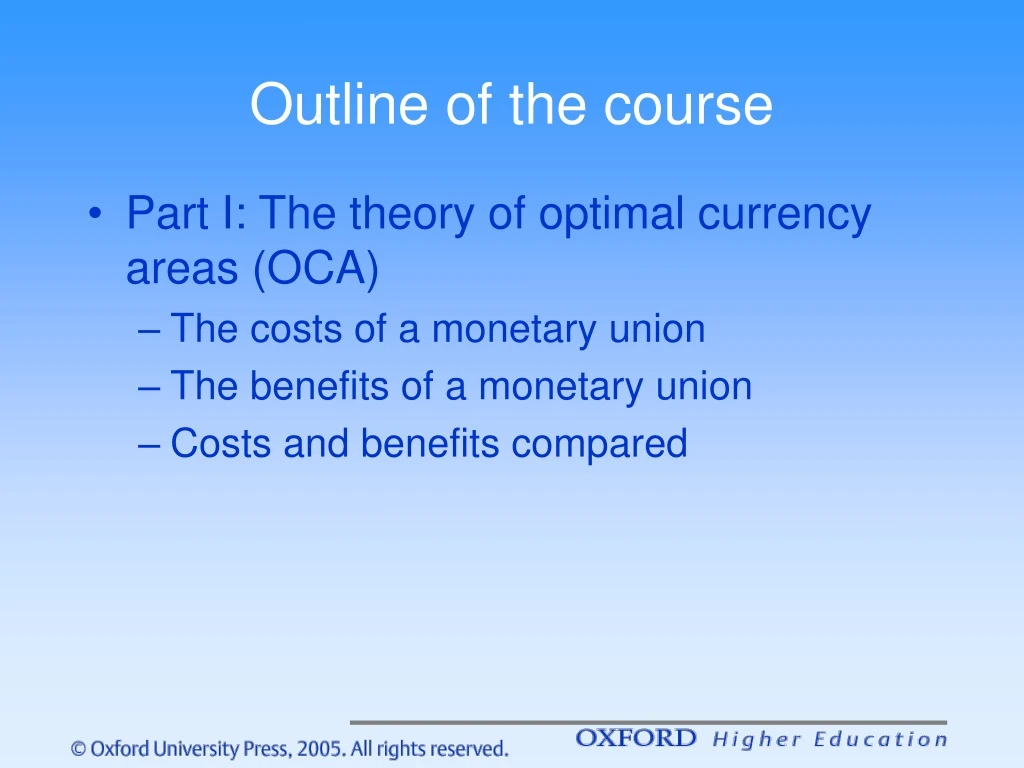

Outline of the course • Part I: The theory of optimal currency areas (OCA) • The costs of a monetary union • The benefits of a monetary union • Costs and benefits compared

Part II: How do existing monetary unions work: the eurozone • The European Central Bank: institutional features • Monetary Policies in the Eurozone • Fiscal Policies in a monetary union

Chapter 1The Costs of a Common Currency Theory of optimal currency areas

Introduction • Costs arise because, when joining monetary union, a country looses monetary policy instrument (e.g. exchange rate) • This is costly when asymmetric shocks occur • In this chapter we analyse different sources of asymmetry

1. Shifts in demand (Mundell) • Analysis is based on celebrated contribution of Robert Mundell(1961) • Assume two countries, France and Germany • Asymmetric shock in demand • Decline in aggregate demand in France • Increase in aggregate demand in Germany • Need to distinguish between permanent and temporary shock • We will analyze this shock in two regimes • Monetary union • Monetary independence

Figure 1.1 Aggregate demand and supply in France and Germany France Germany SG PF PG SF DG DF YG YF

First regime: monetary union • How can France and Germany deal with this shock if they form a monetary union? • Definition of monetary union • Common currency • Common central bank setting one interest rate • Thus France cannot stimulate demand using monetary policy; nor can Germany restrict aggregate demand using monetary policy • Do there exist alternative adjustment mechanisms in monetary union?

Wage flexibility • Aggregate supply in France shifts downwards • Aggregate supply in Germany shifts upwards

Figure 1.2 The automatic adjustment process France Germany PF PG YF YG

Additional adjustment mechanism • Labour mobility • Is very limited in Europe • Especially for low skilled workers • Main reason: social security systems

Monetary union will be costly, if • Wages and prices are not flexible • If labour is not mobile • France and Germany may then regret to be in a union

Second regime: monetary independence • What if France and Germany had maintained their own currency and national central bank • Then national interest rate and/or exchange rate can be used

Figure 1.3 Effects of monetary expansion in France and monetary contraction in Germany France Germany PF PG YF YG

Thus when asymmetric shocks occur • And when there are a lot of rigidities • Monetary union may be more costly than not being in a monetary union • What about fiscal policies?

Insurance against asymmetric shocks • Insurance against asymmetric shocks can be organized • Two systems • Public insurance systems • Private insurance systems

Public insurance systems • Centralised budget allows for automatic transfers between countries of monetary union • Can offset asymmetric shocks • Is largely absent at European level (European budget only 1% of EU-GDP • Exists at national level • Creates problems of moral hazard

Alternative: flexible national budgets • France allows deficit to accumulate; Germany allows surplus • Integrated capital markets redistribute purchasing power • This imples automatic transfers between generations within the same countries • Create problems of debt accumulation and sustainability

Private insurance systems • Integrated capital markets allow for automatic insurance against shocks • Example: stock market • Insurance mainly for the wealthy

Other sources of asymmetry: • Different labour market institutions • Centralized versus non-centralized wage bargaining • Symmetric shocks (e.g. oil shocks) are transmitted differently when institutions differ across countries • Different legal systems • These lead to different transmission of symmetric shocks (e.g. interest rate change) • Anglo-Saxon versus continental European financial markets

Different growth rates • Does a monetary union constrain the growth of less developed countries? • Different fiscal systems • Countries with less developed fiscal system rely more on inflation tax • These countries will have to raise explicit taxes in monetary union

Symmetric and asymmetric shocks compared • When shocks are asymmetric • monetary union creates costs compared to monetary independence • Common central bank cannot deal with these shocks • When shocks are symmetric : • Monetary union becomes more attractive compared to monetary independence • Common central bank can deal with these shocks • Monetary independence can then lead to conflicts and ‘beggar-my-neighbour’ policies

Figure B2.1 Symmetric shocks: ECB can deal with these France Germany PF PG YG YF