Download

1 / 28

280 likes | 425 Views

AcademyHealth. Reducing Health Insurance Costs for Small Business Chicago--June 29, 2004. Purpose. Provide perspective on benefit design issues facing today’s employers and employees. Provide input on the “new” HRA, HSA opportunities. William N. Lindsay III, CLU, RPA

E N D

AcademyHealth Reducing Health Insurance Costs for Small Business Chicago--June 29, 2004

Purpose • Provide perspective on benefit design issues facing today’s employers and employees. • Provide input on the “new” HRA, HSA opportunities. William N. Lindsay III, CLU, RPA Benefit Management & Design, Inc.

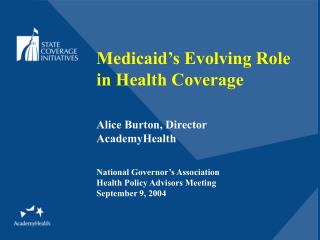

Increases in Health Insurance Premiums Compared to Other Indicators, 1988-2003 Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits 2003

Can we afford it or are we willing to pay for it? Reden & Anders, Inc. 2000

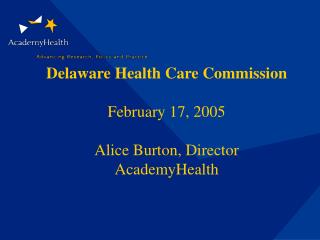

Health Plan Enrollments For Covered Workers, Selected Years 1996-2001 Sources: Kaiser/Health Research and Educational Trust (HRET) Survey of Employer-Sponsored Health Benefits, 1999, 2000, 2001; and KPMG Survey of Employer-Sponsored Health Benefits, 1996, 1998.

“The leading cause of personal bankruptcy is health care costs.” Source: Prosperity Institute Report 2/2002

The "A's" MSA FSA HRA HSA

Issues with Medical Savings Accounts • Only a “pilot,” not permanent • Only for companies with fifty or fewer employees • Only employer or employee money (not both) • No copays permitted • Made dual coverage difficult

MSA Concept • Bring consumers into the equation • Allow rollover of unused funds • Create a way to offset high deductible with a “side fund” • Employee owns the fund and earns interest

FSA • AKA: “Section 125 Plan”, “Flexible Benefit Plan”, “Cafeteria Plan” • 3+ Components: Pretax premiums, Flexible Spending Account, Dependent Care • Enables employees to pay premiums on a pre-tax basis and thus avoid Federal income tax, FICA • Enables employees to set aside (unlimited) funds in an account to pay unreimbursed medical expenses on pre-tax basis

FSA Issues • Owners can’t participate • Requires plan document, SPD • May require IRS form 5500 • Non-discrimination test • “Employer at risk” concept • “Use it or lose it” rule

Executive Summary In this report, the Prosperity Institute explores America’s tax regime [the Internal Revenue Code (Code)] with the object of examining which of its provisions directly and unfairly disadvantage small firms or their owners compared with large firms. The purpose of this report is to identify sections of the Code which discriminate against small businesses and to propose revisions that would establish parity between small businesses and their larger counterparts.

Then…along came a Health Reimbursement Arrangement “HRA” • Treasury Department Ruling • Permits rollover of unused funds from year to year (no “use it or lose it”) • Can be offered in conjunction with a Flexible Spending Arrangement/125 Plan

BUT… • Employer funds only • Funds cannot revert to the employee upon termination, retirement or death* • Subject to COBRA • Nondiscrimination tests apply • Owners can’t participate*

Medicare Reform! Prescription Drug Benefit and… Health Savings Accounts (HSA)

What is an HSA? • Permits employee and/or employer tax-free contributions to a fund • Any size employer and any tax structure is allowed • Funds are not taxed when withdrawn for qualified reasons (Section 213 (d)) • Funds can accumulate at interest

What is an HSA? • Unused portions roll over from year to year (no “use it or lose it”) • Funds are portable • Annual contributions capped at lesser of actual deductible or $2,600 for individuals and $5,150 for families (expanded if over 55)

HSA Requirements • Must be a “qualified health plan” • $1,000 deductible for single (max $5,000) • $2,000 deductible for family (max $10,000) • No copays! • “Family Deductible” concept is new • Only for those under 65 • Can’t have an FSA or HRA* also • Can’t have spouse with dual coverage unless both are “qualified” high deductible plans

HSA Requirements (continued) • Qualified expenses exclude health insurance premium payments (except COBRA) • Funds withdrawn for non-medical purposed will be taxed, plus 10% penalty • Funds on deposit must be held in a custodial account. • Owners CAN participate

The Challenge? • Calculate the potential for savings with these plans • Determine whether these concepts fit the funding model and philosophy • Carefully consider the employee education/communication strategy

Ask Yourself… • Will these options meet our goals over time? • Will these options save us money? • Will we create more uncovered expense? • How will employees react?

Noah’s Principle: “The real value is not in predicting rain, but in building arks”

…At least we have more tools to consider! Thank You.